So Which Is It: Too Much, Just Enough Or Not Enough Bank Capital?

If you’ve watched the recent House and Senate hearings in the aftermath of Silicon Valley Bank’s (SVB), Signature Bank’s and First Republic’s failures, members and witnesses have debated whether there’s not enough capital, just enough or too much. Meanwhile, the financial industry lobbying groups are already gearing up for any anticipated talk about making regulatory capital standards more stringent than they currently are. So who’s right?

Many of the differences in opinion likely arise because people mean different things by capital – those in policy circles tend to refer to regulatory capital, but I will explain how from a finance perspective capital can also just mean equity capital or even subordinated debt. Those in regulatory circles tend to refer to “risk-based” capital measures, which come from the Basel Committee on Banking Supervision (BCBS), a committee based at the Bank of International Settlements in Basel, Switzerland. The BCBS issues guidelines that define regulatory measures of capital (among other things), which national authorities choose to adopt or tailor before having banks adhere to these standards. The hearings focus on what are, in my view, uninformative “risk-based” measures of capital. Much like during the 2007-2009 Crisis, I’ll demonstrate how these measures make large distressed banks look well capitalized. So debates over whether capital’s high enough mislead.

Instead, simpler, higher minimum equity capital to asset (or liabilities) requirements work better than the complex, risk-based capital requirements. Also, subordinated debt can be capital, but when a bank issues it, it becomes more leveraged than if it issued an equivalent amount of equity instead. I will first summarize what people seem to mean, and what might offer a simpler, more effective way to do things.

The “Democrat View”: Not High Enough

While not universal, many Democrat Congressional members, along with political appointees and other senior officials in the current administration, hold the view that there’s still more work to be done to finish implementing Basel III guidelines, which the BCBS issued in June 2011, and US regulators largely adopted with some modifications. You can hear this view in the hearings as Democrat members ask Supervisory staff whether current standards are sufficient, to which the reply generally seems to be “no.”

The “Republican View”: Just Right, If Not Too High

Many Republican Congressional members seem to think that regulatory capital standards in the U.S. are already complex enough, and the best way forward would be to leave things as they are. After all, S. 2155 took considerable effort to get passed, and even changes made to pass it watered down earlier versions of the legislation that came through the House. Here too, the view presumes risk-based capital requirements work just fine, but that the level required is just right, if not too much. Those thinking it may be too high may do so on the grounds that they believe higher capital requirements will reduce lending.

My view blends the “Democrat View” that capital’s not high enough, with the “Republican View” that capital regulation right now proves too onerous, but I use a different measure of capital. With this discussion in mind, the trouble with risk-based capital is that, while perhaps well-intended, it gives banks more means to give the appearance of being well capitalized, without eliminating the risk of being distressed.

What’s Wrong With Regulatory Capital: Too Much Gaming

In a number of studies since the 2007-2009 Crisis, I along with co-authors have shown that risk-based capital that come from the BCBS guidelines provide misleading signals about safety and soundness. In one study, Jim Barth and I, like former Securities and Exchange Commission Chief Economist, Mark Flannery before us, showed that banks can satisfy regulatory capital requirements, even when those banks experiences distress. How is that possible?

