The Effects of Monetary Policy Under the Current Floor Operating System

In 2008 during the crisis, the Federal Reserve (Fed) began implementing “unconventional” monetary policy called Quantitative Easing (QE). Since conventional monetary policy tended to move shorter-term rates, QE aimed to stimulate the economy by lowering longer term rates through an expanded Fed balance sheet. On the asset side, the Fed from 2008 to 2014 began large scale asset purchases of longer-term mortgage-backed securities and US Treasuries, and on the liabilities side, the Fed accommodated this in part with “ample” reserves, on which the Fed would now pay interest. Doing so meant that the Fed would have to change its operating system, which effectively moved the rate of interest on reserves above the Fed’s traditional target Fed Funds policy rate, such that the Fed Funds target would now generally serve as the floor rate. What finally led to the change?

How We Got to the Floor Operating System

Change was in the works soon after Ben Bernanke became Fed Chair in February 2006, as Congress finally began efforts to get the Fed to pay banks interest on reserves by October 1, 2011 with Section 201 of the Financial Services Regulatory Relief Act of 2006. However, this initiative got fast-tracked as the financial crisis began to unravel in 2008, and Congress hastened the introduction of interest on reserves by almost three years to October 3, 2008, in Section 128 of the Emergency Economic Stabilization Act of 2008; incidentally, that’s the same act that gave us the $700 billion Troubled Asset Relief Program or TARP. With the passage of this act and the payment of interest on reserves, the Fed implemented the Floor system.

Comparing the Corridor to the Floor Operating Systems

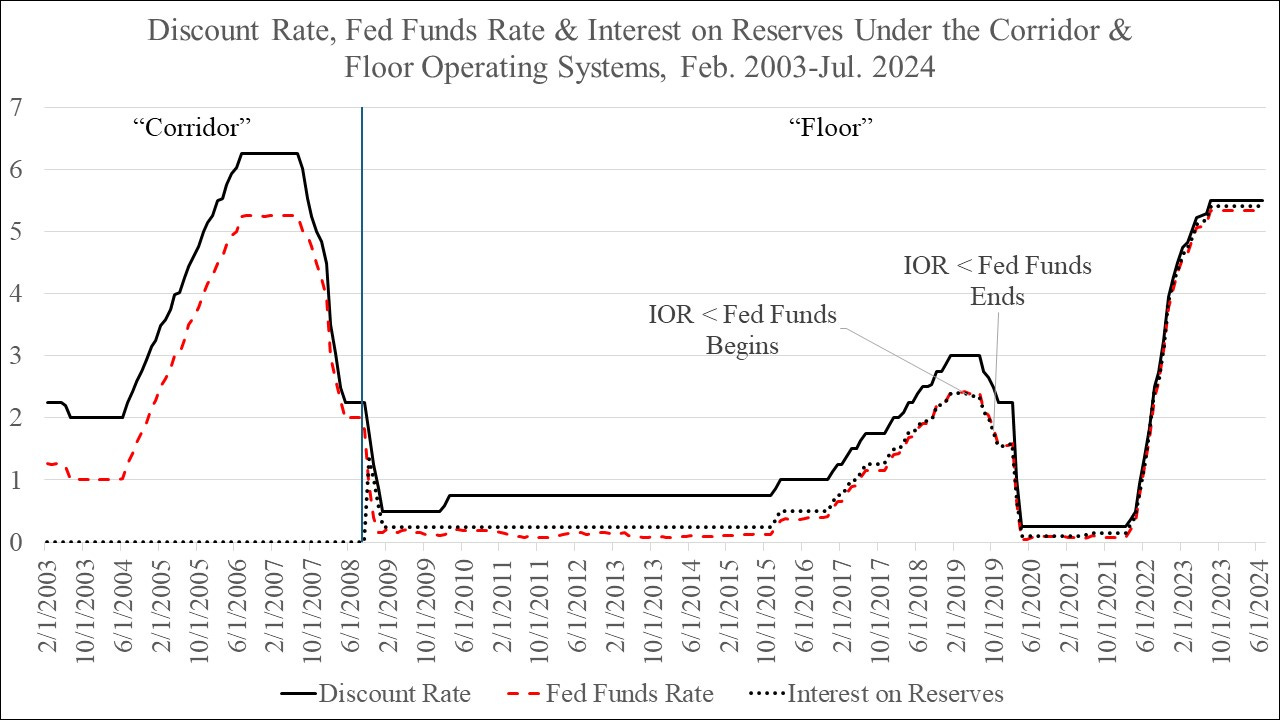

The figure below extends the figure depicting the key rates in the Corridor from my previous post through July 2024. What you’ll notice is that under the Floor system, the Fed Funds rate since 2008 generally lies slightly below the rate of interest on reserves; one exception is the brief period in 2019 that I highlight when the rate of interest on reserves was below the Fed Funds rate.

[Note: Initially, the rate on required reserves exceeded the rate on excess reserves so the Fed originally listed a series for rates on required reserves and a series for rates on excess reserves. However, in 2020, the Fed abolished reserve requirements and as there’s no longer any distinction between required and excess reserves, the Fed now reports just one series. The figure, therefore, depicts the rate on required reserves through 2020 and the rate on reserves since then].

