Repo Market Disruption: Problem or Symptom?

Introduction

The Federal Reserve (Fed) relies on the repurchase market in U.S. treasuries (repo market) and its interest rate in conducting monetary policy. This past September the market experienced unexpected stress when repo interest rates increased from the Fed’s target of 2 percent to levels as high as 10 percent. The demand for cash increased while lenders stepped back. The financial industry and others have offered various explanations for what happened. Quarter-end tax payments were due and the Treasury was auctioning new debt both of which temporarily drained cash from the economy putting upward pressure on rates. In most such instances the PDs would lend into the market, keeping rates near the Fed’s target. But the (Fed) had for some time been reducing the size of its balance sheet, allowing Treasury securities and other assets to role off as they matured. This systematically reduced PDs’ excess reserves (cash) available to lend. Although excess reserves still exceeded $1 trillion, PDs explained that mandated liquidity and capital requirements caused them to hoard balances and not risk falling below minimum requirements.

Thus, the combination of fewer excess reserves and the PDs’ reluctance to lend caused a spike in rates and confusion in the market. As a result, the Fed reentered the repo market in a major way to remedy the shortfall in excess reserves and assure that the targeted repo rate would be consistently achieved. Since September, the Fed has increased its balance sheet by over $300 billion adding reserves and bringing rates to target.

These actions reflect the Fed’s decision to use what is called a floor system, maintaining “ample” reserves, in its conduct of monetary policy. But they also confirm its role as ultimate funding source for the growing public debt, if it wishes to keep interest rates from increasing as debt levels rise. What they imply for the long run health of the U.S. economy is less certain.

Primary Dealer Banks and Liquidity

Chart 1 shows bank excess reserve balances held at the Fed between the start of the Great Recession and today. This balance grew from virtually nothing to a peak of $2.7 trillion in 2015 when the Fed reversed direction and began the process of normalizing its balance sheet. This continued until September 2019, at which time excess reserves had declined to $1.3 trillion. Coincidently, it has been noted that PDs having increased their balances of Treasury securities, were bumping against limits for leveraging their balance sheets, making the funding of Treasury debt increasingly expensive.[1] The effect of these events was to cause PDs to recalibrate the amount of excess reserve judged necessary to manage daily cash needs, leading to the reduction of lending in the market and the sudden market volatility and spike in rates.

In the wake of these events it has been suggested that capital[2] and liquidity[3] constraints on PD be eased or eliminated to provide needed flexibility to lend into the market. One proposal, for example, calls for reducing the amount of cash versus treasuries required to meet minimum liquidity requirements. This would free up cash to buy government treasuries during periods of unusually strong cash demands without falling outside established prudential standards. Another suggestion is to allow reserve accounts to go negative during the day if the demand for cash to purchase Treasury securities spikes as happened in September. Such changes in the rules would add flexibility and temporarily free cash for meeting repo loans since the PDs would not be held to a “hard” lower cash balance until end-of-day settlement.

Such solutions are attractive as they appear simple and easy to implement. They enable PD banks to meet cash demands relying on increased leverage and reduced balance sheet liquidity, and to do so at relatively low funding costs. However, such solutions also reflect an industry that is heavily subsidized through deposit insurance and Fed liquidity facilities. Where market participants normally would insist on strong capital and liquidity levels to protect them from loss, they now rely on government protections. While eased liquidity rules and balance sheet leverage would facilitate larger repo balances among PDs, they also would reduce the industry’s resilience during the inevitable period of financial stress.

