Top 5 Financial Regulatory Restriction-Generating CFR Parts in 2016, By Agency

In this post, I will list of the parts of the Code of Federal Regulation (CFR) that generated the highest fraction of financial regulatory…

In this post, I will list of the parts of the Code of Federal Regulation (CFR) that generated the highest fraction of financial regulatory restrictions by agency in 2016, and will also report the corresponding fraction for 1970. Recall, by regulatory restrictions, I mean words such as “shall”, “must”, “may not”, “required” and “prohibited”; I use the RegData 3.0 data from the QuantGov website described by my colleagues, McLaughlin, Patrick A., and Oliver Sherouse. 2017. “QuantGov — A Policy Analytics Platform.” The federal agencies I examine include the Office of the Comptroller of the Currency (OCC), the Federal Reserve, the Federal Deposit Insurance Corporation (FDIC), the National Credit Union Administration (NCUA), the Bureau of Consumer Financial Protection (CFPB), the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC).

In the CFR Title 12, parts 1–199 cover the OCC, parts 300–399 cover the FDIC, parts 700–799 cover the NCUA, parts 200–299 cover the Federal Reserve, parts 1000–1099 cover the CFPB. In Title 17, parts 1–199 cover the CFTC, while parts 200–399 cover the SEC. I’ll present the agency level summaries in that order.

Complementing the findings I had in a recent post about the rising fraction of regulatory restrictions coming from capital requirements, here I show that the largest fraction of regulatory restrictions for the OCC and FDIC relate to bank capital regulation. For the NCUA, regulations concerning the organization and operation of credit unions generate the largest fraction of regulatory restrictions. For the Federal Reserve and CFPB, Truth in Lending (Reg. Z) regulations generate the largest fraction of regulatory restrictions. For the CFTC, general regulations that concern the Commodity Exchange Act generated the largest fraction of regulatory restrictions, although there’s now a rise (since 2002) from those related to derivatives clearing organizations. For the SEC, “General Rules & Regulations” concerning the Securities Exchange Act of 1934 (Part 240) and 1933 (part 230) generate the largest fraction of regulatory restrictions, respectively. Let’s get to the details.

Bank Regulators

Table 1 lists the top 8 regulatory restriction generating parts of the CFR that concern the OCC. I include the additional three because like “Part 3 — Capital Adequacy Standards”, the eighth ranked “Part 167 — Capital” also concerns bank capital.

Table 1. OCC Top 5 Regulatory Restrictions, 1970 & 2016

Part 3 generated the most regulatory restrictions, about 21.7 percent, in 2016. An additional 2.5 percent fraction of regulatory restrictions come from “Part 167 — Capital.” The combined fraction equals just over 24 percent as I reported in the earlier post. While “Part 19 — Rules of Practice and Procedure” used to generate about 20 percent of the OCC’s regulatory restrictions in 1970, the fraction has fallen to about 5.4 percent in 2016. Finally, the top 5 categories generate about 51 percent of all regulatory restrictions in 2016. Two of the top five categories did not exist in 1970.

Table 2 lists the top 6 regulatory restriction generating parts of the CFR for the FDIC. Note the biggest contributor for the FDIC in 2016 was “Part 390 — Regulations Transferred from OTS,” related to the transfer of regulations that came with section 313 of Dodd-Frank, which abolished the Office of Thrift Supervision (OTS). The median value for Part 390 is calculated since 2012. After that, the next two largest categories concern bank capital. “Part 324 — Capital Adequacy of FDIC-Supervised Institutions” at about 14 percent and “Part 325 — Capital Maintenance” at about 10 percent. Combining the two categories means that capital related regulatory restrictions generate the largest fraction of total regulatory restrictions. Finally, the top 5 categories generate about 59 percent of all regulatory restrictions. Three of the top 5 did not exist in 1970.

Table 2. FDIC Top 5 Regulatory Restrictions, 1970 & 2016

The NCUA

Table 3 lists the top 8 regulatory restriction generating parts of the CFR for the NCUA, between 1971 and 2016, since no values exist for 1970.

Table 3. NCUA Top 5 Regulatory Restrictions, 1971 & 2016

The biggest contributor for the NCUA in 2016 was “Part 701 — Organization and Operation of Federal Credit Union,” followed by “Part 747 — Administrative Actions, Adjudicative Hearings, Rules of Practice & Procedure & Investigations.” The third largest is Part “707 — Truth in Savings.” Interestingly, while capital regulations for the OCC and FDIC make up almost 25 percent of 2016 bank-related regulations, for the NCUA, they make up only 4 percent. Finally, the top 5 categories generate about 56 percent of all regulatory restrictions, down from 59 percent in 1971. Two of the top 5 generating parts did not exist in 1971.

