Bringing Back the Corridor Operating System With Positive Interest On Reserves

In my previous post, I discussed how the Fed’s Floor operating system contributed to the Fed experiencing a loss of $116 billion last year. This happened primarily because the income the Fed received from its asset holdings (Treasuries and mortgage-backed securities) generated less revenue than the interest on reserves the Fed now pays to banks, which increased as the Fed raised policy rates to fight inflation. While there may be interest in restoring the original Corridor system, in light of how bank capital requirements favor reserves, I would like to discuss some simple alternatives for bringing back the Corridor system but with positive rates of interest on reserves.

On Basel III Regulation, Excess Reserves and Bank Lending

I started thinking about this after writing a paper with Blake Hoarty, which showed how risk-based capital requirements distorted bank asset holdings after the implementation of US Basel III capital requirements in 2013. Bank reserve holdings and loans seemed particularly affected by the new regulation.

In the paper, we provide empirical evidence and theoretically confirm that when you increase risk-based capital requirements, as under Basel III, banks subjected to the regulatory change shift from high to lower risk-weight assets. Indeed, with the Floor operating system in effect, during the implementation of Basel III between Q1 2013 and Q4 2014, the largest “advanced approaches” banks, which are subjected to Basel III, did just that. These banks increased their holdings of 0 risk-weight Treasuries and reserves from an average asset share of 8.9 percent to 14.9 percent. Doing so likely helped these banks comply with US Basel III on time. Smaller banks only increased from an average asset share of 3 to 3.6 percent.

Moreover, you also see the rate arbitrage between Treasuries and reserves taking place by advanced approaches banks. For instance, from Q1 2013 and Q4 2014, as the rate of interest on reserves exceeded Treasury yields, advanced approaches banks increased holdings of reserves while keeping holdings of Treasuries constant. By 2015, however, Treasury yields exceeded interest on reserves and the advanced approaches banks began reducing their reserves shares while increasing their Treasury shares.

These portfolio shifts also seemed to affect loan shares for advanced approaches banks, which on average only grew from 28.7 percent to 29 percent between Q1 2013 and Q4 2014, while smaller banks on average increased their loan shares from 59.8 percent to 64.2 percent. These findings are consistent with the view that large banks held more reserves while smaller banks lent more after the implementation of Basel III. While our paper does not address whether Basel III reduced lending, one Fed staff study showed that overall, bank lending was not reduced, as other banks stepped in to lend where advanced approaches banks did not. All this is to say that interest on reserves play a role in the Fed’s operating system, and risk-based capital requirements distort bank balance sheets including holdings of reserves, especially for advanced approaches banks (the largest among these are also among the Fed’s primary dealers). It would, therefore, be good to keep risk-based capital requirements together with policy rates in mind when discussing reform options for the Fed’s operating system.

