The Costs of Crises Revisited

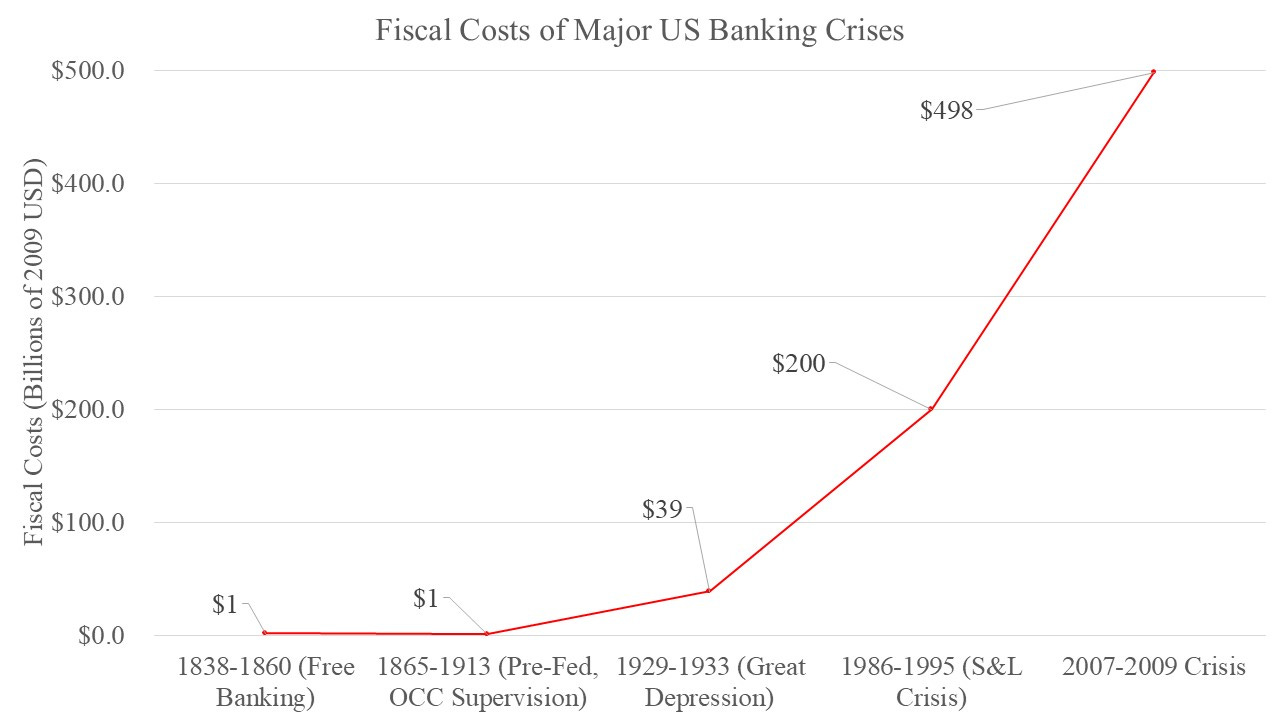

[Note: I revised the graph below. Eugene White reports the costs of crises figure as $1.9 million in 1838-1860 dollars for the “Free Banking” period is similar in magnitude to the $1 billion in 2009 reported for the 1865-1913 period. A quick check on the https://www.measuringworth.com/calculators/uscompare/ suggests the values may have been lower than $1 billion in 2009, but I have rounded up the figure to $1 billion and revised the graph accordingly.]

In a FinRegRag post in 2017, I wrote about how the costs of banking crises have grown over time and how that arises from diminishing market discipline in banking. After briefly summarizing the distinction between “direct” or fiscal costs and economic costs of crises, I update the estimates from the earlier blogpost and then provide some estimates of the economic costs of crises for the 11 major banking crises that have happened in the US before concluding.

Why Revisit and Update?

The estimates of the costs of crises I previously reported came from pp. 29-31 of a study by Eugene White, which concerned how Discount Window lending created incentives for weak banks to stay around longer, making the Great Depression so costly. White points out that rather than voluntarily liquidate, as most closed banks did prior to the creation of the Discount Window, banks leading up to the Great Depression had a reason to stay open longer (and eventually to fail), which made it the mostly costly crisis; reforms since have not restored that pre-Discount Window market discipline.

