How and Why Bank Capital Addresses Concerns About Crises

Nearly 10 years after the 2007–2009 crisis, policy experts and academics still debate how to end the “too-big-to-fail” bank problem. The problem concerns whether or not large banks may be large enough to bring down the financial system, and bank capital has always offered a solution to the problem.

While the roots of the “too-big-to-fail” bank problem go back over a century, the problem is relatively recent. The Dodd-Frank Act has as a stated objective ending “too-big-to-fail”, however, much of Dodd-Frank, aside from addressing government failure during the recent crisis, aims to address “too-big-to-fail” through regulator discretion rather than market dynamism and discipline. Sections 606 and 607 of Dodd-Frank do call for changing the language in bank regulatory code from banks being “adequately capitalized” to “well capitalized”.

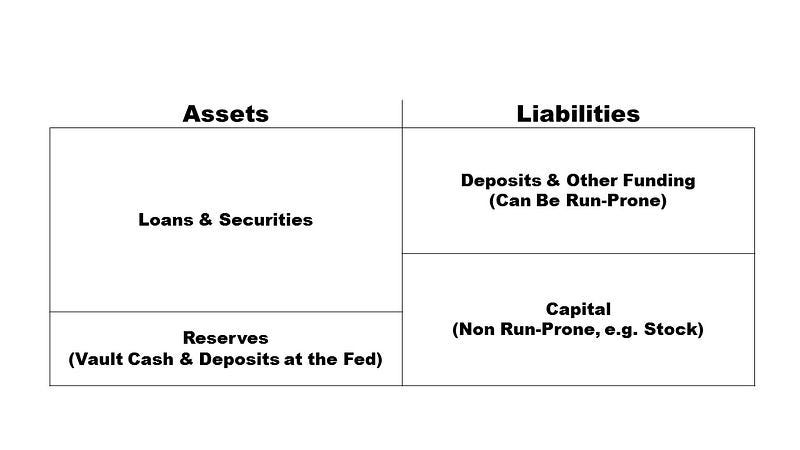

In spite of recent contributions, such as Anat Admati and Martin Hellwig’s, mystery still shrouds capital in policy debates. To see how capital fits in the picture, consider the bank balance sheet displayed above. When a bank wants to originate loans or purchase securities (these are the bank’s assets), it raises funds, the most typical being deposits (checking & savings deposits but also time deposits, such as certificates of deposit, which are the bank’s liabilities). In more recent times, banks have also relied on short-term debt such as repurchase agreements (a.k.a. REPOs, a collateralized form of borrowing) and commercial paper (an uncollateralized form of borrowing).

Many of these sources of funding may be prone to runs. As John Cochrane explains in a recent paper, the run-prone nature of some forms of bank funding arises because they are fixed value claims (you deposit $x, you’re entitled to $x back) that are redeemable on a first-come, first-served basis. You can think of capital as non run-prone bank funding, such as common stock (or even longer term bonds).

With that brief summary of what capital is, keep in mind what it isn’t. Capital does not mean plant and equipment, which economists typically discuss when describing production inputs for non-financial corporations. Also, capital is not reserves (a bank’s vault cash plus its deposits at the Fed); as the figure above shows, reserves are on the asset side of the balance sheet. Finally, you sometimes even hear people use the term “capital reserves”, but that’s misleading, too, since that too suggests capital lies on the asset side of the balance sheet.

Beyond what capital is and is not, a key issue that arises is how to measure it. In practice, capital is measured at historical book value, however, book value fluctuates less than market value. Capital measured at market value (e.g., the current price for share of common stock multiplied by the number of shares outstanding) fluctuates more. The reason is that any losses on the asset side might cause the bank’s stock price, and hence the market value of the bank’s capital, to decline. That tendency for market value to fluctuate more than book value would tend to foster market discipline, since the corporate finance side of the bank would have to pay close attention to any risky activities that might result in the bank experiencing losses.

Once you know what capital is, and how to measure it, the next step, from a regulator’s point of view, might be to establish minimum capital adequacy standards. Since 1988, the Basel Committee on Bank Supervision, located within the Bank of International Settlements in Basel, Switzerland has provided a forum to formulate guidelines to establish capital adequacy.

However, the “Basel” guidelines and U.S. regulatory implementation of those guidelines, have grown increasingly complex. James Barth, the Lowder Eminent Scholar in Finance at Auburn University, and I have written a working paper on this. The complexity has made navigating capital requirements challenging for banks; the complexity works against competition, favoring instead larger, incumbent banks.

If the current complex regulatory capital requirements have worked against having a competitive U.S. banking system, the next question to ask is whether increasing a simpler higher equity capital-to-asset (or perhaps capital-to-liability, as the FDIC did in the 1930s) leverage ratio has benefits that exceed the costs. James Barth and I have written a working paper on this, too.

We find that the benefits of a higher leverage ratio arise from the lower probability of a banking crisis, which in turn lowers gross domestic product. The costs arise from the potentially higher funding costs implied by a higher equity capital requirements, since that might require that banks retire some debt and instead issue new shares of stock, which may be relatively more expensive. That’s debatable.

The logic behind the increased cost arises from banks passing off the higher financing costs to the borrowers, which would result in less real capital formation, thereby lowering gross domestic product. It turns out that under a wide variety of assumptions, if the leverage ratio were increased from the 2014 U.S. required regulatory value of 4 percent to 15 percent, the benefits almost always equal or exceed the costs.

We choose 15 percent because a recent study found that under certain conditions that can be an optimal leverage ratio. Also, the 2013 Brown-Vitter bill selected that value, although that applied to “megabanks”, whereas our baseline case examine all banks.

Similarly, step 1 of the recent Federal Reserve Bank of Minneapolis plan to end “too-big-to-fail” calls for increasing bank capital ratios to 23.5 percent of risk-weighted assets, which corresponds to a 15 percent leverage ratio. Of course, the Minneapolis Fed plan is more complicated, and I have reservations about whether such a complicated plan applied to a select number of banks is sufficient to end “too-big-to-fail”.

Professor Andrew Jalil recently showed that crises prior to the Great Depression were frequent, but short-lived. At the same time, Professor Eugene White shows that while banks failures prior to the Great depression were not costly, the costs of bank failures since then have skyrocketed, and this has coincided with the weakening of double liability. So what works against the “too-big-to-fail” problem? Measures such as double/triple/unlimited liability for bank shareholders, simpler, higher capital requirements, and no restrictions on interstate and branch banking.