Bank Holding Company and Consumer Finance Regulators

Table 4 lists the top 5 contributors to Federal Reserve regulatory restrictions. For the Federal Reserve, the largest contributor by far is “Part 226 — Truth in Lending (Reg. Z)”. The next largest category is “Part 217 — Capital Adequacy of Holding Companies & State Member Banks,” which generates about 8.1 percent. The top 5 categories generate about 56 percent of all regulatory restrictions in 2016. Three of the top five parts did not exist 1970.

Table 4. Federal Reserve Top 5 Regulatory Restrictions, 1970 & 2016

Note that concerning Part 226, Section 1100A of Dodd-Frank transferred rule-making authority for Reg. Z from the Federal Reserve to the CFPB. For the sake of comparison, I also list the top 5 contributors to CFPB regulatory restrictions in 2016 in Table 5 below. The top five parts generate 78 percent of all regulatory restrictions.

Table 5. CFPB Top 5 Regulatory Restrictions, 1970 & 2016

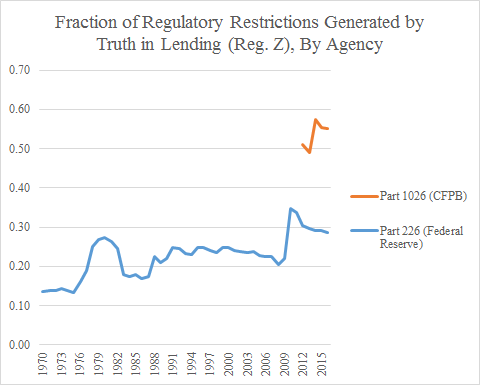

To show that Reg. Z related regulatory restrictions for the Federal Reserve had been trending upward over time prior to the crisis, the figure below depicts the fraction of regulatory restrictions for the Federal Reserve that come from section 226 from 1970 to 2016, as well as for section 1026 for the CFPB from 2012 to 2016.

For the Federal Reserve, the fraction has ranged from a low of about 13 percent in 1975 to a high of about 35 percent in 2010, after which the CFPB took on responsibility for Reg. Z. This point deserves attention, because a key motivation for creating the independent CFPB was because the Federal Reserve is alleged to have ignored complaints about abuses in run-up to the last crisis, even though over 20 percent of the rule-making associated regulatory restrictions came from this part.

A perhaps more holistic summary of events leading up to the crisis was reported in the Financial Crisis Inquiry Commission Report on p. 21, associated with former Federal Reserve Board member Susan Bies’s testimony, which suggests that little was done because:

deliberations over the potential guidance also stirred debate within the Fed, because some critics feared it both would stifle the financial innovation that was bringing record profits to Wall Street and the banks and would make homes less affordable. Moreover, all the agencies — the Fed, the OCC, the OTS, the FDIC, and the National Credit Union Administration — would need to work together on it, or it would unfairly block one group of lenders from issuing types of loans that were available from other lenders. The American Bankers Association and Mortgage Bankers Association opposed it as regulatory overreach.

“The bankers pushed back,” Bies told the Commission. “The members of Congress pushed back. Some of our internal people at the Fed pushed back.”

So while the Federal Reserve has drawn all of the attention, given its role in Reg. Z, perhaps a more balanced view concerns the fact that there were many competing interests (e.g., bankers, members of Congress and some at the Federal Reserve) favoring the securitization business model. The passage suggests that Federal Reserve staff not only thought of the performance of the entities it regulated, but also had home affordability in mind.

Securities Market Regulators

Moving on to the securities regulators, Table 6 lists the top 8 parts of the CFR that contribute to CFTC regulatory restrictions. The top 5 generate about 37 percent of all regulatory restrictions. Four of the top 5 parts did not exist in 1970. The most notable change has been the decline of the role of General Regulations, which stood at 66 percent in 1970 and by 2016 that now stands at 16 percent. Regulatory restrictions concerning derivatives clearing organizations (Part 39) has risen from about 1 percent in 2002 to 5 percent in 2016.

Table 6. CFTC Top 5 Regulatory Restrictions, 1970 & 2016

Table 7 lists the top 6 parts of the CFR that contribute to SEC regulatory restrictions. The top 5 account for 74 percent of all regulatory restrictions in 2016, up 67 percent in 1970. Unlike the other regulators discussed here, only one of top 5 parts did not exist in 1970.

Table 7. SEC Top 5 Regulatory Restrictions, 1970 & 2016

Conclusion

Overall, for most of the agencies discussed here, the top 5 regulatory restriction generating parts of the CFR in 2016 generated at least half of each agency’s regulatory restrictions (the exception was the CFTC). This suggests that in a given year, much of the regulatory burden comes from a narrow part of the CFR that concerns a particular agency. In addition, for most agencies (the exception was the SEC), many of the top 5 regulatory restriction generating parts did not exist in 1970, which unsurprisingly suggests that regulations are adapting to changes taking place in the financial system.

NOTE: This post was updated on March 13, 2018 to incorporate results for the NCUA.