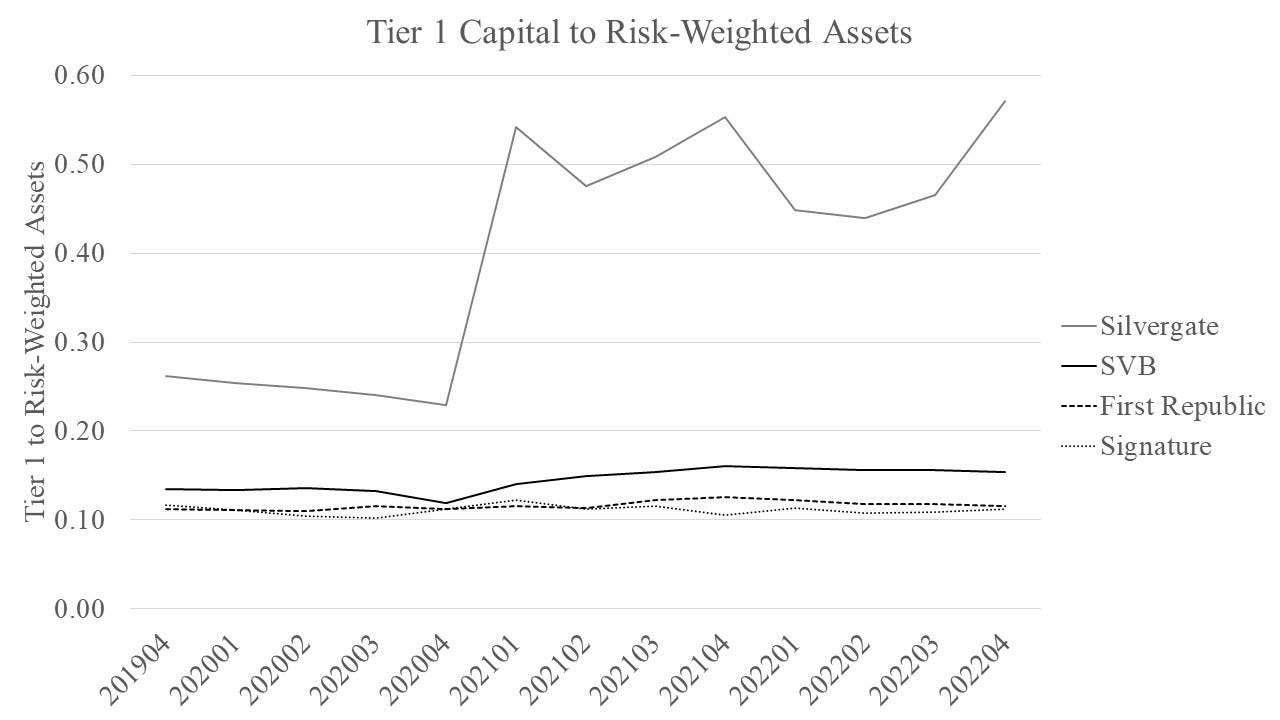

The figure below depicts a key measure, the Tier 1 capital relative to risk-weighted asset, or Tier 1 ratio, for each bank that’s recently closed or failed from Q4 2019-Q4 2022. Under US Basel III, the ratio should be at least 8 percent for a bank to be classified as “well capitalized.” The three failed banks, SVB, Signature and First Republic all exceed that minimum. Notice that Silvergate, which voluntarily liquidated, starting in Q1 2021 had a Tier 1 ratio of well over 40 percent, and in the last quarter before the bank voluntarily liquidated, it’s ratio equaled 57.1 percent! How?

In the case of Silvergate, out of roughly $11 billion in total assets, about $4 billion were held as reserves about $5 billion in available-for-sale securities, mostly MBS and Treasuries. Because these assets required at most, very little capital, Silvergate’s required capital to back most of its assets was very low.

To delve deeper into this issue, the Tier 1 capital ratio’s defined as follows:

Tier 1 capital is an accounting measure of capital that relates to equity capital, but as Jim Barth and I discussed, in the paper linked above, it’s definition changed under Basel III, as earlier definitions allowed banks to include things that had could not count on during periods of distress. Moreover, the denominator gives rise to gaming, as I’ve previously discussed. Given that some assets, like reserves and US Treasuries have no capital requirements, they do not get included in the denominator. Other assets such as agency Mortgage-Backed Securities (MBS) have low capital requirements. As we have seen, the (perhaps unexpected) losses that banks experienced in their bond portfolios due to inflation, could have been offset if these assets had higher capital requirements. Even municipal bonds and mortgages have lower capital requirements than standard commercial loans or other assets that regulators deem risky.

That means regulators determine that banks need less capital to back these assets than standard commercial loans. Knowing this, a bank can choose assets with low or even zero required capital to reduce the denominator, and by reducing the denominator you increase the capital ratio and appear “well-capitalized”.

