Which Trading Assets Drove Too-Big-to-Fail Subsidies During the 2007–2009 Crisis?

[Note: The version as of May 6, 2021 corrects an error in the calculation of the subsidy, elaborates on the discussion of the method used to calculate the subsidy, updates the empirical results and corrects a few minor typos in the text.]

After the 2007–2009 crisis, global initiatives led in part by former Federal Reserve Chair Paul Volcker highlighted proprietary trading, essentially trades of primary and derivative securities for the purpose of enhancing bank revenues rather than trades executed on behalf of clients, as a cause of the crisis. That in turn led to subsequent calls to introduce the so-called “Volcker Rule.” The rule eventually became a reality, in spite of the fact that Volcker himself later acknowledged that proprietary trading did not cause the crisis.

In this post, using a broad sample of bank holding companies (BHCs) in Q2 2008-Q1 2009, I show how quarterly changes in estimates of the so-called Too-Big-to-Fail (TBTF) subsidy for each BHC relate to various proprietary trading asset holdings, each measured as a share of total assets. I find that CDO holdings on average had a large positive association with changes in the estimated TBTF subsidy, while other trading asset holdings had small or even no association with changes in the subsidy.

To estimate quarterly changes in the TBTF subsidy, I begin by applying an option pricing framework developed by Robert Merton to estimate the unobserved market value of assets and their volatility in each quarter, for each BHC. I then use the estimated market value and volatility of assets as inputs, among others, to estimate the subsidy as implicit guarantees on BHC debt. I then examine how quarterly changes in the estimated TBTF subsidy relate to various trading asset categories. I describe how I estimate the subsidy and then turn to the empirical analysis, next.

Estimating the TBTF Subsidy as a Put Option on a BHC’s Assets

From an outsider’s perspective, BHCs have unobservable market values of assets, which poses a challenge if you want to estimate the market value of each BHC’s assets as well as the volatility of those assets. However, under certain assumptions, you can use an option pricing model to estimate the market value of those assets as well as their volatility.

In the first step, a commonly used approach applies Robert Merton’s formula to estimate the market value of each BHC’s equity as a call option on the BHC’s assets, measured at unobservable market values, together with another equation relating the BHC’s unobservable asset volatility to the observable equity volatility. Using these two non-linear equations in two unknowns, you can then back out estimates of the unobservable market value of assets and the unobservable volatility of assets.

Aside from the estimated market value of a BHC’s assets and their volatility, the model requires other inputs to calculate the implicit TBTF subsidy. The first is total BHC liabilities, which I measure as the difference between its book value of assets (BHCK2170) and book value of equity (BHCK3210), where the mnemonic terms in parentheses here and below list the BHC call report series names (see https://www.federalreserve.gov/apps/mdrm/data-dictionary/). I also use end-of-quarter 3-month Treasury rates as a measure of the risk-free rate. Lastly, for time to maturity, I use a value of 0.4, equivalent to just under 5 months, which is slightly higher than the 0.34 value reported in a recent study of the maturity of US bank debt.

Substituting these inputs into Robert Merton’s put option pricing formula gives estimates of the implicit value of TBTF subsidies extended to BHCs during the sample. The reason for using put option values comes from the observation that debt guarantees work like put options, as I recently discussed.

Summary of Results

Consistent with Volcker’s subsequent admission, I find that proprietary trading assets whether measured according to the 2013 or 2019 revision of the Volcker Rule on average had an empirically small relationship when compared with total assets held by BHCs. The estimates imply a change of about $32 million if you use the 2019 rule and about $20 million if you use the 2013 rule for each percentage point increase in the respective share of total assets. On the other hand, changes in the TBTF subsidy had a much larger association with a specific subset of proprietary trading assets, namely collateralized debt obligations (CDOs), basically structured products that pool assets (including bonds or other structured products) as collateral. CDOs issue claims that entitle investors to cash flows from the underlying assets. The estimates imply an increase of almost $7.7 billion (yes, billion not million!) for each percentage point increase in the CDO share of total assets.

Of course, BHCs had much smaller CDO asset shares than proprietary trading asset shares, but the point I make here simply emphasizes how CDO holdings were more damaging. This finding should come as no surprise as these products were at the center of the crisis (for instance, see MIT Finance Professor Andrew Lo’s 2012 survey article, or Federal Reserve Bank of Philadelphia Senior Vice President Larry Cordell’s 2011 co-authored study or the 2019 update).