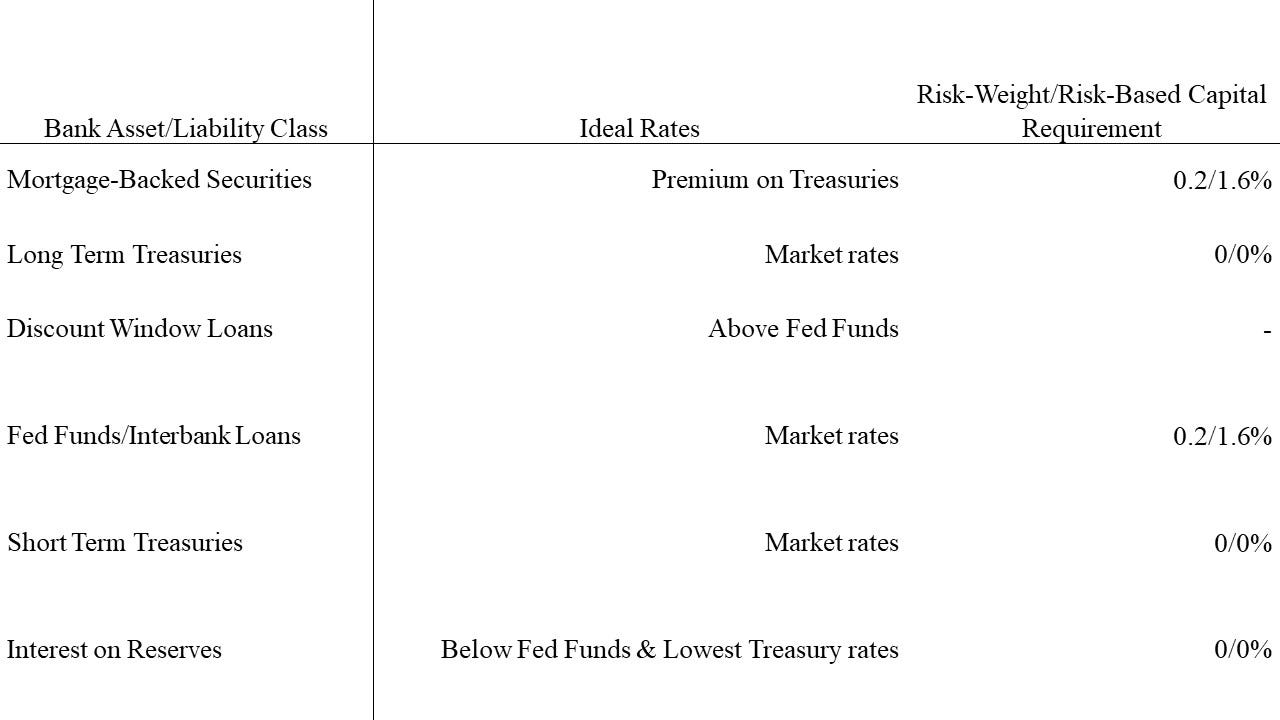

Corridor Asset Classes, Policy Rates and Risk-Base Capital Requirements

In the table below I list how rates of interest for the asset classes associated with the conduct of monetary policy under the Corridor operating system should ordinarily be ranked (from highest to lowest). I also list the risk-weight capital requirement for each asset class, when applicable.

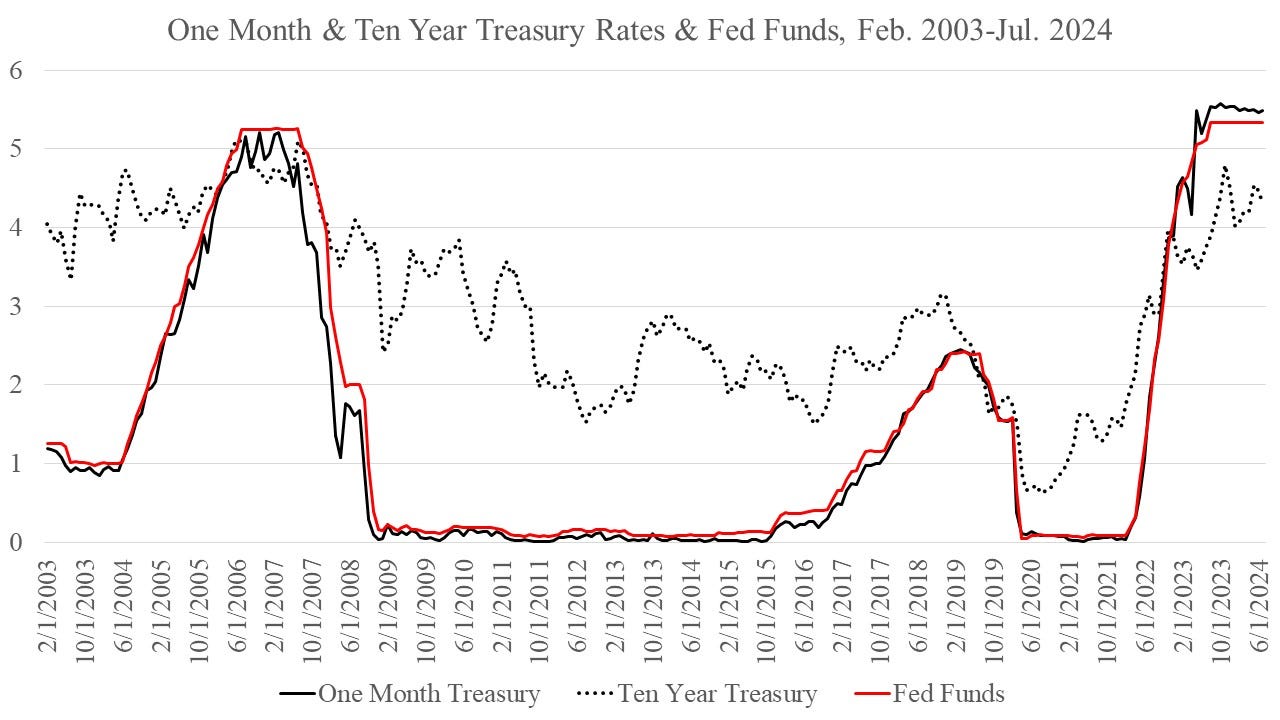

Ordinarily, the return for mortgage-backed securities should exceed that for Treasuries, as this New York Fed report explains how MBS and Treasuries relate through the option-adjusted spread. Next, the Discount rate, if it is to represent a penalty rate should lie above the Fed Funds rate. The Fed Funds rate should ordinarily be above short-term Treasury rates given that there’s likely more risk from overnight interbank loans than short-term Treasuries. The Fed Funds rate should also ordinarily be less than long-term Treasury rates given the interest rate risk reflected in the latter. The figure below shows that the Fed Funds rate lies above the short-term rate (represented by the one-month rate in the graph) and below the long-term rate (represented by the ten year rate in the graph). Exceptions arise if the term structure of Treasury rates inverts, reflecting expectations of lower future interest rates.