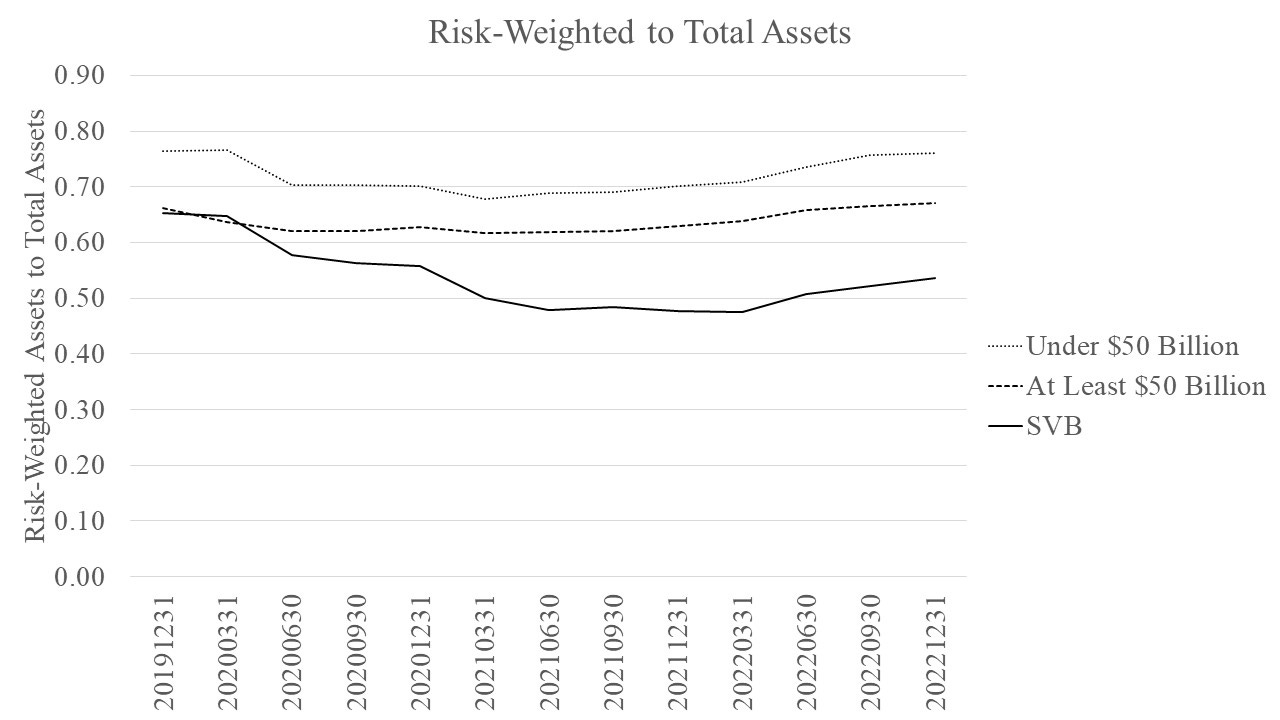

The largest banks tend to satisfy their risk-based capital requirements by holding more low risk-weighted assets. because risk-weighting tends to reduce the amount of assets that banks have to back with capital, you can get a sense of how much gaming of the capital ratio occurs by computing the ratio of risk-weighted to total assets. The larger the ratio, the more capital you have to have to satisfy regulatory requirements. Compared to other bank holding companies with at least $50 billion in total assets, the graph below shows that SVB had an even lower ratio of risk-weighted to total assets. For a given amount of capital, SVB with lower risk-weighted assets can appear more capitalized.