2013 and 2019 Volcker Rule Proprietary Trading Assets

To understand where the two measures of proprietary trading assets come from, Congress called on regulators to target proprietary trading through the so-called “Volcker Rule” in Section 619 of the Dodd-Frank Wall Street Reform and Consumer Protection Act, or Dodd-Frank Act for short. That gave rise to the 2013 version of the Volcker Rule. However, following the 2016 election, Congress revised parts of Dodd-Frank, including the Volcker Rule, through the Economic Growth, Regulatory Relief, and Consumer Protection Act (EGRRCPA).

EGRRCPA in turn gave rise to one of the 2019 revisions of the Volcker Rule. When the Federal Deposit Insurance Corporation (FDIC) finalized its revision, former Chair and current FDIC Board member, Martin Gruenberg dissented.

The dissent reports estimates that the revised rule would exclude $619 billion out of $2.45 trillion worth of 2018 BHC assets and liabilities that would have been subject to the 2013 rule. The $619 billion in assets now excluded from proprietary trading rules includes so-called “available for sale” assets, and equity and non-traded derivative assets reported at fair value.

Measuring 2013 and 2019 Volcker Rule Proprietary Trading Assets in 2008/2009

The 2019 measure captures most of the assets, which are reported in BHC call report “Schedule HC-D Trading Assets and Liabilities.” The call report forms have changed somewhat since 2008/2009, as the forms have increased greatly in length, and some variables have been dropped since then, while others have been added.

To measure 2019 Volcker Rule proprietary trading assets using 2008/2009 data, I use:

· non-agency, commercial and residential mortgage backed securities, which in 2008/2009 was “All other mortgage-backed securities” (BHCM3536)

· other debt securities including structured products, which in 2008 was “other debt securities” (BHCM3537)

· “other trading assets” (BHCM3541)

· “derivatives with a positive fair value” (BHCM3543), and

· “total trading liabilities” (BHCT3548)

To measure 2013 Volcker Rule proprietary trading assets, I start with the 2019 measure and add certain available-for-sale assets, which in 2008/2009 included:

· “other pass-through securities” (BHCK1713)

· “all other mortgage-backed securities” (BHCK1736)

· “asset backed securities (BHCKC027)

· “other domestic debt securities” (BHCK1741)

· “foreign debt securities” (BHCK1746)

· “investments in mutual funds and other equity securities with readily determinable fair values” (BHCKA511)

I also include “gross positive fair value”: “interest rate contracts” (BHCK8741), “foreign exchange contracts” (BHCK8742), “equity derivative contracts” (BHCK8743) and “commodity and other contracts” (BHCK8744). Lastly, the 2013 rule measured in 2008/2009 would also include “gross negative fair value”: “interest rate contracts” (BHCK8745), “foreign exchange contracts” (BHCK8746), “equity derivative contracts” (BHCK8747) and “commodity and other contracts” (BHCK8748). One category that does not appear in the 2008/2009 call report forms is “equity securities with readily determinable fair values not held for trading.”

Trading Assets and Bank Risk

In the sample, from Q1 2008-Q4 2008, 2013 Volcker Rule trading assets on average equaled 2.4 percent of total BHC assets, while 2019 Volcker Rule trading assets on average equaled 0.4 percent of total BHC assets. However, for large CDO dealers, 2013 Volcker Rule trading assets on average equaled 22.2 percent of total BHC assets, while 2019 Volcker Rule trading assets on average equaled 17.2 percent of total BHC assets.

