Historical Perspectives On the Size of Recent Bank Failures

Several years ago, I wrote an op ed and a policy brief to make the point that political discourse sometimes focuses on the “record profits” in banking, when from an economic point of view, nominal dollar values lose their meaning if you don’t account for inflation and you may want to scale by firm equity or assets. Once you adjust for inflation or firm assets, the numbers can tell a very different story, and the notion of “record profits” loses its meaning. The same principle applies in the context of recent bank failures.

For example, headlines point out that SVB’s failure was the second largest bank to fail in US history behind Washington Mutual in 2008, until First Republic surpassed that. However, when comparing bank failures over time: 1) inflation results in greater nominal values for many economic series reported in dollar values, and 2) the banking sector has grown over time. As a result, focusing on nominal dollar values, as in the case of “record profits” has little meaning.

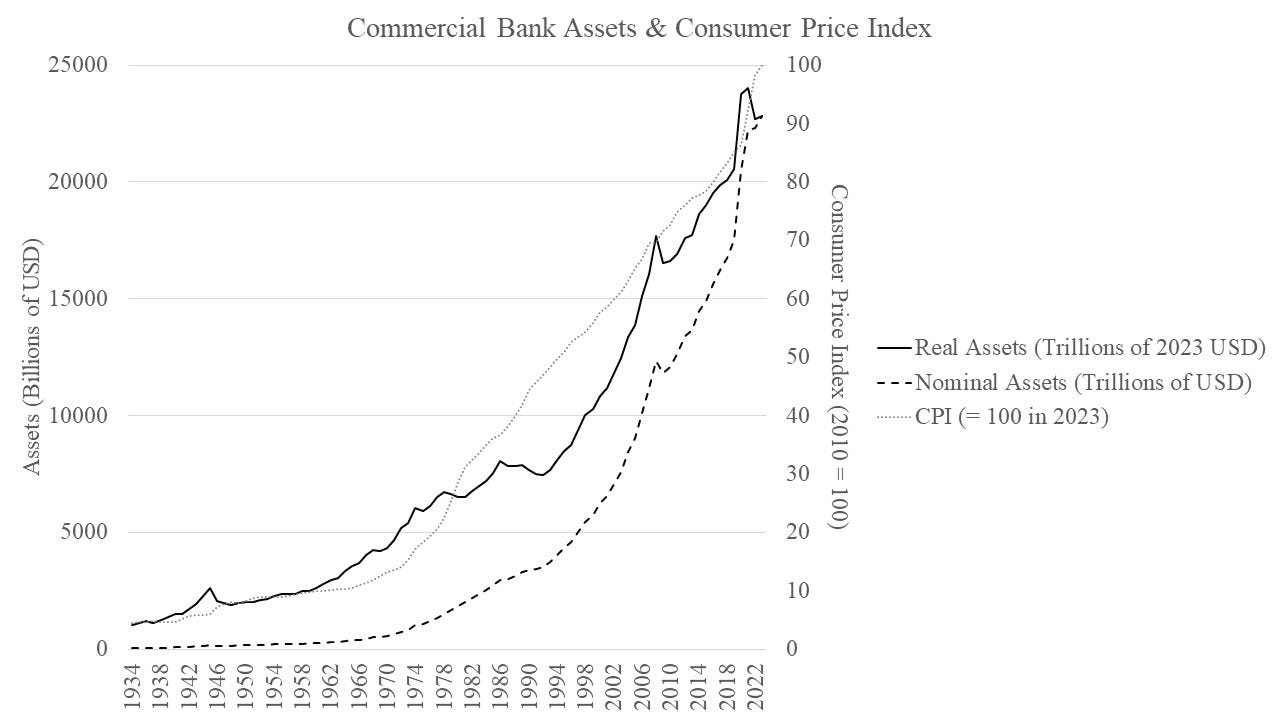

The Commercial Banking Sector, like the Consumer Price Index Grows Over Time

The figure below depicts the total current dollar commercial bank assets from 1934 to 2022, and billions of March 2023 constant dollar commercial bank assets on the primary axis; in real terms, total commercial bank assets have grown from $1.05 trillion to $22.82 trillion. On the secondary axis, the figure depicts the December values of the consumer price index (CPI) from 1934 to 2022, and for March 2023. In short, since 1934 commercial bank assets in real terms have grown almost 22-fold and prices as measured by the CPI have grown nearly 23-fold.

