Banks and Capital Distributions During Recession: A More Prudent Choice

Given the severe economic and financial circumstances facing U.S. banks, a question is raised regarding whether regulators should require them to suspend distributions of capital to investors. This would include bank dividends, stock buybacks, and distributions related to executive bonuses. I find it all too familiar that the focus is on what reluctant regulators should do rather than what bank managers must do to withstand the recession and contribute to the economy’s recovery. How they choose to conserve and use capital will influence how well matters end.

In this regard, four questions seem appropriate to guide their choice. First, given the depth of the on-coming recession, would it be best to retain additional capital to absorb unexpected losses? Second, after losses, will there be sufficient capital funding to retain and renew existing loans and support borrowers through the crisis. Third, is their access to needed capital funding to confidently honor lines of credit as corporations suddenly seek liquidity from their bankers? Finally, as the recession ends and companies begin to rebuild their operations, will there be capital to fund the expected increase in loan demand? Managers too often put these questions aside as they focus on the moment rather than the future.

In nearly all past recessions and crises, bank managers under-anticipate losses. During the crisis of 2007–2009, for example, as conditions deteriorated, bank managers announced loan loss provisions of several billions of dollars, promising they would amply address future expected losses. After such announcements, the five largest U.S. banks confidently distributed over $75 billion in dividends and billions more through stock buy backs. Losses, however, continued to mount and for these five banks eventually exceeded $350 billion. The current recession appears more severe than any since the Great Depression, and banks will almost certainly experience significant, perhaps record, credit losses.

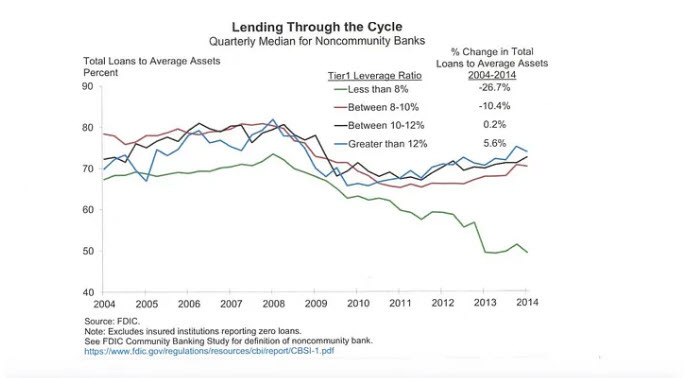

Also, as losses mount, borrowers that avoid default will still need credit support. Their revenues and income will be sharply reduced, and they will turn to their banker for loan extensions and concessions. Such support, as the chart below demonstrates, will come from the better capitalized banks, which consistently maintained stronger lending patterns during this last crisis. In contrast, banks with less capital, sharply reduced their lending as they dealt first with their own funding shortfalls. Given these experiences there is every reason for bank managers to conserve capital resources early, rather than wait for regulators to tell them the obvious, when it’s too late.

Under severe economic stress capital markets often cease being a source of short-term corporate funding. Companies immediately turn to pre-committed lines of credit to fill the funding gap. The Wall Street Journal reports, for example, that bank loans jumped by over $365 billion between March 11 and March 25 of this year to meet just such demands. This naturally absorbs bank capital, sometimes impeding needed flexibility in working with other stressed borrowers.

Finally, as the economy recovers and businesses restart, banks will be a primary source of loans. This is no small matter since every additional dollar of bank retained capital supports as much as 15 dollars of new loans. If the 10 largest banks in the U. S. retained the equivalent of their 2017 earnings, they could fund an additional $1 trillion of loans (Payouts, Retained Earnings, and Loan Growth). Preserving capital, being prepared to maintain and extend credit through the recession and beyond is what’s critical to the immediate and long-term health of the U.S. economy. Under such circumstances, distributing earnings hardly represents a good choice.

There is understandable concern that suspending dividends will hurt retail investors. As owners they are entitled to their share of any capital distribution, but they are investors not depositors. They are not guaranteed uninterrupted payments, especially when current and future needs and opportunities of their bank demand conservative payouts. Also, as investors they continue to own the retained capital, which is reflected in the price of the asset and future payouts when the crisis passes.

U.S. banks subject to the Federal Reserve’s most recent stress tests, passed and might expect to distribute capital consistent with these results. However, while useful, such tests rely on models that are hardly failsafe and are only as good as the assumptions behind them. Since the last tests were conducted, the country has experienced a pandemic and the near shutting down of its economy. Unemployment will be far higher and income far less than assumed in the most severe of recent tests. Private capital will be far scarcer than the models projected. A test is hardly necessary to know that retaining capital, not distributing it, is the prudent choice.

During this crisis, the Federal Reserve has taken on the role of commercial bank, investment bank and banker to the world. Hopefully, this will end as the crisis recedes. However, for the Federal Reserve to return to normal operations and do so successfully, the economy must regain its footing. The country needs its commercial banks to reestablish their role as intermediary rather the conduit for the Federal Reserve. Maintaining and further building a strong funding base best serves to assure this outcome. It appears the Federal Reserve is again leaving the decision in the hands of bank management and directors, let’s hope they choose well this time.