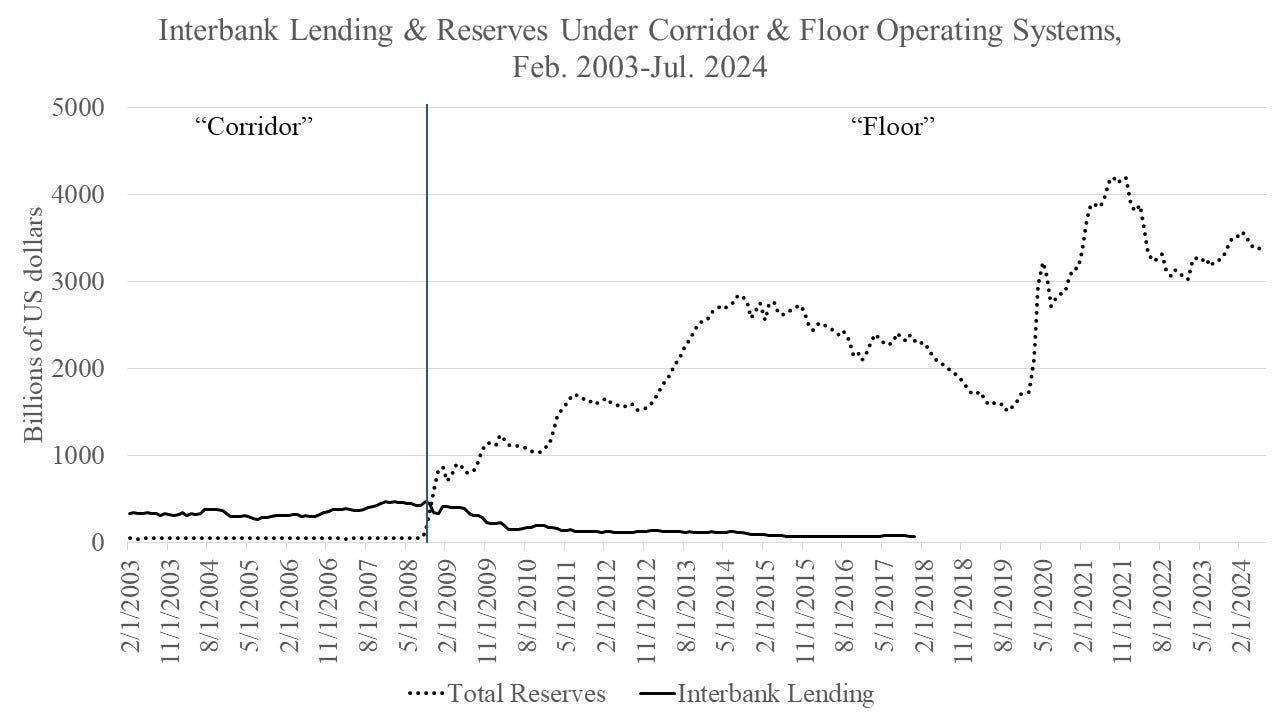

This change from the Fed Funds rate moving within the Corridor to serving as the floor rate, also dramatically affected interbank lending and reserves as the figure below, which extends the figure on interbank lending and reserves from my previous post through July 2024, shows.

Under the Floor operating system, the volume of total reserves dramatically overtook the interbank lending market, which effectively no longer exists (it’s now dominated by the Government Sponsored Enterprises). This change came not just from the rate differentials, due to the Fed Funds rate now being slightly lower than the interest rate on reserves, but also from risk-based capital requirements.

Recall from my previous post that under risk-based capital requirements, interbank loans also had a small capital requirement of 1.6% (as they have a risk-weight of 0.2), while reserves have no capital requirements (they have a risk-weight of 0). So while reserves paid relatively lower rates of return than interbank loans under the Corridor system, now reserves earned a slightly higher rate than the Fed Funds rate and as they did not require capital, banks could use reserves to increase the slack in the capital buffer. The once highly useful interbank lending market no longer provides the information on counterparty risk for banks that it once provided. Banks now “lend” to the Fed rather than to other banks. I suspect that reviving the interbank lending market would be a good idea, and there may be good reasons to return to a Corridor. Nonetheless, the higher rates of interest on reserves in the aftermath of the Fed’s fight against inflation resulted in last year’s Fed losses.

What Explains Fed Income/Losses?

With the 2008 crisis over and QE having ended by 2014, some economists, including Peter Ireland, began calling for eliminating payment of interest on reserves, noting the risk arising from having to raise policy rates to higher levels that might exceed what the Fed earns from long term assets. A St. Louis Fed blogpost briefly discusses how the Fed has historically generated income for the Treasury, as its assets tend to generate more income than the costs arising from its liabilities. However, that can change under the Floor operating system, as Peter Ireland pointed out (see also Table G.10 on numbered pages 208-210 of the Federal Reserve’s 2023 annual report, especially the “Current income”, “Net expenses” and “Distributions to the Treasury U.S. Treasury” columns ). Last year as earnings on assets declined relative to the Fed’s policy rates, including the rate of interest on reserves, the Fed’s net expenses grew more more than current income. The Fed accordingly reported a $116 billion loss instead of the typical positive remittance to the Treasury. Tempting as it may sound to return to the original Corridor system, I believe it does make sense to pay interest on reserves, but doing so in a Corridor system does not have the problem of the Floor system, as I’ll discuss in my next blog post.