What’s Wrong With Regulatory Capital: Too Complex, Too Costly to Implement

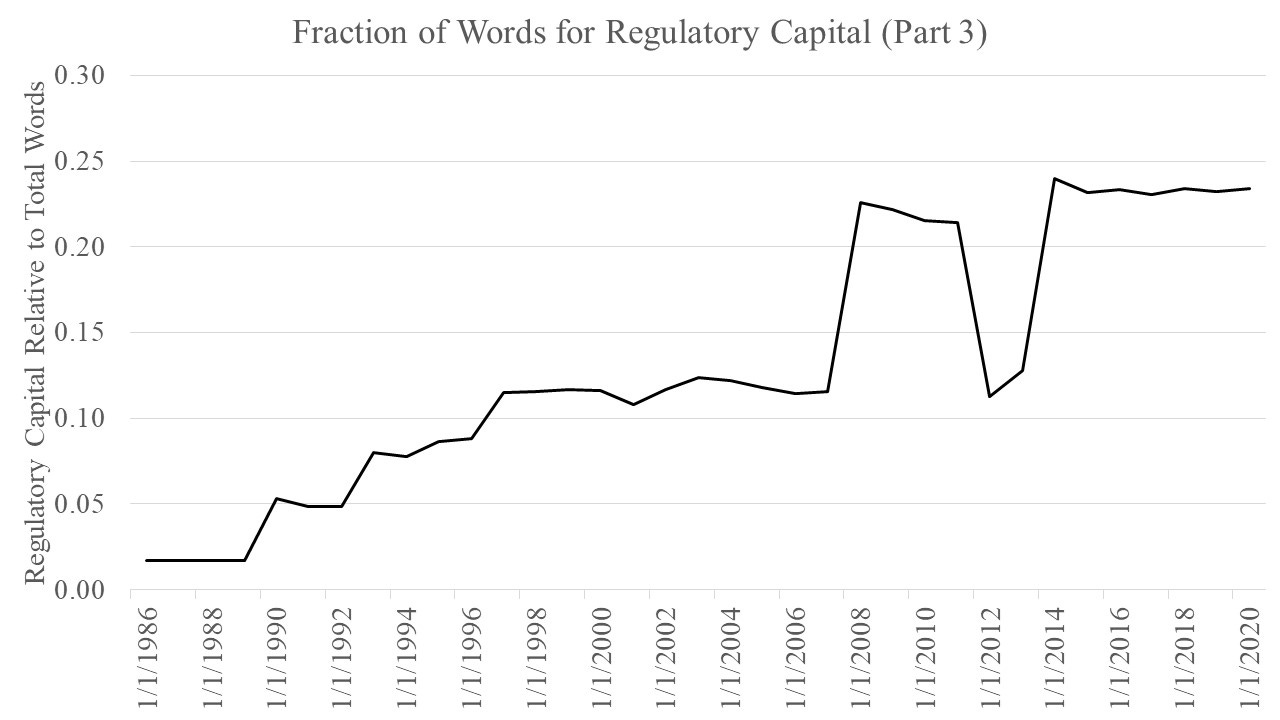

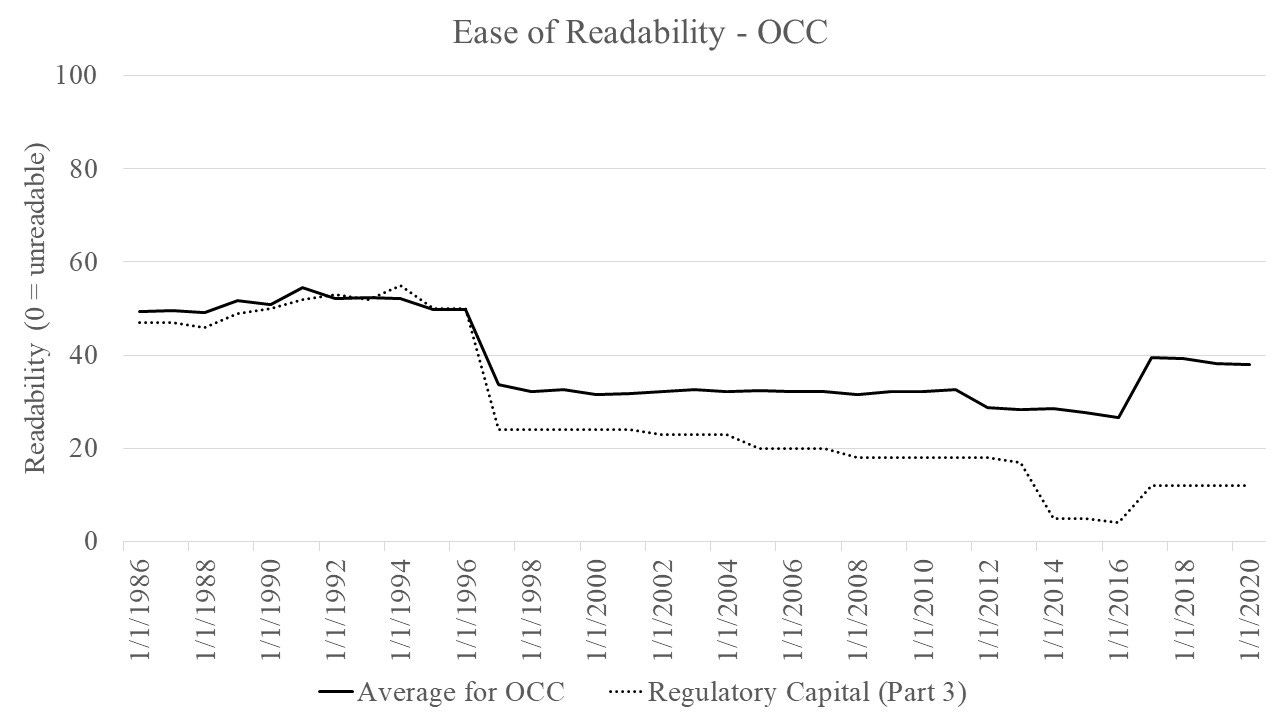

Moreover, the introduction of risk-based capital requirements has made regulatory capital increasingly complex since the 1980s. Regulatory capital requirements already makes up about 20 percent of the entire regulatory word count for banks (for the uninitiated, trying reading through the subparts of Code of Federal Regulations Title 12 Part 3, which is the Office of the Comptroller of the Currency’s guidelines for large banks). That’s even though regulatory capital makes up a small fraction of one side (the liability side) of a bank’s balance sheet, often under ten percent.

Not only does regulatory capital take many words to describe, but it’s harder to read through those words, as you can see with the Flesch Reading Ease score, with 0 meaning unreadable and 100 meaning very readable. A lack of readability translates into more billable hours for lawyers and other experts, higher firm costs, which banks can easily pass onto customers. So while you may think you’re sticking it to the banks when you write more complex regulations, complying with those regulations becomes more costly for everyone, as that increases the cost of banking. A simpler alternative that reintroduces market discipline exists.

