Bank Capital Requirement Related Regulatory Restrictions

In this post, I’ll discuss the rise of regulatory restrictions embedded in the parts of Title 12 that cover bank and bank holding company…

In this post, I’ll discuss the rise of regulatory restrictions embedded in the parts of Title 12 that cover bank and bank holding company capital requirements. I briefly discussed the basics of bank capital in a Medium post some time ago, but here just think of capital as a source of funding for a bank that is not prone to bank runs (e.g., non-deposit forms of funding, such as stock and long-term bonds).

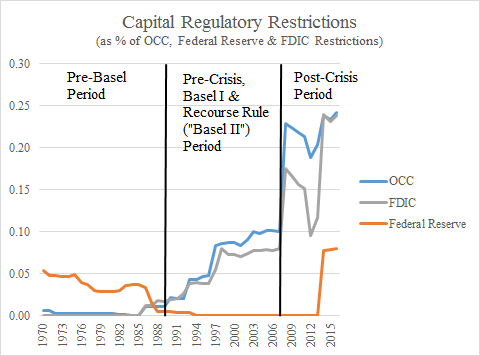

The regulations that concern capital are found in Title 12, part 3 and part 167 for the Office of the Comptroller of the Currency (OCC), part 217 for the Federal Reserve and part 324 and part 325 for the Federal Deposit Insurance Corporation (FDIC). Also, capital adequacy regulations since 1970 can be assigned to three broad periods.

The first is the so-called pre-Basel period, when U.S. regulators applied considerable discretion concerning the determination of adequate bank capital. The Latin American Debt Crisis of 1982 resulted in the International Lending Supervision Act of 1983 (Pub. Law 98-181; 97 Stat. 1278), which tasked U.S. regulators with finding a multilateral way to raise capital requirements not only for U.S. banks, but also foreign banks. That effort gave rise to the 1988 Basel Accords, sometimes called Basel I, which has opened the way for capital requirements to become increasingly complex over time, as we’ll see below.

The second period began when U.S. regulators began to phase-in the capital adequacy standards suggested by the Basel Accords in 1989 (see “Risk-Based Capital Guidelines” 54 Federal Register 4186, January 27, 1989). A key feature of Basel I guidelines was that they varied the minimum amount of capital banks need according to asset class. For instance, cash got a risk-weight of 0, agency mortgage backed securities (those created by Fannie Mae & Freddie Mac) got a risk-weight of 0.2, mortgages got a risk-weight of 0.5 and commercial loans got a risk-weight of 1. Multiplying the minimum capital ratio of 8% by the risk-weight would give you risk-based capital ratios of 0%, 1.6%, 4% and 8%, respectively, for every dollar allocated to each asset class. The original Basel I guidelines were summarized in 30 pages.

U.S. regulators made additional changes in 2001, when they finalized the so-called “Recourse Rule”, which I’ve recently written about. A key feature of that rule change was that AAA- and AA-rated mortgage backed securities created by investment banks (and other similar structured products like collateralized debt obligations) were given the same risk-weights as the agency mortgage backed securities. This change was also embedded in the Basel II guidelines, which the U.S. did not adopt by the time the crisis began to unfold. The Basel II guidelines had ballooned to 347 pages.

The third period began with the crisis in 2007. In the wake of the crisis, Basel III guidelines were unveiled to address perceived shortcomings of Basel I and II guidelines, and the U.S. regulators have adopted many of the changes in capital related regulations. The Dodd-Frank Act also resulted in changes.

Of all the parts of Title 12 that cover capital, until recently most of the variation came from part 3 (OCC), part 217 (Federal Reserve) and part 325 (FDIC). To show the growing complexity of capital related regulations, I will plot the fraction of regulatory restrictions found in Title 12 for each regulator, relative to the total number of regulatory restrictions for each regulator. So for the OCC, I plot the sum of restrictions in parts 3 and 167 relative to all restrictions in parts 1–199. For the Federal Reserve, I plot the restrictions in part 217 relative to all restrictions found in parts 200–299. For the FDIC, I plot the sum of restrictions in parts 324 and 325 relative to all restrictions in parts 300–399.

The figure reveals that prior to the crisis, capital requirement regulatory restrictions made up no more than 10% of each regulator’s regulatory restrictions. After the crisis, that has more than doubled for OCC and FDIC capital requirement regulatory restrictions.

Below I plot a similar graph, but this time with regulatory restrictions replaced by word counts. The figure reveals similar patterns.

Overall, the findings in this post suggest that an increasingly important contributor to the rise in regulatory restrictions by bank regulator comes from capital requirement regulatory restrictions. In the next post, I’ll relate this to compliance, by showing how the rise in regulatory restrictions and word counts mirrors what’s happening with financial holding company call reports.