Most estimates of the costs of crises that White reports measure fiscal costs, but without a readily available estimate of the fiscal costs at the time of its publication for the 2007-2009 Crisis, White turns to a Gross Domestic Product (GDP)-based economic cost measure. Deborah Lucas has since provided an estimate of the “direct” or fiscal cost of that crisis in Table 2 of a recent study, which I use to update the graph I previously reported, which otherwise confirms what White argued, as the (fiscal) costs of crises have been rising over time.

Also, the late Jim Barth and I recently had our last co-authored study on “U.S. Financial Crises and Growing Federal Oversight of Banking” accepted for publication in the Elgar Encyclopedia of Financial Crises, in which we provide estimates of the economic costs of the 11 major US banking crises going back to the Panic of 1819. This gives me an opportunity to show how the US has done since the 19th century, both from a fiscal and an economic perspective.

“Direct” or Fiscal vs. Economic Costs of Banking Crises

In a 2002 study, Hoggarth, Reis and Saporta estimate and compare the costs of banking crises from a fiscal and an economic cost perspective. Fiscal costs measure the monetary value of the resources used by the government to resolve any failing institutions during a crisis; these can reflect transfers to bank equity and bond investors. The economic cost measures forgone opportunities across the economy due to a crisis; numerous ways to do this exist. The approach Jim Barth and I use measures deviations from trend real GDP growth. In sum, the fiscal costs can help to monitor how a government manages a crisis given available resources, while the economic cost approach helps to monitor how disruptive crises are to economic activity.

Updated Fiscal Costs of Crises

In my previous blogpost, I only reported the costs of crises for the 1865-1913 period, the Great Depression, the Savings & Loan (S&L) Crisis and the 2007-2009 Crisis. I did not include the estimated costs that White reports for the 1838-1860 “Free Banking” period. Also, for the 2007-2009 Crisis, rather than fiscal costs, White reports the economic costs in terms of foregone GDP estimate, equal to $1.7 trillion in 2009 dollars. Deborah Lucas provides a suitable replacement for this estimate of the fiscal costs of the 2007-2009 Crisis equal to $498 billion, with $311 billion of that coming from Fannie Mae and Freddie Mac alone. The greater costs reflect the government’s greater scope of intervention. The graph below accordingly updates my previous graph by including the 1838-1860 “Free Banking” Costs as well as Lucas’s recent estimate of $498 billion. While smaller than the estimate based on forgone GDP, the graph still shows that the fiscal costs of crises have been rising, as White claimed. Using the numbers that Jim Barth and I reported, I can also provide a comparable series for the economic costs of crises.