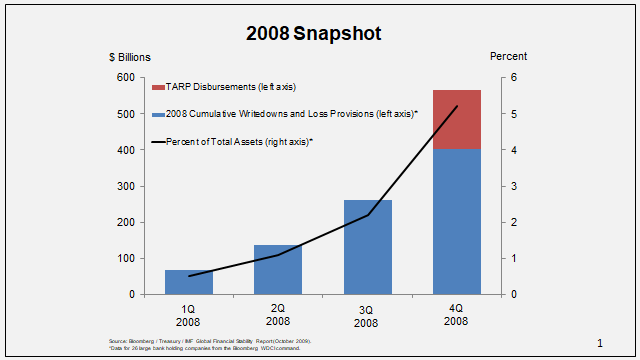

Table 1 summarizes capitalization ratios for global systemically important banks (G-SIBs). Among the ratios presented is the supplemental leverage ratio, highlighted in yellow. The ratio measures the percent of total on-and-off balance sheet assets that can become loss without the institution becoming insolvent. While over the past decade this ratio has increased, it remains only sightly higher than the industry’s losses plus government capital injections that occurred during the 2008 crisis, as shown in Chart 2. Also, while the recent dust up in the repo market was attributed to issues of liquidity, the shortfall was minor in the context of the liquidity crisis of 2008.[4] As shown in Chart 3, during this earlier crisis, the Fed provided hundreds of billions of dollars of liquidity to both domestic and foreign banks.

The disruptions within the repo market that occurred in September reflect far more than temporary or technical glitches in market operations. Over the past decade the Fed has changed how it conducts monetary policy and has made the industry increasingly dependent on the Fed’s large balance sheet for liquidity. Reacting to these disruption by having the industry operate with weaker capital and liquidity standards, thereby increasing the public subsidy, will not strengthen the financial system on a sustained basis. It simply doesn’t solve the problem.

What’s The Problem, Really?

The repo market and the PDs’ role in it are deeply intertwined with the growth in U.S. debt.

For over a decade U.S. economic policy has followed a growth strategy relying on zero or low interest rates accompanied by dramatic increases in both public and private debt. The Federal Government has led this trend as it has increased its spending, relying on ever larger levels of debt versus revenues — deficit spending. Chart 4 shows, for example, that the Federal Government, between year-end 2007, the start of the financial crisis, and the third quarter of 2019, increased its debt from $9.2 trillion to over $22 trillion. And in an economy in which Fed policy kept policy interest rates at zero, the private sector also added significantly to the economy’s debt load. Total credit for the non-financial sector, for example, increased from $24 trillion to above $31 trillion over the same period.[5] The effects of these policy choices are many but among them is that the Fed, to keep rates at zero increased its balance sheet from less than $900 billion to a peak of $4.5 trillion in 2015.

As the economy improved over the last decade, the Fed began an effort to reduce (normalize) the size of its balance sheet, which had declined to $ 4 trillion this past September. However, with the economy’s growing dependence on debt financing, this is proving increasingly difficult. Between 2017 and September of 2019, for example, while the Fed was shrinking its balance sheet, both private and public debt continued to expand. Total credit to the private non-financial sector has increased $2.8 trillion while federal government debt expanded $2 trillion.[6] Under such circumstances it is reasonable to question whether U.S. debt can expand at its current growth rate and at current interest rates without continued additions to bank reserves and an expansionary monetary policy.[7]

QE in Perpetuity?

The repo market is the current venue in which the drama of increasing debt and pressure on interest rates is being played out. PD banks are principle players in this drama purchasing and distributing government securities, and providing liquidity into the repo market. And it was in this market that the accelerating demands for cash, by public and private sectors alike, tested the willingness of PDs to provide needed liquidity. When they stepped back from doing so, the result was an increase in market volatility and significant upward pressure on interest rates.

Rather than risk an unstable market following the September repo market volatility, the Fed felt compelled to intervene and make certain that reserves (cash) was plentiful and that repo interest rate remained stable at around a 2 percent target. It immediately purchased government securities adding $80 billion of reserves into the banking system and has committed to injecting $60 billion per month through March of 2020. These actions have succeeded in calming the market. However, they also reflect a reversal in Fed plans to downsize, “normalize”, its balance sheet, and signals to the markets that its priority is to keep the Treasury debt market calm and repo rates from rising.