Comparing Recent Bank Failures to Other Noteworthy Failures

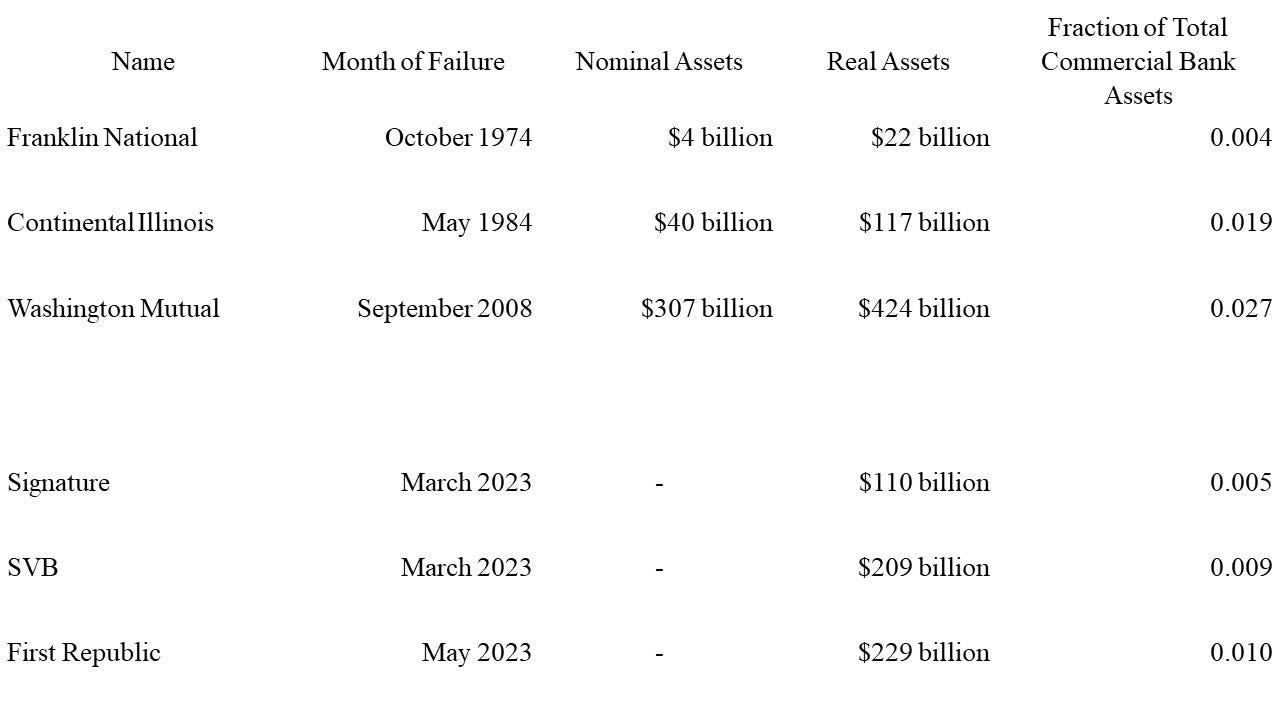

Now to put the size of the three recent failures in perspective, the table below lists the nominal or current value of assets for six noteworthy banks that failed, including the three recent failures, as these nominal values tend to make their way into the headlines. The table also lists the equivalent in March 2023 constant dollars as well as the fraction of total banking assets held by each of the six banks. From the Federal Deposit Insurance Corporation’s (FDIC’s) failed bank list, the three past failures include: 1) Franklin National, one of several bank’s that failed in 1974, which led to the formation of the Basel Committee on Banking Supervision, 2) Continental Illinois in 1984, after which the term “Too Big to Fail” became popular, and 3) Washington Mutual, the largest commercial bank to fail in the US. First Republic, SVB and Signature had about 1 percent, 0.9 percent and 0.5 percent of all assets.

The table shows that Washington Mutual was by far the largest of the six banks, with assets that would have equaled $424 billion in March 2023. However, its assets made up only 2.7 percent of total commercial banking assets in September 2008. In real terms, the March 2023 dollar value of Continental Illinois’s total assets were comparable to Signature’s at $117 billion, but its total assets equaled 1.9 percent of total commercial banking assets in May 1984. Franklin National’s total assets would have been equivalent to $22 billion in March 2023, and its fraction of total assets equaled 0.004, a little smaller than Signature’s fraction of total banking assets. All told, the recent failures were small when compared with Washington Mutual’s, but more importantly, none of the banks held a large fraction of the commercial banking system’s assets.

