From the Fed’s Corridor to the Floor Operating System... & Back?

In this three-part blogpost mini-series, I’ll discuss the Federal Reserve’s (Fed’s) past and current operating system for the conduct of monetary policy and simple ways to reform it; my discussion will also highlight how bank capital requirements distort bank balance sheets. Before I discuss ideas for reform, I’ll begin here with a brief history of how the Fed conducted monetary under the “Corridor” operating system prior to the crisis in 2008 and finish by discussing how bank capital requirements distort bank asset holdings. In the next blogpost, I’ll discuss the current “Floor” operating system, which has also changed the banking landscape in certain important ways and has also recently resulted in Fed losses and quiet calls for reform. In the last blogpost, I’ll discuss simple ways to reform the Fed’s operating system.

The Conduct of Monetary Policy

The Fed for many decades used open market operations (OMOs) to conduct monetary policy. If the Federal Open Market Committee (FOMC), from which the Fed’s monetary policy decisions emanate, wants to conduct expansionary monetary policy, it buys securities from primary dealer banks, while crediting reserves to those banks. If the FOMC wants to conduct contractionary monetary policy, it can sell securities to primary dealer banks, while reducing their reserves. For the Fed, expansionary/contractionary OMOs mean both the Fed’s assets and liabilities increase/decrease as the policy’s implemented. For banks, OMOs simply change their asset mix between securities and reserves. I’ll next introduce the more recent Corridor operating system and how the key policy rates define it.

