An Ominous Outlook for the Banking Sector

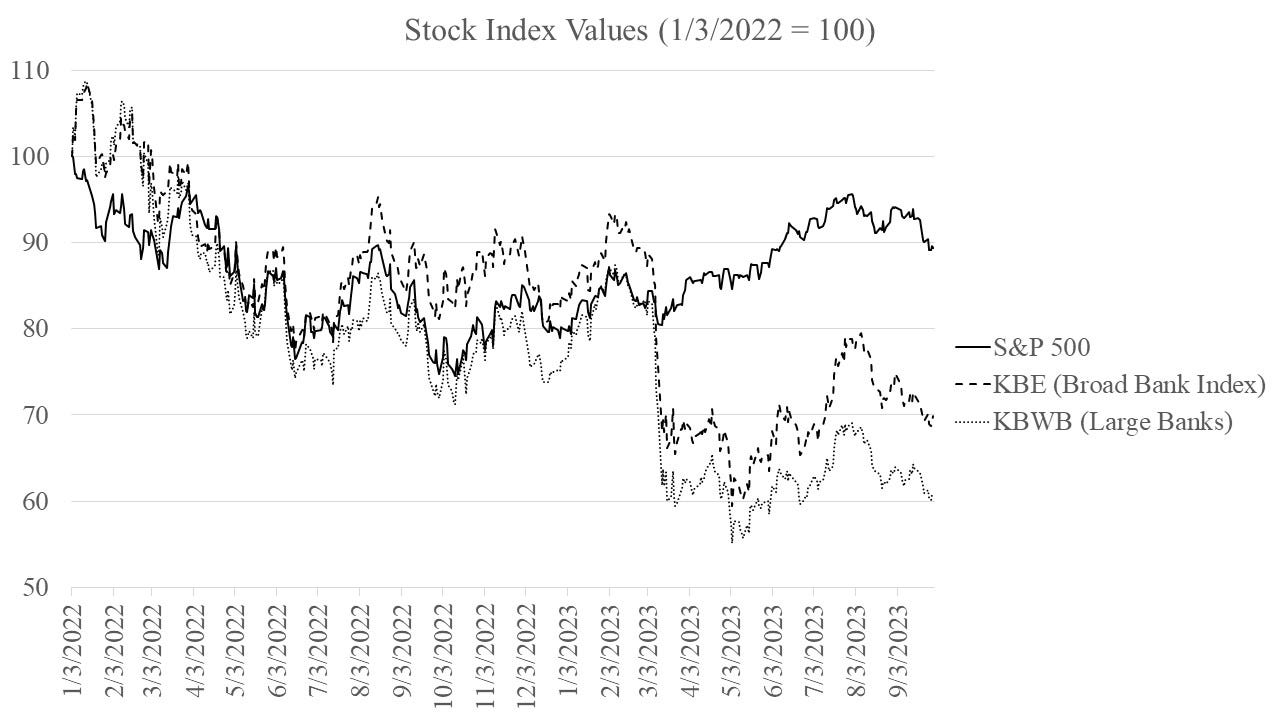

The inflationary Bear market of 2022 began after the stock market, as measured by the S&P 500 index, reached an all-time high on January 3, 2022 and subsequently declined by about 25 percent through October 12, 2022. The graph below depicts the decline, as well as the recovery that lasted through late July 2023, as the S&P 500 has dropped 6.6 percent since then, 4.8 percent since mid-September.

The banking sector, as proxied by the KBE index, and especially larger banks, as proxied by the KBWB index, have exhibited even worse performance, declining by almost 41 percent and 45 percent, respectively, in 2022 before recovering. That decline includes the effects of the regional bank failures between March and May. However, since late July, the KBE index and KBWB indices have declined by almost 12 percent, down 3.8 percent and 5.2 percent, respectively, since mid-September.

The recent decline reflects deteriorating long-term bond performance due to inflation and higher rates, which has caused a drag across asset classes, with the exception of short-term bonds that have maturities of no more than one year. The declines in long-term bonds have affected the banking sector, too.

The deteriorating performance of long-term bonds continues to create problems for some, though by no means all banks in the form of unrealized bond losses that arose with the rise in inflation. Since equity analysts began publicly discussing unrealized losses in the banking system earlier this year, the problem has not improved.

