How Many Words Might Basel III Endgame Add To Current Bank Regulation?

Right now, there’s no way to know for certain how much more verbose and complex a US Basel III Endgame final rulemaking would make existing bank regulation listed in the Code of Federal Regulations (CFR). However, my colleague Patrick McLaughlin, a pioneer behind RegData, which uses machine learning to extract word counts, regulatory restrictions and other measures of regulatory complexity from the CFR, informed me that you can make a simple educated guess of the effects based on word counts.

To do that, you first do a simple word count on everything in the preamble of the US Basel III Endgame notice of proposed rulemaking (NPR). As per the Federal Register, that would mean counting all of the words from Agency just below the title of p. 64028 until the section “V. Impact and Economic Analysis” on p. 64167 of the NPR, since everything from that point on does not concern the actual rulemaking. Doing so yields 143,896 words. However, those pages also include 174 of the 176 questions that prospective commenters are asked to provide answers for to help regulators decide on the merits and drawbacks of the NPR, as well as alternative suggestions. Those 174 questions account for 11,120 words. Netting them out gives a total of 132,776 words of additional regulatory language for banks.

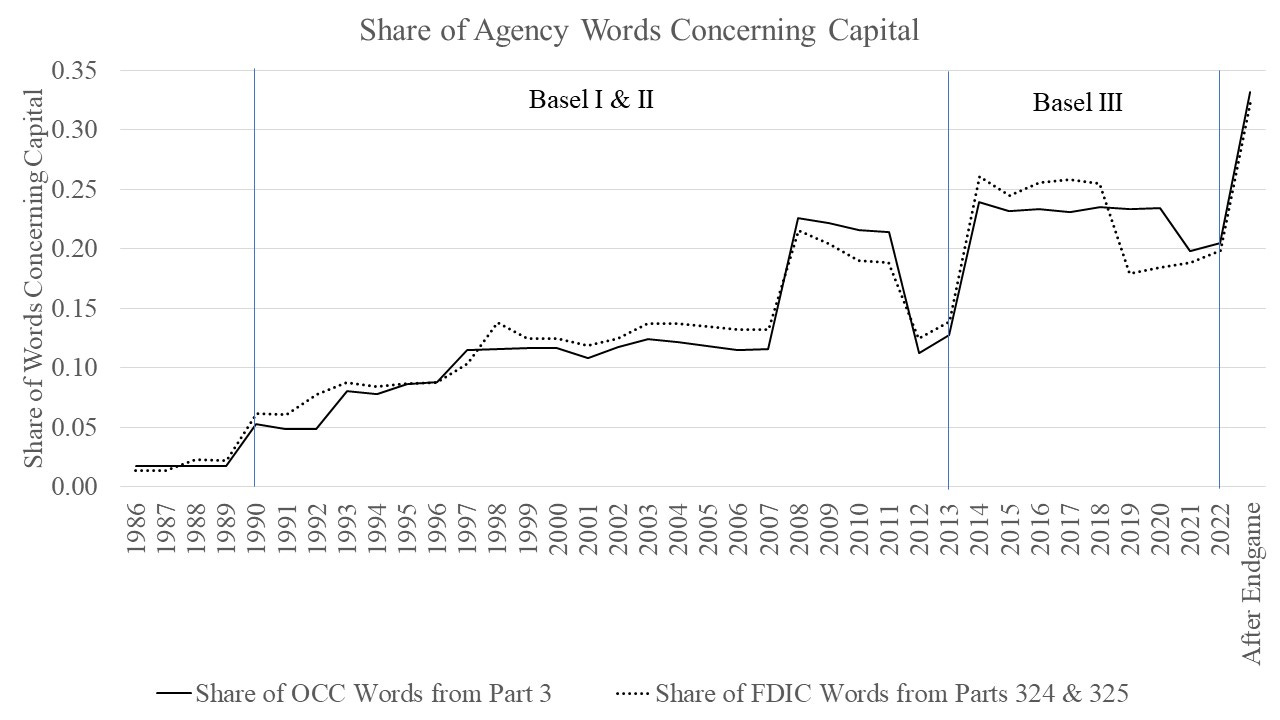

At the end of 2022, Title 12 of the CFR had 696,240 words that concerned the Office of the Comptroller of the Currency (OCC) in Parts 1-199, and 715,163 that concerned the Federal Deposit Insurance Corporation (FDIC) in Parts 300-399. Of those words, for the OCC 142,332 concerned capital (Title 12, Part 3 of the CFR), and for the FDIC 142,031 concerned capital (Title 12, Parts 324 & 325 of the CFR). That means Basel III Endgame could increase the total CFR words that concern the OCC to 829,016 and nearly double the total words for the OCC that concern capital to 275,108. Similarly, the Basel III Endgame could increase the total CFR words that concern the FDIC to 847,939 and nearly double the total words for the FDIC that concern capital to 274,807.

In terms of shares, through 2022, about 20 percent of all words in the CFR for the OCC and FDIC concerned capital. When compared with the shares in the 1980s, the dramatic growth reflects the growing complexity of the Basel-style capital requirements since they were first proposed and implemented. If you now add in what Basel III Endgame would do, that would increase the total number of words that concern capital to 33 percent for the OCC and 32 percent for the FDIC. That’s a dramatic potential increase from one rulemaking.

The growing verbosity and complexity of bank regulation resembles what’s happening across the government. In a recent op ed, Jennifer Pahlka, summarizes how the Department of Defense has turned to GAMECHANGER, which applies artificial intelligence (AI) to determine whether the agency complies why the enormous volume of regulation. Pahlka also suggests that in the future, AI could become a tool to simplify legislation and rulemaking, before being finalized. Likewise, Citigroup has recently used AI to improve efficiency across the bank, and even to decipher the impact of Basel III Endgame.

A simpler alternative regulatory framework would replace the multitude of risk-based capital requirements, and instead rely strictly on the leverage ratio. After all, my co-author Jim Barth and I showed that the benefits of increasing the leverage ratio from 4 to 15 percent outweigh the costs, by reducing the likelihood of a financial crisis, even after accounting from a potential cost arising from less bank lending, an issue still debated. This would mean having banks fund with more equity capital, especially the larger ones, as they rely on more debt funding than smaller banks.

Note:

After posting, my colleague Andy Vollmer, a veteran reader of proposed and final financial regulatory rulemakings in the Federal Register, raised objections to the calculation, as he thinks Code of Federal Regulation text is not comparable to text in the pre-amble of a Federal Register notice. That’s a fair criticism of the calculation. And the calculation may overstate word counts, especially if the agencies chose to eliminate some proposed changes after the notice and comment period. Perhaps the final rulemaking will add a quarter of those words (33,194) or half of those words (66,388). If so, then that would lower the capital to total CFR words for the two agencies to about 23-24 percent (175526/729434 for the OCC and 175225/748357 for the FDIC) or 27 percent (208720/762628 for the OCC and 208419/781551 for the FDIC). Either way, that’s a large and growing number of words for what winds up being just a fraction, say under 15 percent, of one side of a bank’s balance sheet.