Concerned About Bank Climate Risk Exposures? More Equity’s An Option

[Note: The version as of June 2, 2021 revises the method used to motivate the discussion.]

In a recent blog-post, I discussed 1) why firms in certain industries (not just banks) may be deemed “Too Big to Fail” (TBTF), and 2) how higher equity capital requirements for TBTF firms could limit the implicit TBTF subsidies. In this blog post, I discuss why higher bank equity capital requirements can also address concerns about potentially greater future climate risk exposures in the banking sector. In short, for a given amount of risk observed in bank stock/equity returns, because a bank can increase risk through either leverage or the type of assets held, then since a bank with less equity has more leverage, it has to operate with much less riskier assets than a bank with more equity.

On Complex & Simple Ways to Regulate Bank Climate Risk Exposures

Some have proposed expanding the Basel Committee on Bank Supervision’s risk-based capital requirements to include climate risk-weights. That solution complicates an already complex regulatory framework. Judging from the history of the implementation of Basel-style capital adequacy standards, implementing the climate risk-weight standards could well result in yet another opportunity for law firms and consultants to offer their services to banks to guide them through the complex regulatory compliance process. It seems to me that bank customers would likely bear the brunt of the associated higher costs of complying with such new regulation.

Another approach consists of applying stress tests to climate risks. Here again, it seems to me that bank customers would likely bear the brunt of the associated higher costs of complying with such new regulation. Rather than compelling banks to use complex measures to capture climate risk exposures, an alternative that I explore here calls for significant increases in minimum bank equity capital requirements.

More equity for a bank means more loss absorbing capacity. With more equity, if climate exposures wind up being more severe than current predictions suggest, banks will be better prepared to navigate through the risks than if they continue funding with lots of debt. And if those exposures wind up being less severe, that’s fine too, since banks with more equity would still be better prepared to handle other non-climate risks, such as risk of default during banking crises.

After all, my co-author and I in a recent study, like some of the studies we cite, find that increasing the equity capital-to-asset ratio for all U.S. banks from 4 percent to 15 percent has benefits that outweigh the costs. In our baseline scenario, 19 percent was optimal. We also found many scenarios with optimal ratios in the 20–30 percent range, too, similar to what Anat Admati and Martin Hellwig suggested. An alternative approach might simply involve measuring equity capital requirements relative to liabilities rather than assets. [For instance, see pp. 115–116 of a report on the history of the Federal Deposit Insurance Corporation (FDIC), which points out that in the early days of the FDIC, minimum capital requirements were set to 10 percent of deposits.]