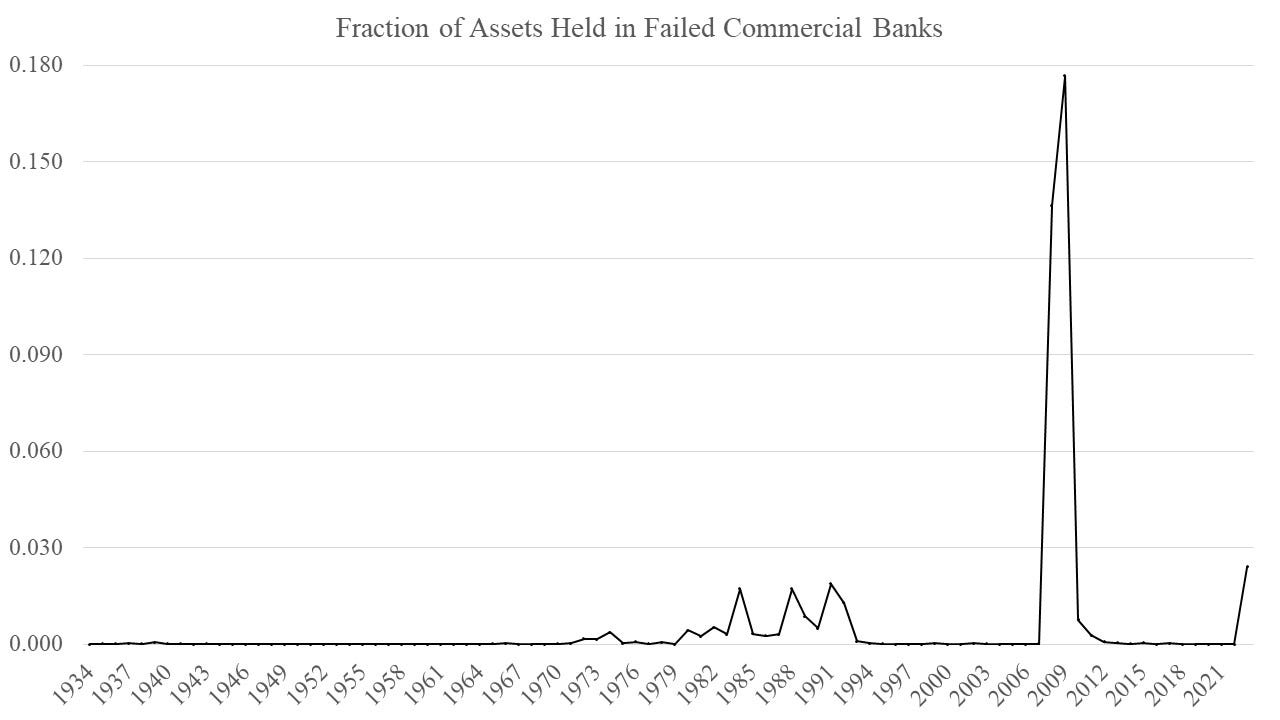

Since the FDIC was Established, What Fraction of Total Assets Have Failed Banks Held

As a last exercise to put banking crises since the FDIC was established in perspective, I depict the fraction of total banking assets that were held by failed commercial banks in each year. The figure shows that assets held by failed banks in 2023 equaled about 2.7 percent of total commercial bank assets. That figure pales in comparison with fraction of total assets held by failed commercial banks during 2009 when it equaled 17.7 percent in 2009 and in 2008 when it equaled 13.6 percent.

Some Concluding Thoughts

Much like the notion of “record profits”, the idea of reporting the “largest bank failure” when measured in nominal dollar values can lose its meaning once you adjust for inflation, or more importantly, when you compare a bank’s assets with the size of the entire banking system’s assets. The results here suggest that SVB’s, Signature’s and First Republic’s failures were perhaps not systemic. Counterfactuals aside, the assets held by banks that failed appear to have represented a small part of the commercial banking system.