Why Revising the Supplementary Leverage Ratio Keeps Coming Up and What to Do About It

[Note: After uploading, I added some slight edits for clarity.]

Tom Hoenig recently wrote about how policymakers should focus on addressing debt concerns rather than eliminating Treasury holdings from the supplementary leverage ratio (SLR) to make it easier for these large banks to absorb more Treasuries. Addressing the debt should certainly be the focus going forward. While we wait for that to happen, I also think the SLR’s design has flaws. Here, I discuss U.S. Basel capital regulation, how the SLR fits in this framework, why we keep debating whether or not to exclude items from it, as well as two alternatives.

U.S. Capital Regulation and Securities Warehouses

After the 1988 Basel Accords, U.S. regulators adopted risk-based capital measures, such as the Tier 1 capital to risk-weighted asset ratio. The U.S. Basel standards were phased in between 1989 and 1992. I have long had real concerns about the intended and unintended consequences of the framework. Tom Hoenig alluded to one intended problem, namely, the creation of what he calls “Shadow Central Banks.”

For some time, I have used a different term: “securities warehouses.” I like summarizing the business of banking as “(1) making and administering loans, and (2) processing transactions” and I have no problem if banks hold securities, too. However, I do not think being a securities warehouse deserves regulatory concessions like the kind I discuss next.

Risk-Based Capital Regulation and Unintended Consequences

Risk-based capital rewards banks, especially securities warehouses by requiring little to no capital for holding mortgage backed securities (MBS), Treasuries or reserves deposited at regional Fed banks. Why? Risk-based capital regulation attempts to turn unexpected losses into expected losses, to turn “unknown unknowns” into “known unknowns”; the regulatory presumption is that these assets are virtually risk-free. However, there are unintended consequences of doing so.

Recall the spectacular distress created by the AAA-rated CDO tranche blowup that nearly wiped out market value of equity for some large banks during the 2007-2009 Crisis; the 2001 Recourse Rule created this problem by lowering risk-weights on the highest rated, private label tranches. More recently, after the 2021-2023 rise in inflation leading up to the 2023 bank failures, it was unrealized losses from AAA-rated MBS and Treasuries—not exotic securitization deals—that caused sharp declines in Silicon Valley Bank’s market value of equity.

U.S. Leverage Ratios

In addition to risk-based capital ratios, under U.S. Basel regulation, regulators subjected banks to a simple capital-to-asset, leverage ratio, a variant of which had informally been in use prior to 1989. The SLR was introduced in the aftermath of the 2007-2009 Crisis. By name, it sounds like just another leverage ratio, but the Basel Committee wanted to bring off-balance sheet items into the calculation of the total asset denominator.

While I do not usually side with industry views about bank capital, Sean Campbell at the Financial Services Forum pointed out a key problem some time ago in that the total leverage exposure measure used in the SLR denominator lacks transparency. In effect, the SLR is constructed like other risk-based capital ratios.