Bank Equity as a Call Option on Bank Assets

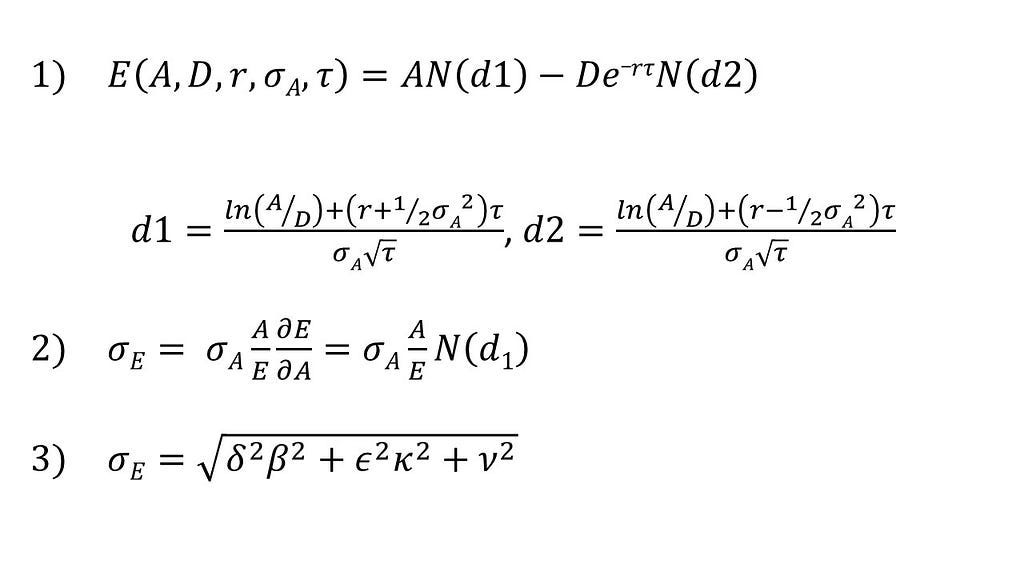

The motivation here comes from Robert Merton’s insight that you can view equity as a call option on a firm’s assets. That can even apply to a bank. In Merton’s solution, the call option is a function of the value of a bank’s assets, the face value of its debt, the risk-free rate of interest, the volatility of the firm’s assets as a measure of risk and lastly, the time to maturity of bank liabilities.

However, in the real world you can observe the market value of the bank’s stock (as well as the volatility of bank stock returns), but not the market value of the bank’s assets or the volatility of the return on bank assets. Therefore, I will use the option pricing model to solve for the unobserved market value of the bank’s assets, but the option pricing model has a second unknown, namely the unobserved volatility of the return on bank assets. To solve for the unobserved volatility of the return on bank assets, I use a second equation that reflects an equilibrium relationship between the observable bank stock return volatility and unobservable bank asset return volatility. I will also add a third equation that expresses the volatility of bank stock returns in terms of systematic market risk and climate risk inherent in the bank’s assets that comes from a two factor model of market model, which has the stock returns on the left-hand side, a systematic market risk factor and a climate risk factor as well as idiosyncratic risk on the right-hand side.

The three equations include:

The first equation just says that the current market value of a bank’s stock or equity (E), as a measure of net worth, reflects the difference between the market value of the bank’s assets (A) and the discounted present value of its debt (Dexp(-rτ)), where D is the face value of the debt and exp(-rτ) is the discount factor). But other factors come into play, too. N(d1) and N(d2) in the first equation complicate matters, but have some intuitive implications.

You might interpret N(d2) as the probability, in a risk-adjusted sense, that the option will be exercised; N(d1) is more abstract, relating to the present value of the contingent receipt of the assets exceeding the current value of the assets. In a mechanical sense, 1 ≥ N(d1) ≥ N(d2) ≥ 0. So N(d1) always equals or exceeds N(d2), because of the way the second and third equations are structured, as the second equation has a plus sign between terms in the numerator, while the third equation has a minus sign between terms in the numerator, meaning d2 does not exceed d1. N(d1) and N(d2) never exceed one or fall below zero. So if the option has value and is very likely to be exercised then N(d1), N(d2) will be close to one, so E ≈ A – Dexp(-rτ). And, if the option has no value and is very unlikely to be exercised N(d1) = N(d2) = 0, which means E = 0. You often observe intermediate values for N(d1) and N(d2), depending on the likelihood that the call option will be exercised.

The second equation just says that in equilibrium, the volatility of the bank’s equity is proportional to the volatility of the bank’s assets; the constant of proportionality equals the elasticity of the bank’s equity with respect to the bank’s assets, which measures the sensitivity of the bank’s equity to its asset values. On a more practical note, the second equation suggests that the bank’s equity return volatility will be higher if it is more leveraged, where I define leverage as assets relative to equity, and/or if bank staff choose to invest in riskier assets. That also means that for a given volatility of equity returns and leverage, equilibrium forces will tend to constrain the volatility of asset returns.

The third equation just breaks down the volatility of the bank’s equity in terms of its exposure to 1) systematic market risk (β), 2) the volatility of the market (δ), 3) systematic climate risk (𝜅), 4) the volatility of systematic climate risk (𝜖) and 5) the remaining unexplained volatility (𝜈).