Economic Costs of Crises

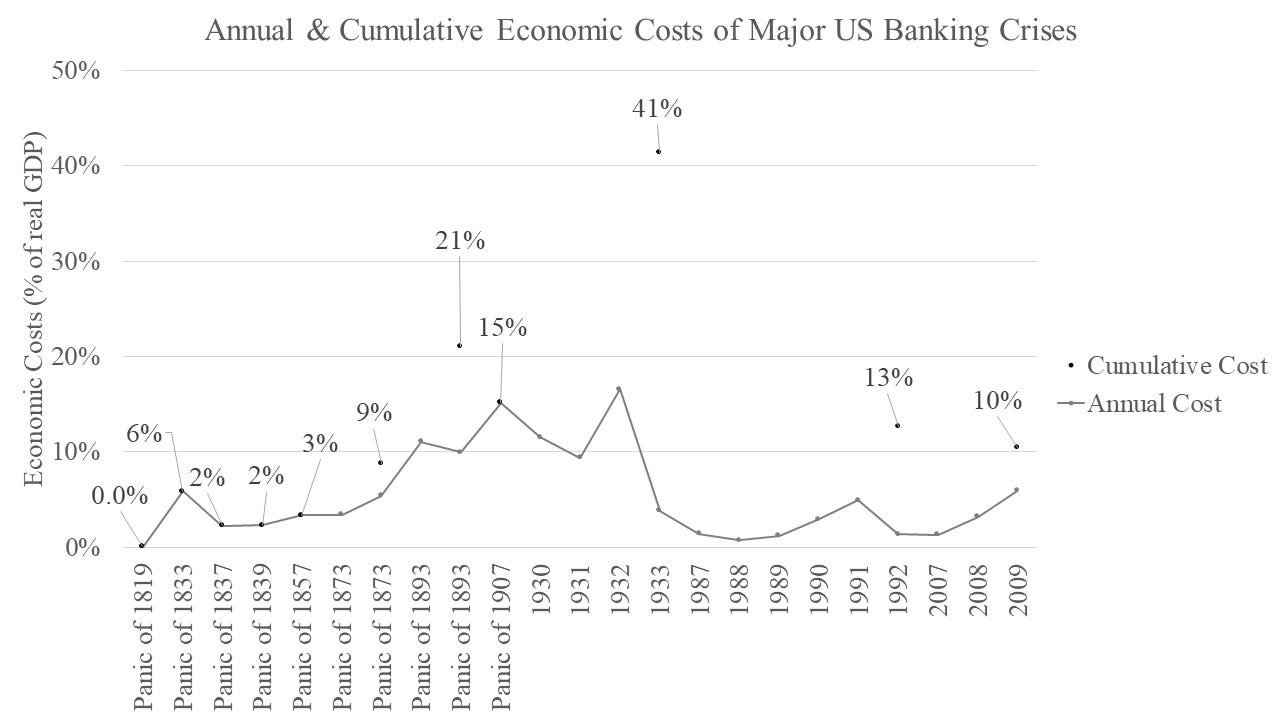

To estimate the economic costs of crises, I use Hoggarth, Reis and Saporta’s GAP1 measure, given that I can apply it to all major US banking crises. GAP1 sums the differences between the growth rate of real GDP for each year during a crisis and a measure of potential real GDP growth computed as the average real GDP growth rate in the three years prior to the crisis. For the GAP1 measure, the end of the crisis occurs when the real GDP growth rate exceeds the pre-crisis potential real GDP growth.

The graph below depicts the cost of a crisis for the Panic of 1819 (see Hugh Rockoff’s discussion), for the major crises that Andrew Jalil identifies in 1833, 1837, 1839, 1857, 1873, 1893, and 1907, for the Great Depression, for the S&L Crisis and for the 2007-2009 Crisis. The graph depicts both the economic cost of a crisis in a given year using the gray line and also the cumulative costs across all years of a particular crisis using the black points to compare crises that lasted longer than one year with crises that lasted under one year. I make this distinction because Jalil shows that crises prior to the Great Depression tended to be seasonal in nature, lasting less than one year, the exceptions being the Panics of 1873 and 1893. Also, using Jalil’s crisis dates, note that the potential GDP estimate for the Panic of 1837 includes the effects of the Panic of 1833 as that spilled over into 1834, while the potential GDP estimate for the Panic of 1839 includes the effects of the Panic of 1837.

When ranked in terms of economic costs, the Great Depression remains the most costly banking crisis at about 41 percent of annual real GDP. The Panic of 1893 comes in a distant second at just over half the cost of the Great Depression at 21 percent of annual real GDP. The Panic of 1907 comes in third place at 15 percent of annual real GDP. The S&L Crisis comes in fourth place at just under 13 percent of annual real GDP; note that this estimate reflects the length of the crisis more than the real GDP losses, which in most years were more comparable to the costs during crises of the 1830s. The 2007-2009 Crisis comes in fifth place, at about a quarter of the cost of the Great Depression and about half of the cost of the Panic of 1893. Overall, these estimates suggest that even if less frequent, the duration of crises since the 19th century has grown, and crises become more costly in terms of real GDP losses.

Concluding Thoughts

The duration of banking crises and the costs of banking crises, whether measured in terms of fiscal costs or economic costs, have been higher than since the early decades of the US. In the 19th century, US banks funded with more equity than today, and shareholders were often subject to contingent liability, such as double, triple or unlimited liability. Higher equity capital funding and contingent liability likely contributed to the low costs of banking crises, even as prohibitions on interstate banking made banking crises more frequent in the US, as Michael Bordo, Angela Redish and Hugh Rockoff highlight. Today it’s the opposite, as banks fund with relatively little equity and the shares are subjected to single (limited) liability, but banks are now allowed to operate across state lines. It stands to reason that steps to reduce the duration and costs of crises include more equity funding, perhaps with greater penalties for failed banks, combined with more interstate banking.

Note: I slightly altered and split the first paragraph under Why Revisit and Update? to better summarize Eugene White’s discussion of the effects of the Discount Window, and corrected a few typos.