The Corridor Operating System

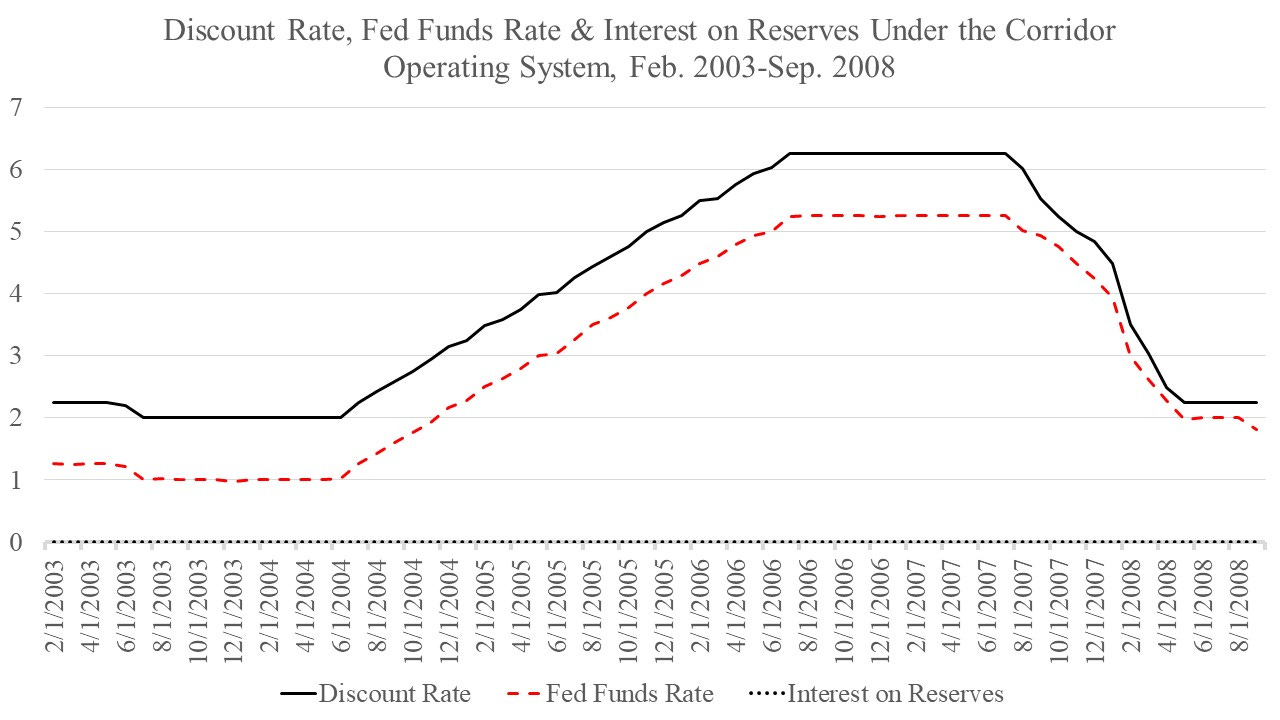

To see what I mean by the Corridor system, I’ll briefly discuss the three key Fed policy rates. The first is the Discount rate, which is the “penalty” rate at which banks facing “liquidity” issues, but with good collateral, can borrow from the Fed’s Discount Window. This is the oldest of the Fed’s lender-of-last-resort instruments. The second key policy rate is the Fed Funds rate. For many decades the Fed required banks to hold required reserves to meet depositor withdrawals, and the Fed Funds rate was the rate at which banks with required reserve shortages would borrow from banks with required reserve surpluses; today, the interbank lending market in the US is virtually non-existent under the current Floor operating system, which I’ll discuss in the next post. Lastly, there’s the interest rate on reserves, which banks deposit at the Fed and until 2008 this equaled zero.

For empirical purposes, I’ll depict the monthly average Discount rate series from the Federal Reserve Bank of St. Louis. I also depict the monthly average effective Fed Funds rate series, where “effective” means the “volume-weighted median of overnight federal funds transactions”, which can differ from the Fed’s target; use of the median reflects the distribution of rates for banks operating in this market, as safer/riskier banks would get charged a lower/higher rate. The figure below depicts the three series from 2003-2008 under the Corridor operating system. The Discount rate often lay below the effective Fed Funds rate prior to 2003. From 2003-2008, the Fed Funds rate remained in a corridor between the Discount rate at the top, and the rate of interest on reserves, which equaled zero, at the bottom.