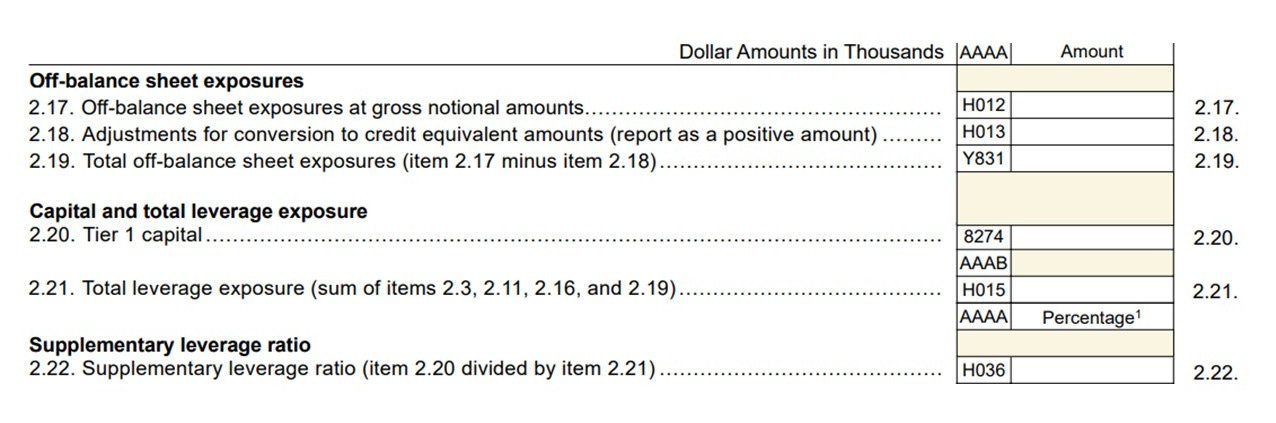

How? You can look at how the SLR is computed on p. 6 of the Federal Financial Institutions Examination Council’s “Regulatory Capital Reporting for Institutions Subject to the Advanced Capital Adequacy Framework” Form 101. The SLR (item 2.22.) divides Tier 1 capital (item 2.20.) by total leverage exposure (item 2.21.)