A Simpler, Higher Capital Alternative With Market Discipline

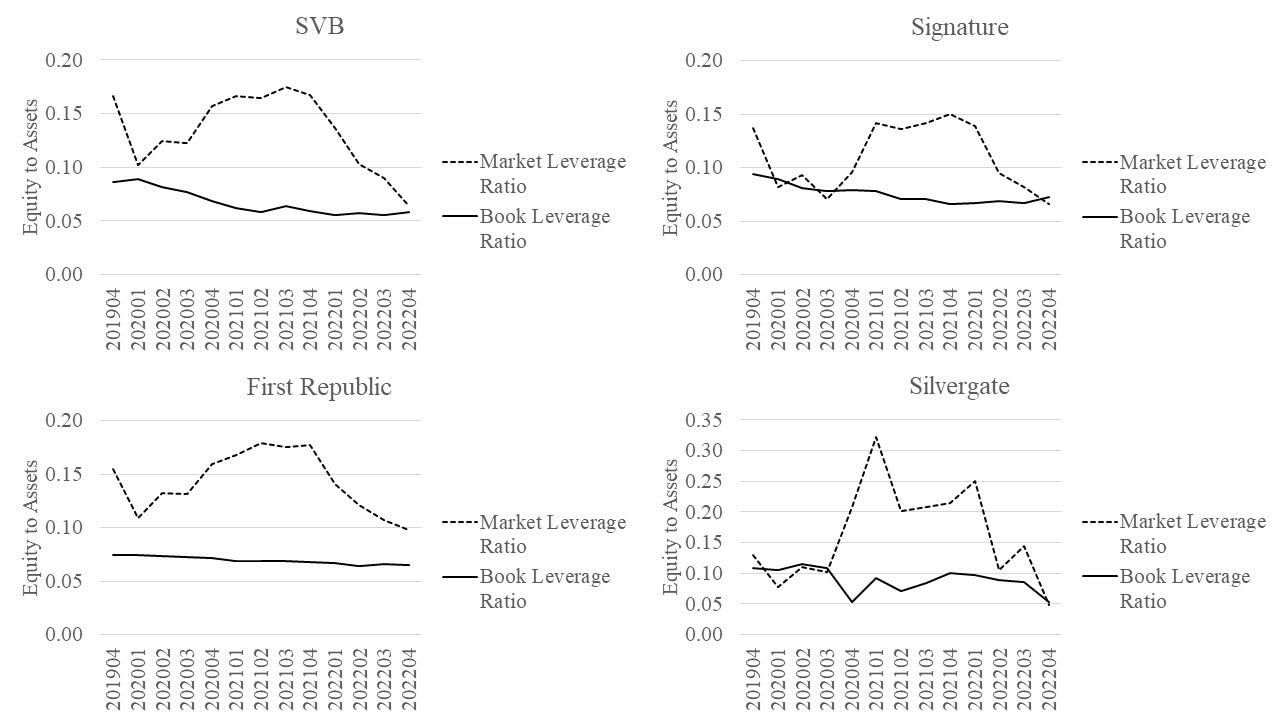

Regulatory capital predominantly reflects accounting or “book” values, yet investors also pay attention to the market value of equity. One Nobel prize winner for work in finance, Merton Miller, once uttered the quip “… stock … selling for only 50 percent of book value … [is] … just the market's way of saying: We gave those guys a dollar and they managed to turn it into 50 cents.” In finance, since at least Nobel laureate Robert Merton’s “rocket science” approach to corporate finance, the market value of equity is known to reflect asset risk in addition to leverage. Applied to a bank, the riskier a bank’s assets the greater the market value of a bank’s equity, but when the bank relies more on leverage, the market value of a bank’s equity decreases. Ideally, accounting value of equity should roughly equal its market value. Using the accounting and market values together, you can monitor changes in a bank’s equity. When it lies above that’s a good sign in the sense that market values the bank more than the accountants, but it could also reflect growth and/or risk-taking by the firm. If market value lies below the accounting values, that signals that the market values the bank less than the accountants.

The figure below depicts the book leverage ratio (measured as book equity relative to book assets), as well as the market leverage ratio (measured as market equity relative to the quantity of book assets minus book equity plus market equity) for the banks that failed or closed in Spring 2023. Applied to the recent failed banks, as well as Silvergate, you can see that each bank’s market leverage ratio exhibited considerable growth in 2021. Also, the market leverage ratio for each bank’s equity declined throughout 2022, before their operations came to a halt. Lastly, even the book leverage ratios declined for the three failed banks during the sample. Unlike the Tier 1 capital to Risk-Weighted Asset ratios shown above for the three failed banks, which remained flat, the downward trending book leverage ratios and especially market leverage ratio indicate that the banks’ performance deteriorated for some time before they had to shut down operations.

How High Could a Simpler, Higher Leverage Ratio Be?

Lastly, to address how high the leverage ratio could be, the figure below shows the result of a baseline exercise from a longer study I co-authored with Jim Barth on the benefits and costs of a higher bank leverage ratio, summarized here. We examine if the benefits of increasing the leverage ratio (assuming risk-based capital requirements are eliminated) to 15 percent exceeds the costs. From our estimates, we find that in general the benefits do exceed the costs. The exercise quantifies the tradeoff between increasing capital requirements, which reduces the probability of a banking crisis, and therefore reduces the associated loss of Gross Domestic Product (GDP), but also may increase the cost of lending, which in turn lowers GDP. Under fairly conservative assumptions about the benefits of increasing capital requirements and under the highest cost case, we found that the optimal leverage ratio equals 19 percent.

Some Concluding Thoughts

Whether you think regulatory capital requirements are not high enough, just right or too high, you’re probably not thinking about the unintended distortions these regulations have on bank balance sheets, or about how costly it is to comply with this regulation. For good reason, as you only seem to see the unintended distortions after things go wrong, and we don’t have good data on costs (but you can start by looking at the salaries people earn). Sure, the regulatory code creates jobs, but perhaps those working on compliance could use their talents more productively, elsewhere. After all, as in 2007-2009, those working on complying with capital regulation were successful, even as their banks went under. A simpler, higher capital regime that reconnects bank capital back to its origins, a source of non-run prone funding, will be much cheaper to comply with. It will also reconnect capital to strong market discipline, whereby regulators (along with everyone else watching), can see that when a bank’s stock price drops, it might be time to act.