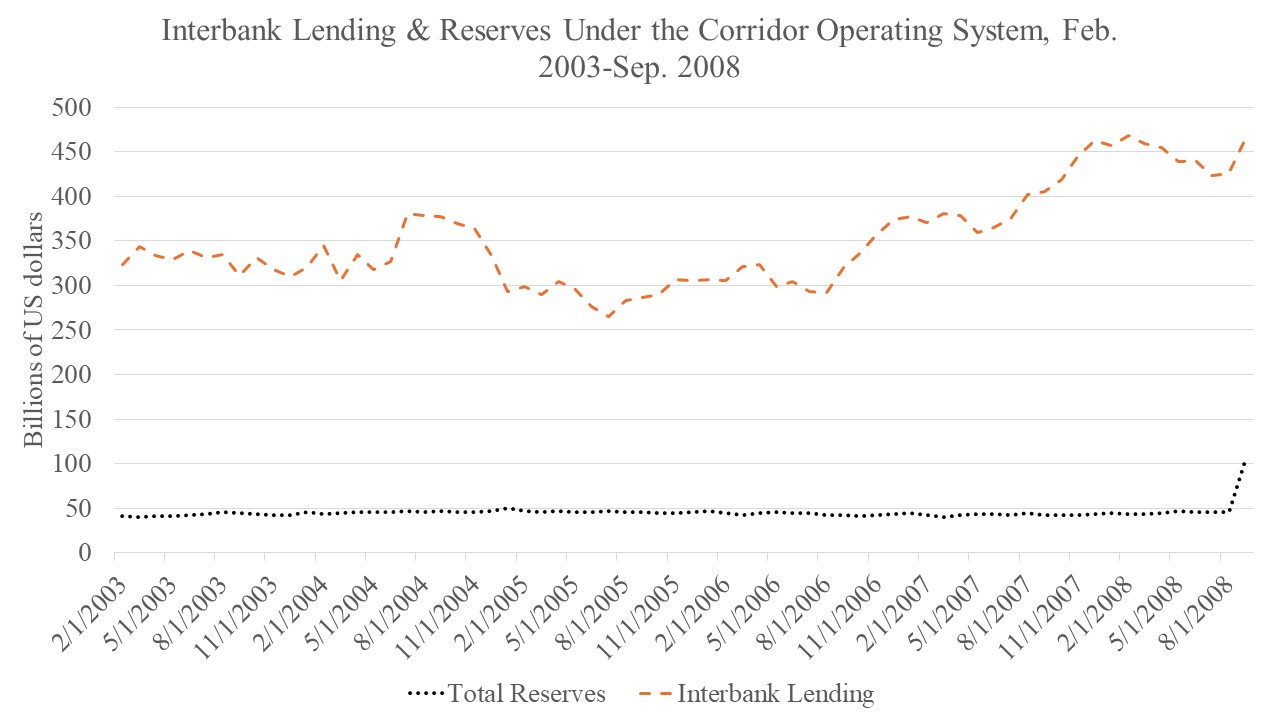

With the rates ordered as above, the figure below depicts the volume of interbank lending at the Fed Funds rate, as well as the volume of required reserves that banks had to keep. The differences in the volumes of interbank lending and reserves largely reflected the differences in returns banks could earn from each asset at that time.

Why Not Pay Interest on Reserves?

While the Fed had long paid no interest on reserves, George Selgin in his book Floored! observes that in discussions leading up to the passage of the Federal Reserve Act, payment of interest on reserves was actually debated, but not adopted. One reason why you might want to pay interest on reserves, is because if you do not while requiring banks to hold reserves to meet customers withdrawals, as was traditionally the case in the US, then the zero rate of interest effectively becomes a tax on deposits, which gets passed onto depositors.

After inflation rates began rising in the 1960s and 1970s, some at the Fed periodically attempted to get Congress to support efforts to allow them to pay banks interest on reserves. However, the US Treasury always countered such efforts due to concerns about losing remittances from the Fed, since payments of interest on reserves would otherwise go to the Treasury. But all of this was about to change as the crisis in 2008 unfolded. I’ll end this first blogpost with a brief discussion of bank capital requirements for the asset classes discussed here, namely Treasuries, mortgage-backed securities, interbank lending and reserves.

What Of Capital Requirements?

Because monetary policy and bank regulation/supervision have different aims (the former for overall price stability and full employment while the latter for banking system stability), you do not often see discussions of monetary policy together with bank regulation. I will, therefore, end this blogpost by showing how they relate in the context of the Fed’s operating system. If you have a look at Davis-Polk’s comparison of the US implementation of Basel I and Basel III guidelines, especially on numbered pp. 43-46, you’ll see that exposures to asset categories in the Fed’s operating system have among the lowest capital requirements. Under US Basel guidelines, to be adequately capitalized, a bank has to have a risk-based capital ratio of at least 8% (to be well capitalized a bank has to have at least 10%). The 8% (or 10%) number applies to standard commercial loans. However, some assets have lower capital requirements due to their having lower risk-weights.

For instance, assets with a risk-weight of 0 or 0.2 would have a capital requirement equal to 0% (=0*8%) or 1.6% (= 0.2*8%), respectively. For a bank, reserves and Treasuries are assigned a risk-weight equal to 0, which means banks do not need capital to back them. Mortgage-backed securities and claims on U.S. depository institutions and credit unions, such as interbank lending, have a risk-weight of 0.2, which means banks need to have at least 1.6% capital to back them. Also, keep in mind that the largest banks tend to have the highest risk-based capital ratios, but do not need as much actual capital to achieve that because they tend to hold a larger volume of low risk-weight assets, including the ones listed here, than smaller banks.

With this in mind, given that reserves did not pay interest under the Corridor operating system, that would suggest that banks would have preferred Treasuries to reserves under that system. Also, even though interbank loans had a higher risk-weight/capital requirement of 0.2/1.6% than reserves, which equal 0, given that the Fed Funds rate was above interest on reserves, you would expect a bank to prefer interbank lending to holding reserves, too. This would all change under the Floor operating system that I’ll discuss next.