Despite protests to the contrary, the Fed is once again engaged in QE in which it is committed to purchasing large amounts of government securities over an extended period, adding to its balance sheet and to the industry’s excess reserve levels, and assuring a stable repo market.

If in September, the PDs’ faced only a temporary shortage of reserves, there would have been no need for the Fed to modify its basic strategy for monetary policy or ease established prudential standards. The Fed could have addressed the temporary market disturbance with short-term interventions, confident that the market would supply future needed funds. But as the Fed acknowledges with its actions, it is likely the disturbance reflected the combined effects of an unrestrained supply of public debt and significant reduction of Fed supplied excess reserves, necessitating the reversal of policy.

Conclusion

The U.S. is on a path in which large Federal deficit spending will continue well into the future, and Fed policy appears committed to assuring sufficient bank reserves to fund both expanding Treasury and private debt, to preclude likely increases in interest rates. What this means for the economy and the future path of monetary policy is highly uncertain. At the moment the economy is booming and the accommodation seems to be working. However, the economy also has the feel of 2005, when it was booming as it rode the wave of a rapid growth in debt. Today, as then, bank and economic leverage more generally are on the rise. There is no appetite for reining in U.S. fiscal deficits or for allowing rates to increase for fear that they would ration credit within the private sector and slow the economy.

Perhaps the recent disturbance in the repo market was the “canary in the coal mine”. Perhaps policy makers should heed the warning. With history as a guide, failing to do so will cause markets to become increasingly unsteady. Heeding the warning will require more disciplined fiscal and monetary policies, and sufficiently-capitalized, resilient financial firms to manage through economic adjustments that come with such discipline. Ignoring the warnings risks deepening the imbalances and increasing the inevitable economic upheaval and costs which the public will inevitably bear.

[1] Nelson, Bill, “What Just Happened in Money Markets, and Why it Matters”, Bank Policy Institute, September 18, 2019.

[2] Regarding bank leverage, the Fed, FDIC and OCC recently changed the measurement of leverage allowing banks to exclude reserves at the Fed from total assets for purposes of calculating the supplemental leverage ratio (SLR) of tangible capital to total on-and-off balance sheet assets. They also have proposed easing banks’ SLR buffer from a fixed 2 percent to a buffer calculated as 50 percent of a banks GSIB surcharge. This rule change would permit the banks to more easily lever-up their acquisitions of treasury debt.

[3] If the largest banks were to maintain tangible capital to asset ratios — leverage,- at between 10 and 15 percent, the likelihood of bank failure or bailout would decline significantly. Under these conditions there is a case to be made that government imposed liquidity standards would not be necessary. See James Barth and Stephen Matteo Miller, Benefits and Costs of a Higher Bank Leverage Ratio, Mercatus Working Paper, Mercatus Center at George Mason University, Arlington, VA, 2017.

[4] Barclays, Rates and Credit Research, “Proposals to address repo market fragility,” November 7, 2019. While much is made of the shortfall in available funds, this article notes that the repo market in Treasuries is one in which the levered investors (e.g. hedge funds) would have been able to cover their positions with minimal or no loss and would have adjusted future fund demand had the Fed not intervened.

[5] Source for Non-financial credit is the Bank for International Credit and Federal Reserve Bank of St. Louis.

[6] Source: Bank for International Settlements — Total Credit to Private Non-Financial Sector

[7] While the federal government prefers lower to higher interest rates, it will fund itself independent of the level of rates. The private sector, however, is sensitive to interest rates, and as they rise, borrowers are rationed from the market, placing added pressure on the Fed to fill the gap. Also, interest rates are affected by changes is domestic savings and foreign flows into the United States. However, U.S. savings levels have long failed to meet U.S. demands for capital. For example, between 2017 and 2019 Gross Private Savings for the U.S. increased from $4.041 trillion to $4.690 trillion. The availability of foreign savings also has become less certain with the rise of trade conflicts between the U.S. and the rest of the world.