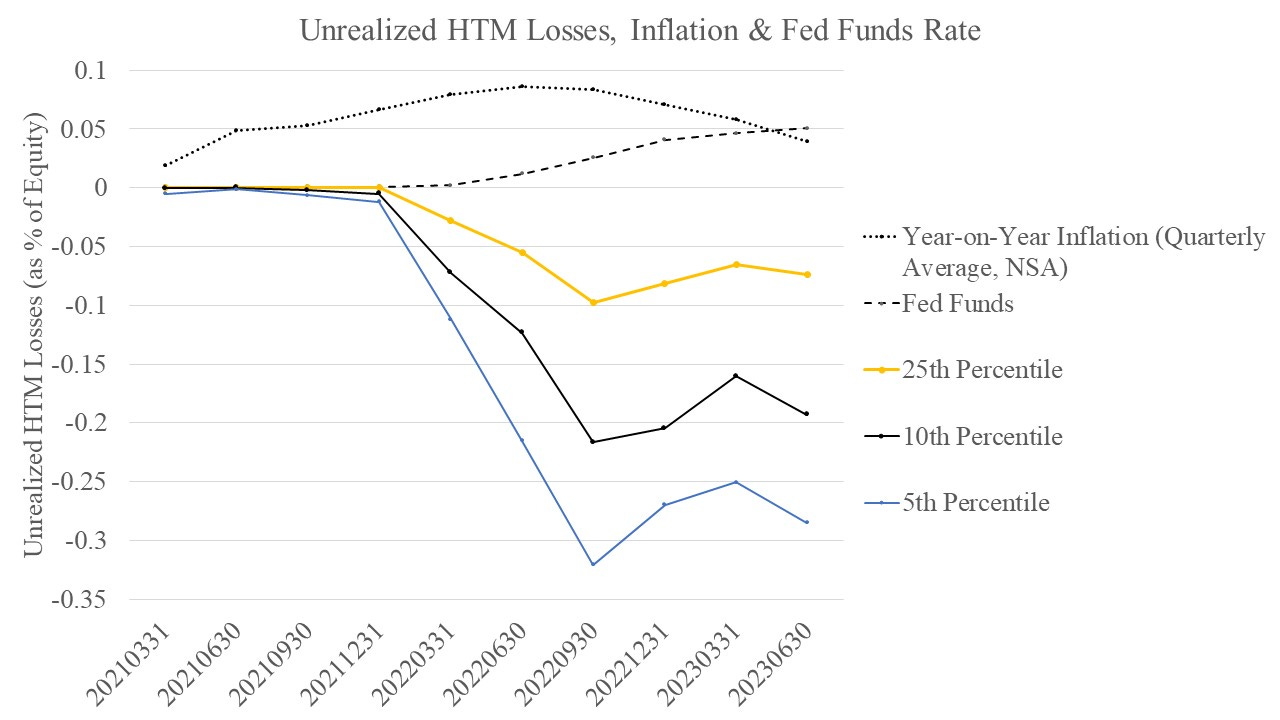

The figure below depicts the reported unrealized losses from held-to-maturity securities relative to book equity from bank call report data for the 25th percentile, 10th percentile and 5th percentile through June 30th 2023; not depicted is the median which equals roughly zero, which suggests that problem exists for a fraction of the banking system.

And we have already been observing weakened credit conditions for some time based on responses to the Senior Loan Officer’s Survey, which is likely due to the Bear Market of 2022 and risk of bank assets. When combined with high leverage, that can exacerbate weakness within the banking system.

To understand why, in a paper several years ago, professors Matthew Baron, Emil Verner and Wei Xiong set out to identify when banking crises have occurred since 1870 for a sample of 46 countries. The motivation for the exercise arises in part because historians have often produced inconsistent accounts of when banking crises have occurred and often provide no insight into the severity of crises. These authors find that, rather than being precipitated by bank runs, banking crises are often preceded by bank stock declines, and sometimes no runs occur during crises. Furthermore, these declines in stock market activity predict subsequent declines in economic activity, measured by gross domestic product, and also bank credit.

All told, the conditions in the banking system do not bode well for a vibrant economy. Now does not seem to be a good time for regulators to implement the proposed Basel III Endgame requirements onto the existing patchwork of complex bank regulation. But at the same time, if banks were funding with much more equity capital than they currently do, we might not have such concerns about the banking system.