You aren’t protecting consumers by denying them a choice

Innovative non-bank fintech lenders are providing better and wider access to credit for many borrowers. While this should be seen as an…

Innovative non-bank fintech lenders are providing better and wider access to credit for many borrowers. While this should be seen as an unambiguous good, emerging regulatory and litigation trends threaten a linchpin of the current model. Fortunately, there are things that Congress, federal regulators, and the states can do to protect the progress being made. A new policy paper lays out the issues and what can be done.

Many fintech lenders rely on a bank-partnership model as a workaround for obsolete and inefficient regulation. Under federal law, banks are able to make loans nationwide subject to their home state’s laws governing interest rates. This allows banks to offer a consistent product and enjoy economies of scale. Fintech lenders have partnered with banks to leverage this ability, but recent court decisions and regulatory actions have called this model into question.

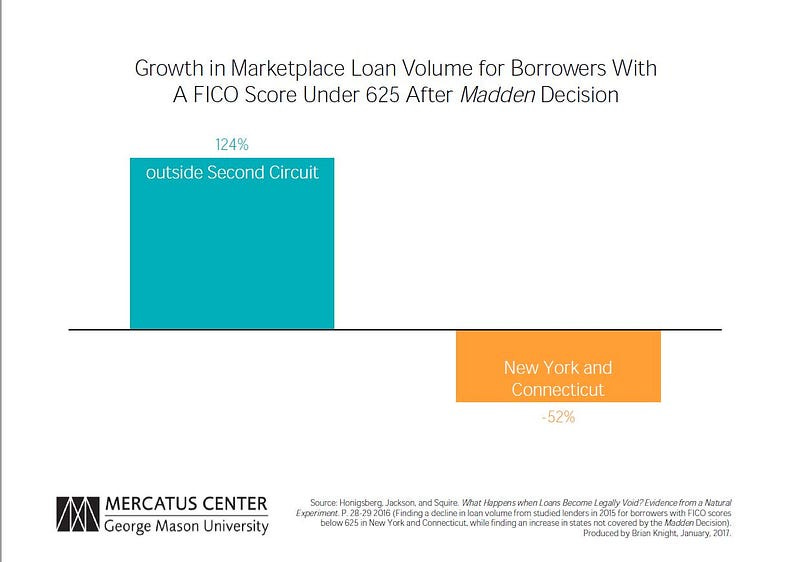

This legal uncertainty has been shown to restrict credit access. In states covered by the U.S. Court of Appeals for the Second Circuit’s recent Madden v. Midland Funding LLC. decision borrowers with lower credit scores have seen a significant decrease compared to increased access outside the Second Circuit. The very people who benefit the most from expanded access to credit are being denied it in the name of “consumer protection”. This is perverse.

Thankfully, there are steps that Congress, federal regulators, and the states can take to help preserve innovation. These include greater state coordination, extending federal interest export rules to fintechs, and allowing fintechs to become banks themselves. Every solution has its pros and cons, and should be robustly debated. But something needs to be done to allow people to continue to benefit from innovation and competition.