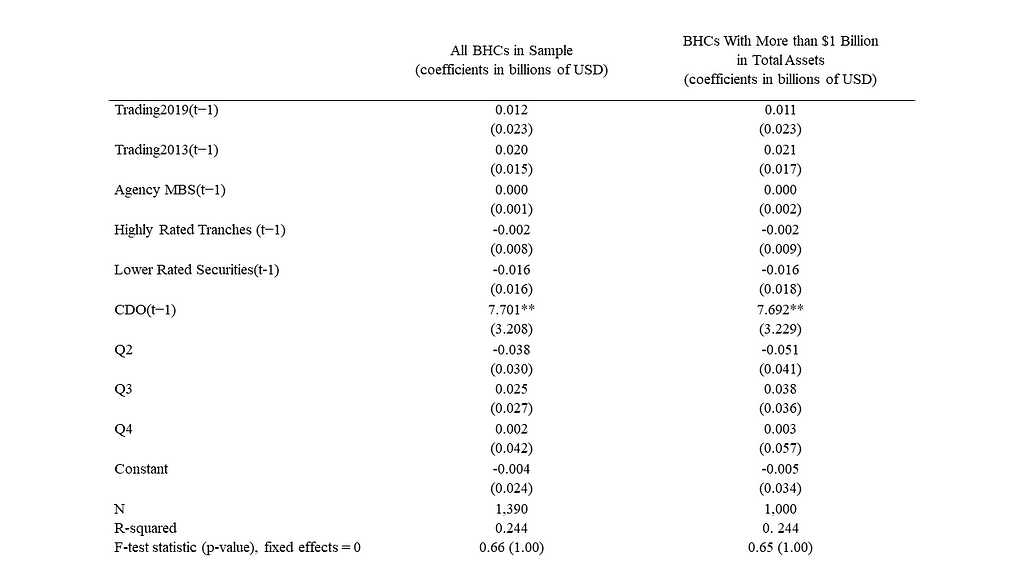

Table 1 below reports the estimated coefficients measuring the ceteris paribus average sensitivity of quarterly changes in BHC TBTF subsidy to increases in the share of a particular trading asset category between Q2 2008-Q1 2009. I use a relatively short sample of one year of quarterly data because CDO data was only reported in Q1 2008-Q1 2009 before the call reports were revised, and I use one-quarter lagged values in the regressions. I estimate pooled ordinary least squares regressions rather than fixed effects regressions as I cannot reject the null hypothesis that all fixed effects equal zero. I report standard errors clustered at the BHC level. The primary trading asset categories include estimates of the 2013 Volcker Rule and 2019 Volcker Rule proprietary trading asset categories. I also include a measure of a BHC’s share of highly rated, private label securitization tranches — primarily holdings of bonds sold from bank-originated, mortgage backed securities (MBS) — first proposed in a Review of Financial Studies publication. I also include a measure of lower rated securities that I used in a recent study of the Recourse Rule. Lastly, I include the share of agency MBS that get pooled by Freddie Mac and Fannie Mae, as some commentators have suggested that agency MBS caused the crisis.

Table 1. Panel Estimates of Quarterly Changes in the TBTF Subsidy Against Trading Assets, Q2 2008–Q1 2009

Since the 2019 proprietary trading asset measure is a subset of the 2013 proprietary trading asset measure, by including both categories in the regression, the 2013 proprietary trading asset coefficient measures the contribution to changes in the TBTF subsidy, while the 2019 proprietary trading asset coefficient measures the difference between the effects of the two measures. Thus, if the estimated 2013 coefficient equals a, and the estimated 2019 coefficient equals b, the contribution of 2013 proprietary trading assets equals a, while the contribution of 2019 proprietary trading assets equals a + b.

The results in Table 1 for the broader sample of BHCs suggest that if you increase the share of assets held as CDOs by one percentage point, on average the TBTF subsidy increases by $7.7 billion. If you increase 2013 trading asset share by one percentage point, on average the TBTF subsidy increases by $20 million. If you increase the 2019 trading asset share by one percentage point, on average the TBTF subsidy increases by $32 million ($20 million + $12 million). The MBS share has no association with the TBTF subsidy, while the higher and lower rated private label securities have a small negative association with changes in the TBTF subsidy; this result could be consistent with the effects of various Treasury and Fed programs that guaranteed various securities in 2008–2009. I get similar results if I just look at BHCs with over $1 billion in total assets.

Conclusion

The debate over the Volcker Rule has been fraught with ambiguity over what caused the last financial crisis and what to do about it. The results here indicate that in general, proprietary trading assets, whether measured according to the 2013 Volcker Rule or the 2019 revision of the Rule, were not on average associated with changes in TBTF subsidy during the crisis. CDOs had a much higher association with changes in the TBTF subsidy during the crisis, while other securities such as MBS did not. These findings offer some confirmatory evidence, which suggest that a broad regulatory focus on proprietary trading may not have the intended effects in terms of preventing crises, as some post-crisis narratives suggest.

Which Trading Assets Drove Too-Big-to-Fail Subsidies During the 2007–2009 Crisis? was originally published in FinRegRag on Medium, where people are continuing the conversation by highlighting and responding to this story.