The Ever-Evolving Policy Framework: What’s Next?

The Federal Reserve (Fed) has adopted the policy framework in which it manipulates both the price of money and quantity of money, expecting better outcomes for economic growth and employment. This policy framework began during the last half of Alan Greenspan’s chairmanship of the Fed and was greatly expanded by each Fed chair following him. Under the framework monetary policy can include a zero-interest rate policy (ZIRP) and the unrestricted creation of money through the purchase of securities across the yield curve, quantitative easing, or QE. The effect of this framework has been to balloon the Fed’s balance sheet and commercial bank reserves. The policy evolved as the Fed expanded its focus beyond price stability to financial stability and full employment. It also specifically narrowed its inflation focus to price inflation of goods and services, ignoring asset inflation, which enabled the expansionary policy to run longer than it otherwise would have.

Inevitably, inflation has followed such a policy, and the question now is how the economy will do as the framework is applied in reverse. My view is that the inertia of the past two decades makes using the framework to slow the economy far more difficult than is assumed by the Fed and others. The Fed, in the end, will err on the side of inflation rather than risk price and asset deflation and difficult financial volatility.

The Evolution to QE and the ZIRP

The first and in some ways most significant change in the Fed’s operating framework came in 1971, when the U.S. abandoned having an external discipline (gold standard) to constrain government spending and monetary and interest rate policy.

At that point, the U.S. went with a central planning Federal Open Market Committee (FOMC) of 12 individuals with the sole control of the policy framework. Policy discipline would be self-imposed, subject to political pressure, and the record is not good, given that the Fed allowed itself to become increasingly responsive to political pressure in its management of monetary policy.

The current framework, QE and ZIRP, began to evolve during the second half of Greenspan’s chairmanship of the Fed, as he became increasingly an interventionist. In Jackson Hole, WY, he made it explicit that the Fed would not head off asset bubbles but would rather clean up the aftermath if they burst. His bailout of the markets became recognized as the Greenspan Put.

The Asian financial crisis began in July 1997, followed by the Russian financial crisis in August 1998, and both are examples of his policy path. Again, in early 2001 the U.S. suffered a recession as the dot-com bubble collapsed and the Fed came to the rescue.

During the Asian and Russian liquidity crises, the FOMC lowered the fed funds rate from 5.56% to 4.8% in Q1 1999. It did reverse its rate trajectory after reaching a high of 6.5% in Q3 of 2000. But then the dot-com bubble burst. True to Greenspan’s commitment to wait for the asset bubble to pop and then clean up, the FOMC quickly increased bank reserves and systematically lowered rates. It was also during this period that the FOMC began telling the market that it would hold to an accommodative stance for “a considerable period.”

The fed funds rate was lowered to 1% by Q2 2004 and was kept there for the remainder of year, even as growth accelerated.