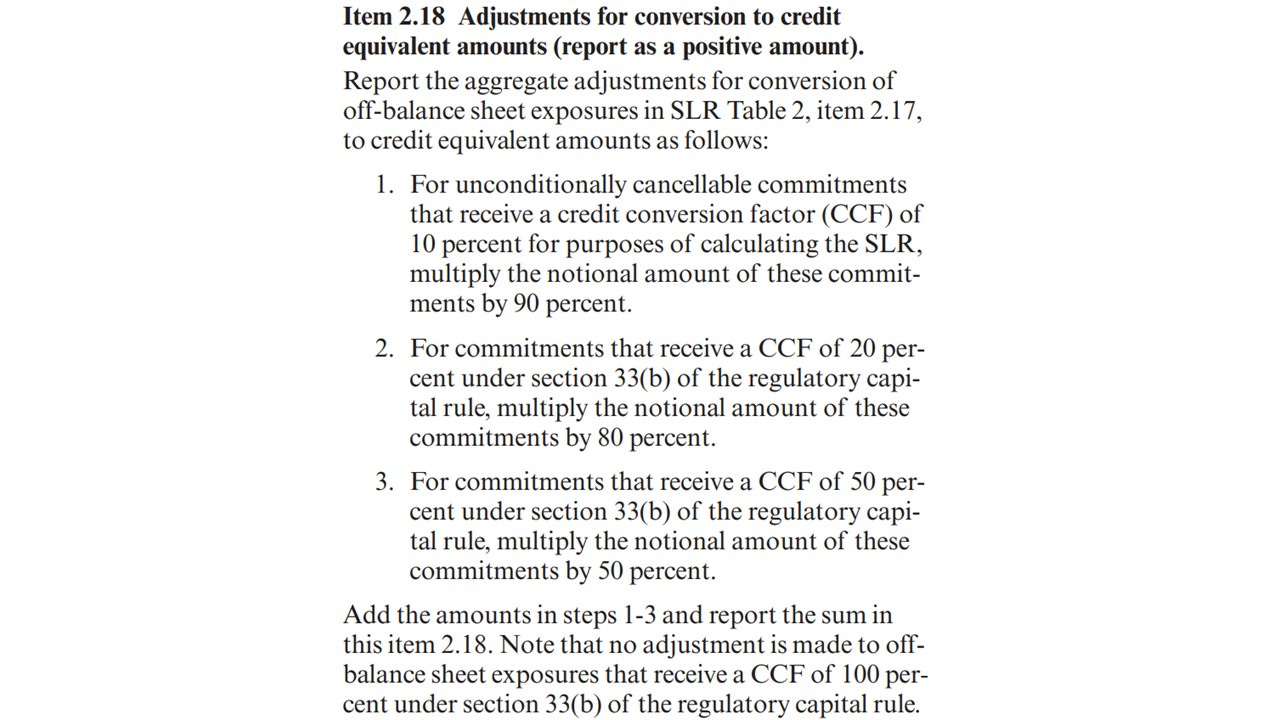

But you can also see above that that banks make adjustments to the off-balance sheet entries in item 2.18. To get a better sense of what that means, the screenshot below from p. 33 of the instructions for Form 101 for item 2.18. shows that off-balance sheet items receive credit conversion factors (CCFs), which are also used to calculate risk-weights.

As it stands, the SLR is like a leverage ratio for the on-balance sheet items, but a risk-based capital ratio for the off-balance sheet items. Moreover, if you remove Treasuries or other assets from the total leverage exposure, the SLR will become even more like the risk-based capital ratios, since now one of the on-balance sheet entries get assigned a risk-weight of zero.

Why Remove Items from the SLR?

Proposals to eliminate Treasuries and other assets from the SLR are not new. Recall that Treasuries and reserves were eliminated from the SLR during the pandemic from April 2020 through March 2021. This issue keeps coming back because the volume of Federal debt keeps growing, and the primary dealers among the securities warehouses have to buy unsold inventories from Treasury auctions. They complain that the SLR is a binding constraint, so removing certain assets, like Treasuries, from the SLR would help securities warehouses comply with the regulatory requirements. However, keep in mind that the binding nature of the SLR arises because of choices, too.

What choices? Large banks, including securities warehouses, tend not to want to increase the Tier 1 capital in the numerator. But recall that equity funding is a choice variable, not a constraint. More/less equity funding means less/more debt funding. By funding with more equity, not only would they be more resilient, but they would have more room to absorb these assets. Also, securities warehouses may not want to change their derivatives activities, which these banks can use for a variety of purposes, including hedging.

Therein lies the crux of the problem: securities warehouses do not want to fund with more equity capital and may not want to reduce certain off-balance sheet activities. Given their choices, the industry’s preferred regulatory fix involves removing certain assets, like Treasuries, from the SLR. Even if you do not believe the current SLR is yet another risk-based capital ratio, once you do eliminate Treasuries from the SLR, by construction it becomes yet another risk-based capital ratio. So what might you do instead?

Concluding Thoughts About Alternatives

Aside from addressing the growing debt burden, if regulators leave the SLR as is, one simple option, which I originally heard Cato Institute’s Norbert Michel suggest, would be to simply have more banks serve as “primary dealers.”

I wrote about another option in an earlier post, which would also address the SLR constraint issue, by changing the purpose of holding company capital requirements. In that post, I discuss the view that capital regulation should apply at the subsidiary level rather than the holding company level. Bank subsidiaries in a holding company cannot issue equity. Therefore, you could replace all existing holding company capital requirements, including the SLR, with a simple requirement that holdings companies stand ready to issue enough equity capital to ensure that bank subsidiaries always satisfy subsidiary capital requirements. Why? In Section 6 of a paper on Dodd-Frank’s Orderly Liquidation Authority, in spite of the Fed’s doctrine that holding companies serve as a “source of strength,” Paul Kupiec gives examples where holding companies failed to come to the rescue of failing subsidiaries. More recently, we saw that Silicon Valley Financial Group survived, while Silicon Valley Bank failed. With this simple holding company requirement, you could operationalize the “source of strength” doctrine, whereby the “source of strength” arises from requiring holding companies to always be ready to recapitalize subsidiaries.

In sum, regulators could side with the industry proposal, but that would entail spending more energy tweaking an already overly-complex regulatory framework to accommodate constrained banks. Instead, why not just allow less constrained banks in the market, or ditch the constraint altogether, in favor of making holding companies be an actual source of strength for bank subsidiaries?