Numerical Insights

I use equations 1), 2) and 3) to solve for the market value of the bank’s assets as well as the volatility of the bank’s assets after specifying the inputs. For simplicity, I assume the bank has a face value of debt equal to either $95 billion or $80 billion. I assume the market value of the bank’s equity equals either $5 billion or $20 billion and use equation 3) to specify the quantity of equity risk.

To motivate my choice of the other numerical inputs, I refer to an earlier draft of a working paper called Carbon Risk, which included carbon risk estimates for the financial sector. The more recent draft eliminates those estimates, given that the authors point out that the assignment of carbon emissions to equity and bank lending does not occur. But that does not mean that market valuations exclude those assessments. In addition to the market index, the paper constructs a “Brown Minus Green” portfolio, which measures the excess return of more brown firms relative to more green firms. While the working paper also includes other risk factors, I exclude them for the sake of simplicity.

For δ: the Carbon Risk paper reports in Table 2 that the monthly standard deviation for the market index equals 0.0402, which I first multiply by 12 and then round up to get an annualized standard deviation of 0.5.

For 𝜖: The Carbon Risk paper reports that the monthly standard deviation for the “Brown Minus Green” index, equals 0.0195, which I first multiply by 12 and then round up to get an annualized standard deviation of 0.25.

For β: my co-author and I found in our study mentioned earlier that most banks in the U.S. with traded shares have betas less than one, meaning they’re relatively safer than the market as a whole since banks can be viewed as shock absorbers. However, larger banks tend to have betas greater than one, meaning that they’re relatively riskier than the market as a whole. Here, I will assume that the bank is riskier than the market, and assume the market beta, β, equals 1.5. That means that for a one percent change in the market index, the bank’s stock will change by 1.5 percent.

For 𝜅: The Carbon Risk paper in Table 7 reports a range of “Brown Minus Green” carbon-related, climate risk factor from -0.587 to 0.25. However, I examine a wider range for 𝜅, from -2 to 2.

For 𝜈: As a measure of the bank’s unexplained, idiosyncratic risk, I assume that equals 0.5, like the market index.

For r: As a value for the risk-free rate, I assume that equals 0.02.

For τ: As a measure of the maturity of the bank’s debt, I assume that equals 0.25 based on estimates reported here, which suggests that the maturity of liabilities equals three months.

Results

Evaluating the three equations numerically, I present the estimated volatility of bank asset returns, assuming the market value of equity equals either $5 billion or $20 billion, the face value of debt equals either $95 billion or $80 billion, as well as the parameters, δ, 𝜖, β, 𝜅, σ, and τ discussed above. Plugging these values into the formula above yields the figure below:

The figure shows that for a given amount of equity return volatility:

1) the bank’s asset volatility increases as the systematic climate risk factor deviates from zero,

2) banks with a greater net worth have a higher asset volatility as a bank with $20 billion in equity can operate with asset risk equal to roughly 20 percent, while a bank with $5 billion in equity can only operate with asset risk equal to about 5 percent, and

3) banks with a greater net worth measured in terms of market value have a greater sensitivity of their asset return volatility to variation in systematic climate risk.

Another way to think about these results is that banks that operate with high leverage have less capacity to hold risky assets, whether the risk comes from systematic market risk, climate risk or something else.

Concluding Thoughts

Bank equity can offer a way to manage future climate risks, in terms of both concerns about funding risks, as well as concerns about underlying bank asset risk. Current approaches tend to call for fine-tuning capital requirements by establishing a floor for bank capital that all banks can satisfy. A more proactive approach to dealing with the potentially greater future risks, whether climate-related or otherwise, simply calls for increasing the minimum amount of equity capital by lots.

Concerned About Bank Climate Risk Exposures? More Equity’s An Option was originally published in FinRegRag on Medium, where people are continuing the conversation by highlighting and responding to this story.