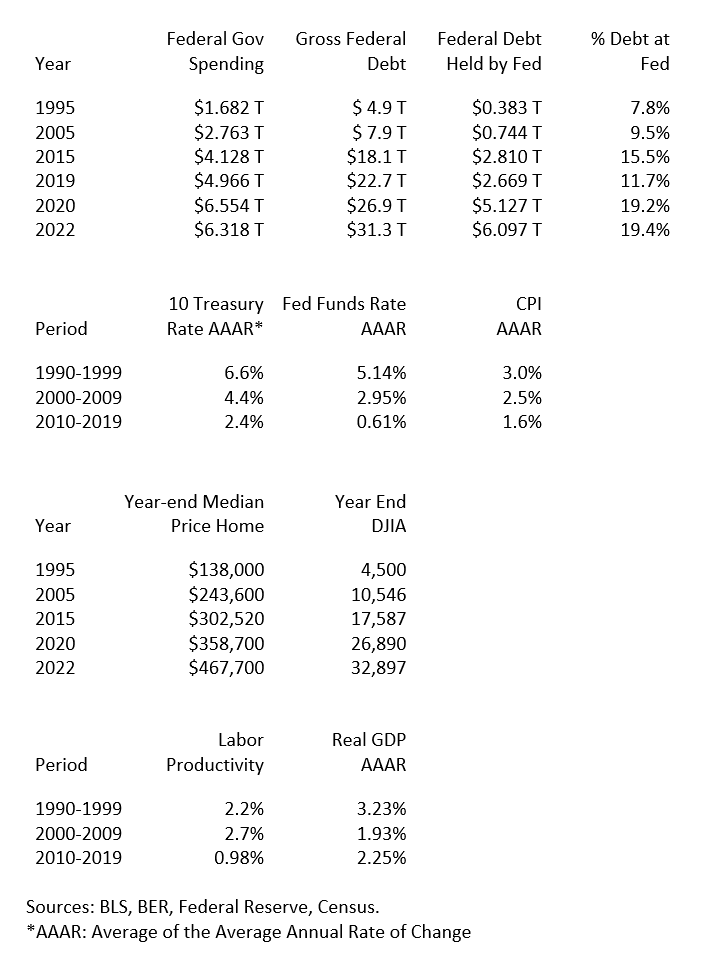

The Fed’s Treasury holdings increased from $507 billion to $685 billion, a 35% increase in balances. Also, bank reserves more than doubled, from less than $6 billion to more than $12 billion.

This practice of keeping interest rates exceptionally low for an extended period and increasing bank liquidity, contributed to the asset bubble centered around housing and eventually the Great Recession.

Following the Great Recession, and the liquidity infusion—QE—that served to stanch it, the FOMC, rather than cautiously restoring its balance sheet and raising the fed funds rate toward a neutral position, doubled down on its policy prescription and began massive increases in Treasury and mortgage-backed security (MBS) purchases and the creation of nearly an unlimited supply of liquidity into the financial markets; and it systematically suppressed the yield curve, keeping short term rates near zero.

QE2. In 2010 the FOMC began the first noncrisis massive injection of $600 billion in liquidity into the financial system.

QE3. This policy was continued in 2012 at the rate of $40 billion per month; that amount was quickly raised to $84 billion per month through 2013.

QE4. In September 2019, what I call QE4, the Fed intervened with QE again as the repo interest rate spiked, threatening highly leveraged hedge funds that had been borrowing extensively in the repo market. In this instance, the Fed began purchasing $60 billion of securities per month and continued doing so through March 2020.

QE5. Finally, the pandemic caused the Fed to take QE to a new level. Starting in March 2020, the FOMC began purchasing Treasuries and MBSs at the rate of $120 billion per month, and did not completely cease doing so until March 2022, when inflation—this time both in assets and consumer prices—increased to a 40-year high.

Thus, from 2007 to 2015 the Fed expanded its use of QE and increased its balance sheet from less than $1 trillion to over $4 trillion. Then starting with the repo crisis in September 2019, continuing through the pandemic, and ending in March 2022, its balance sheet more than doubled to $9 trillion.

Side Effects of Framework

Beyond its own balance sheet, this massive expansion of the Fed’s framework enabled the federal government to finance its spending through ever larger deficits, relying on the Fed’s willingness to grow its balance sheet and to pursue ZIRP. By keeping interest rates at zero and below the natural rate of interest, it encouraged, as intended, speculative investing and increased asset inflation that changed the dynamics of the U.S. economy.

Below I note just some of the data that coincide with the evolution of this policy framework.

The Fed’s ZIRP and QE policy framework has reshaped policy expectations. The Fed has come to dominate debt markets as it has stepped in to bail out markets in almost every economic slowdown or crisis over the past two decades. It has enabled the government to fund its ballooning debt at low rates and has facilitated its massive spending initiatives. Exceptionally low rates, below the natural rate, have encouraged large scale speculation in financial markets and have been a source of asset inflation. For all its intervention, however, the U.S. has not seen a systematic acceleration in real growth.

The Fed Policy Framework Forward

Looking forward, the Fed says that controlling inflation is its primary objective, and it has said repeatedly that although disinflation appears to be showing its presence, the Fed is nowhere near ready to declare victory. It keeps reminding the world that labor demand remains exceptionally strong and wage demands are putting upward pressure on prices. It also argues that inflation has found its way into the core measure of inflation, which removes food and energy from the measure and which has fallen less the overall inflation. All this is true.