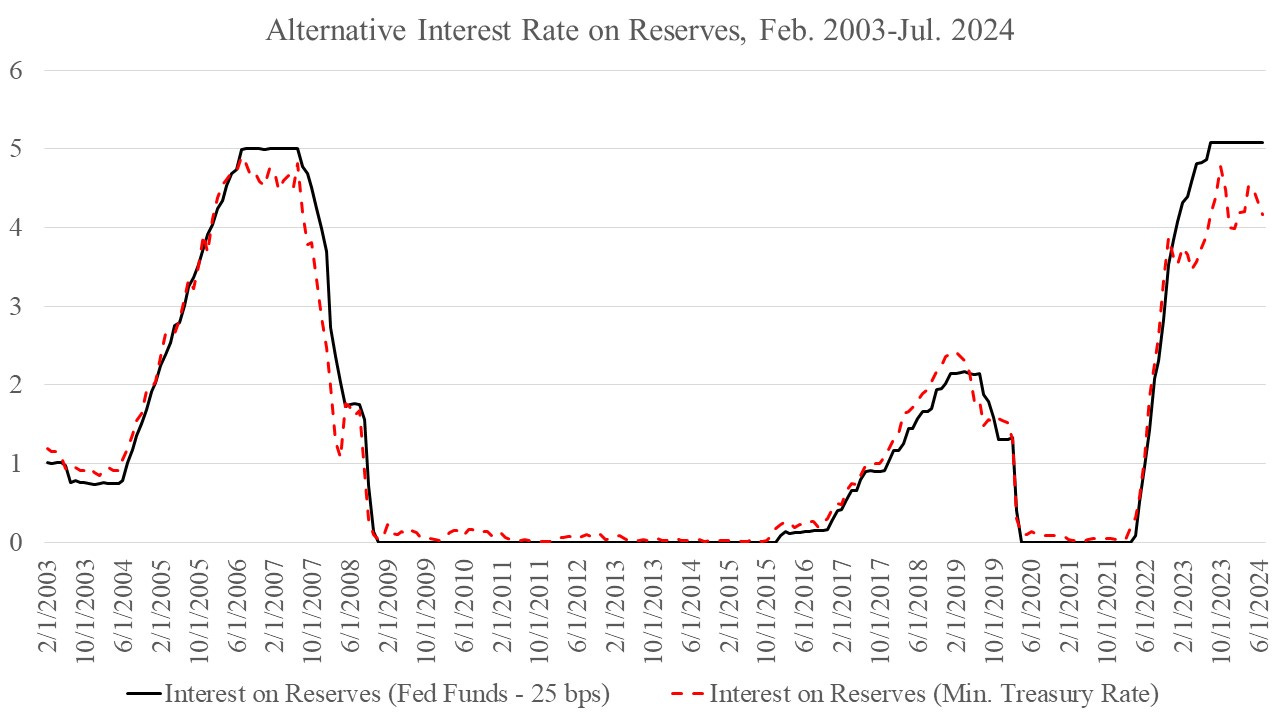

Of course, if we do not bring back reserve requirements, that might also determine whether banks continue to source funds from the overnight lending market that operated under the previous Corridor operating system. Indeed, former Richmond Fed President Jeff Lacker in comments to the Shadow Open Market Committee last year suggested moving to one policy rate, namely in rate of interest on reserves. Accordingly, I depict two alternatives for an interest rate on reserves.

The first is one inspired by Stephen Williamson’s description of the Canadian version of the Corridor operating system. He notes that their equivalent of the Discount rate was just 25 basis points (a quarter of 1 percent) above the interbank lending rate, while the rate of interest on reserves deposited at the Bank of Canada was just 25 basis points below the interbank lending rate. [Incidentally, Williamson also points out that the Canadian interbank rate is a secured rate, while the Fed Funds rate in the US is not.]

A second alternative is inspired by Jeff Lacker’s suggestion for a single policy rate, namely the rate of interest on reserves. To limit arbitrage preferences for reserves over Treasuries, perhaps you could set it equal to (or slightly below) the monthly average of the minimum daily par rate from the Treasury yield curve; during the sample depicted, the lowest value for this constructed rate equaled 0.0033 percent. If you did something like this, the Discount rate would reflect a premium relative to the rate of interest on reserves.

Final Thoughts

The Corridor operating system with a positive rate of interest on reserves makes sense from a bank’s risk-reward perspective. In designing a new operating system, it also makes sense to keep track of the consequences arising from distortions due to risk-based capital requirements. If we just had a simpler capital regime, with no risk-based capital requirements and just a total equity relative to total asset or total liability leverage ratio in place, banks would likely keep lower reserve balances under a new Corridor operating system with positive rate of interest on reserves. That’s because reserves, like interbank loans would have the same capital treatment as all other assets, including Treasuries, mortgage-backed securities, other securities and all types of loans, but would offer a lower reward. That too, makes sense from an economic perspective. Politically, however, that does not seem likely right now. Either way, the rate of interest on reserves currently seems too high, while zero seems too low; keeping it somewhere in between these values does make economic sense.