Will St. Paul’s Rent Control Measure Bring Rents and Prices Down?

The new rent control measure approved by voters in St. Paul will be interesting to watch. I have a working theory of rents and prices since 2007, and St. Paul may be a good test for it.

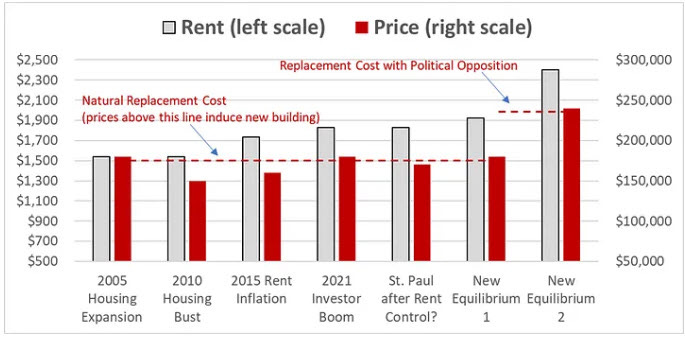

In my graphic above, before 2007, there was a home building boom. Prices were high enough to induce building, and construction was somewhat active (Housing Expansion). After 2007, lending standards were sharply shifted from previous norms. Initially, this pushed down prices in credit constrained markets, ones where potential buyers can’t borrow under current standards. It didn’t push down rents, though, because the underlying demand for shelter hadn’t diminished, only the ability to buy homes had. That means that price/rent ratios declined (Housing Bust).

Prices were too low to entice builders because existing homes could be purchased for less than an equivalent new home would cost. Tenants couldn’t pay more for homes even if rents were rising because they couldn’t get mortgages. Additionally, institutions hadn’t developed a taste for single-family landlordship as it was a market traditionally dominated by owner-occupiers who were willing to pay more for those homes. Switching to a new financial context where owner-occupiers had less funding meant that rents had to rise in those markets before new construction would return (Rent inflation).

Thus, in the aftermath of the financial crisis, rents have increased in low tier housing in the typical American city. But rent inflation hasn’t yet increased enough to induce much construction. The traditional apartment construction market has been running at a pace close to its late 20th century cyclical peaks. Entry-level single-family building, however, is dead on arrival.

But something interesting has happened recently. Low-tier home prices have recovered, and price/rent ratios have rebounded (Investor Boom). This should theoretically lead to a rebound in building. Prices should be high enough to induce more building There are complications here involving interest rates, lot prices, etc., yet this still poses a mystery: Why isn’t more low tier building happening?

Maybe it is starting to. Mortgages for owner-occupiers haven’t been loosened. The buying pressure instead seems to be coming from cash buyers and institutional buyers, and a “build to rent” market is being birthed. This seems like it could be a refutation of my intuition. Prices recovered without loosening lending, and the market could recover without owner-occupier recovery. But this is really the only way it could go, and the important issue to focus on is rents. If owner-occupier buying had recovered, prices could have naturally recovered to the past equilibrium, a lot more building could happen, and rents could decline back to lower levels.

The recent recovery in low-tier price/rent ratios is a natural market reaction to the lack of adequate building. It is still a landlord market that will settle at higher rents and a lower price/rent ratio once we reach the new equilibrium. But, on our journey from the old equilibrium to the new equilibrium, rent inflation will be unusually high until it reaches the new level. Developers are noticing that rents are rising. They are engaging in some speculative buying now because they can forecast that rents will continue to move higher. Price/rent ratios in this inter-equilibrium transition are high based on today’s rents, but not based on the eventual rent. Rent inflation is built into the forecasts, temporarily pushing up prices and moving some buying activity sooner.

Now in either case, if there isn’t a recovery of entry-level, owner-occupier lending, we will end up at the same, new high-rent equilibrium either way (Equilibrium 1).

This is where rent control and St. Paul, Minnesota comes in. My theory above assumes that we are currently in an odd temporal zone where unsustainable rent inflation is built into developer forecasts. Meanwhile, St. Paul just passed a very strict rent control law. And immediately, there appears to be a reaction among developers to halt construction. This suggests that these projects required high rent inflation to “pencil out”.

But what is the end result of that? Maybe, nothing. If “Equilibrium 1” was eventually going to be reached anyway, this could just delay some transitional buying activity and construction, but St. Paul will end up in the same place. New construction will just have to wait until it reaches that equilibrium and high rents can be charged right out of the gate.

My guess is that what happens in practice is that St. Paul ends up with even higher market rents (Equilibrium 2). This is basically where Los Angeles, San Francisco, and New York City are currently. The process for getting to “Equilibrium 2” is more the result of second-order effects. A local housing market becomes embroiled in a convoluted web that both creates economic rents and divides them up in a classic “Bootlegger and Baptist” ballet.

Eventually, owner-occupied home values, which are not limited by the rent control law, become inflated. Affordable units aren’t naturally available anymore, so “affordable” living is a favor doled out by local municipalities. New, market-rate construction rents at much higher rates than controlled units do, so every new project attracts more opposition. Locals are perpetually up in arms about those greedy developers. Anyone who supports building any feasible new projects is derided for licking the boots of the greedy developers that won’t build affordable units for “real” locals. Rent control, by itself, probably can’t get you to Equilibrium 2, but it can be an important part of the vicious cycle to dysfunction.

The problem here is that there may be no way for St. Paul to solve this problem. Even without a vicious cycle, rent will keep marching up to Equilibrium 1. It might be possible to encourage a very generous, deregulated local multi-unit market to fill in the gaps left by the diminished owner-occupier market. That might be able to drive rents back down somewhat. That would require building hundreds of thousands more apartments across the country each year than we currently do. Rent control is decidedly not a move in that direction.

It is not hard to find homes in St. Paul that could be purchased with mortgage payments estimated by Zillow to be well below the homes’ monthly rental value. Allowing those tenants to make no-brainer decisions to buy homes will increase prices, naturally induce more building, and lower rents (eventually bringing prices down, too). It will be hard for St. Paul to do that until many post-financial crisis reforms at the federal level are reversed. This appears to be a tragic example of poor public policies creating a backlash that triggers even worse policies. It also is an example of the importance of leaning toward freedom of association and freedom to contract so that emergent private solutions to economic problems are not inadvertently blocked.