Fed Chair Jerome Powell has said that he is taking a Volcker-like approach to policy. In other words, despite these challenges, the Fed will risk a serious recession rather than see inflation reignite in 2023 and beyond. Rates will remain elevated, and the Fed’s balance sheet will be reduced until inflation is certain to return to 2 percent. This promise has yet to be tested.

Making these bold statements is being done in the face of major impediments to its policy. The federal government’s spending commitments and borrowing needs forward continue to expand enormously. The federal government still spends over $6 trillion per year and will do so well into the future. It may run trillion-dollar deficits in perpetuity, given current political conditions. Finally, the Fed will come under enormous pressure to help fund these deficits to keep the market liquid and keep the government’s interest costs contained.

If the Fed stays with its policy commitment and raises the fed funds rate and shrinks its balance sheet (not increasing its purchase of Treasuries or other assets), the government’s borrowing cost will trend higher and put additional upward pressure on the cost of borrowing in the private sector as well. This will almost certainly slow the economy and increase the risk of recession. Add to this a banking crisis and the odds of a recession multiply.

The Fed is at the proverbial fork in the road. Over the past two decades, it has established a fed funds equilibrium for the economy near zero. The government and markets have come to expect a compliant Fed willing to purchase government debt and satisfy the financial sector’s liquidity needs to fund that debt. With the outbreak of price inflation, it shifted toward a tighter money policy. However, aggressive as it might appear, policy remains, relatively speaking, only mildly restrictive. The real fed funds rate, for example, remains negative. More rate increases appear necessary. The Fed’s balance sheet remains bloated in the range of $8.5 trillion. Under these conditions the Fed must tighten further. The question then becomes whether—under mounting pressure and amid the risk of a faltering economy (with the potential for a recession and financial crisis)—the Fed will once again employ ZIRP and QE to save the day regardless of where inflation stands at the time.

With consumer price index (CPI) inflation declining in February to 6.0 percent, I am confident the Fed has intensified internal discussions around what the terminal fed funds rate should be and when and at what speed it might start to lower rates. Also, despite its commitment to risk a recession to bring inflation down, how serious a recession it is willing to accept is unknown. How these discussions go and what surprises the Fed encounters will affect the Fed’s employment of its operating framework forward.

These evolving discussions and how they unfold come with two significant risks for the markets and public.

The first risk is that the Fed is aware of the market’s skepticism of its resolve. To regain credibility, it has messaged that it will accept a recession to assure the return to 2 percent inflation—the Volcker solution. In its zeal to show its commitment to this goal, it may raise rates too high or keep rates elevated too long, and it may shrink its balance sheet at all costs, destroying demand, undermining consumer and business confidence, and discouraging investment. Inflation would decline more quickly toward 2 percent but at a cost of a deeper recession with a significant loss of jobs and income. At that point the Fed would find itself struggling to regain control of its policy and the economy.

This is a likely outcome given the policy pattern that the current Fed chair has followed since joining the FOMC.

This course introduces the second risk, which concerns how the Fed will react to the political and public pressure that comes with a likely economic recession. The Fed says repeatedly that it is committed to its Volcker-like policy. However, as the economy slows and unemployment increases, politicians, Wall Street, and the public will press the Fed relentlessly to ease policy, even if inflation slows only modestly from its current level. The Fed’s pattern has been to give these groups what they want. There is no policy rule to follow or to use as a guide.

Over the past two and a half decades the Fed’s reaction function has been to reverse and “do whatever it takes” to avoid recession or bail out the financial industry. Thus, if the economy falls into a recession or experiences a financial panic, the Fed will not only lower interest rates, but will fire up QE and inject substantial liquidity into the system to stabilize markets. Also, as the federal debt continues to grow, the Fed will be pressured to provide the liquidity to fund it. Wall Street, Congress, and the public have come to expect this from the Fed. It is frankly difficult to imagine the Fed will change its operation unless circumstances force it to do so. Volcker-like policy came last time as a last-resort policy. This most likely will be the only way the Fed stays the course this time.

Complicating these risks are a host of external factors that will affect the U.S. and global economies. Trade friction remains an issue, and other supply bottlenecks make judging the source of inflation difficult. My observation is that seldom are new policy tools abandoned; they get refined but never abandoned.

The new monetary policy framework is manipulating both the price and quantity of money. This framework isn’t going to change easily or soon.