Yes, Risk-Based Capital Contributed to the Crisis, Can Be Gamed…

In my previous post, I discussed my support for a 2017 critique of the supplementary leverage ratio written by Sean Campbell at the Financial Services Forum. As much as I agreed with the views there, soon after posting, I came across Sean Campbell’s critique of former FDIC Chair, Sheila Bair’s recent op ed. Here, I will critique the first four claims about risk-based capital, which I think are debatable, at best: 1) “Risk-based capital requirements did not cause the financial crisis,” 2) ‘Risk-based capital requirements are not “gamed” by banks,’ 3) ‘The leverage ratio is not “neutral” to capital allocation’, and 4) “A binding leverage ratio is not evidence that risk-based capital requirements are too low.”

1. On Risk-Based Capital and the 2007-2009 Financial Crisis

In 2013, I taught an undergraduate elective on the 2007-2009 Financial Crisis and used the Financial Crisis Inquiry Commission Report (FCICR) as the primary text. The FCICR identified the role of the Recourse Rule, which adopted an early version of Basel II risk-weights for securitization tranches as a reason for the rise (see numbered pages 99-100, 119, 140 and 196). To understand how, the rule lowered capital requirements on the highest-rated, private label securitization tranches, including collateralized debt obligations, and increased capital requirements on lower-rated, private label tranches. You might then expect that if you lower/increase the capital requirements on a particular asset class, at least some banks might respond by increasing/decreasing their holdings of those assets.

Unfortunately, the FCICR itself did not provide evidence to support the assertions. When I joined the Mercatus Center in 2014, I set as my first task to investigate this issue empirically; after all, Arnold Kling had also flagged the reduction in capital requirements for highly-rated, private label securitization tranches as a cause of the crisis, but also offered no evidence. The earliest preliminary evidence I found supporting the hypothesis was in Chapter 2 of Jeffrey Friedman and Wladimir Kraus’s Engineering the Crisis and a paper published in the prestigious Review of Financial Studies by Isil Erel, Taylor Nadauld and Rene Stulz. You can think of my work as building on the latter paper to test the hypothesis about how risk-based capital regulation contributed to the crisis.

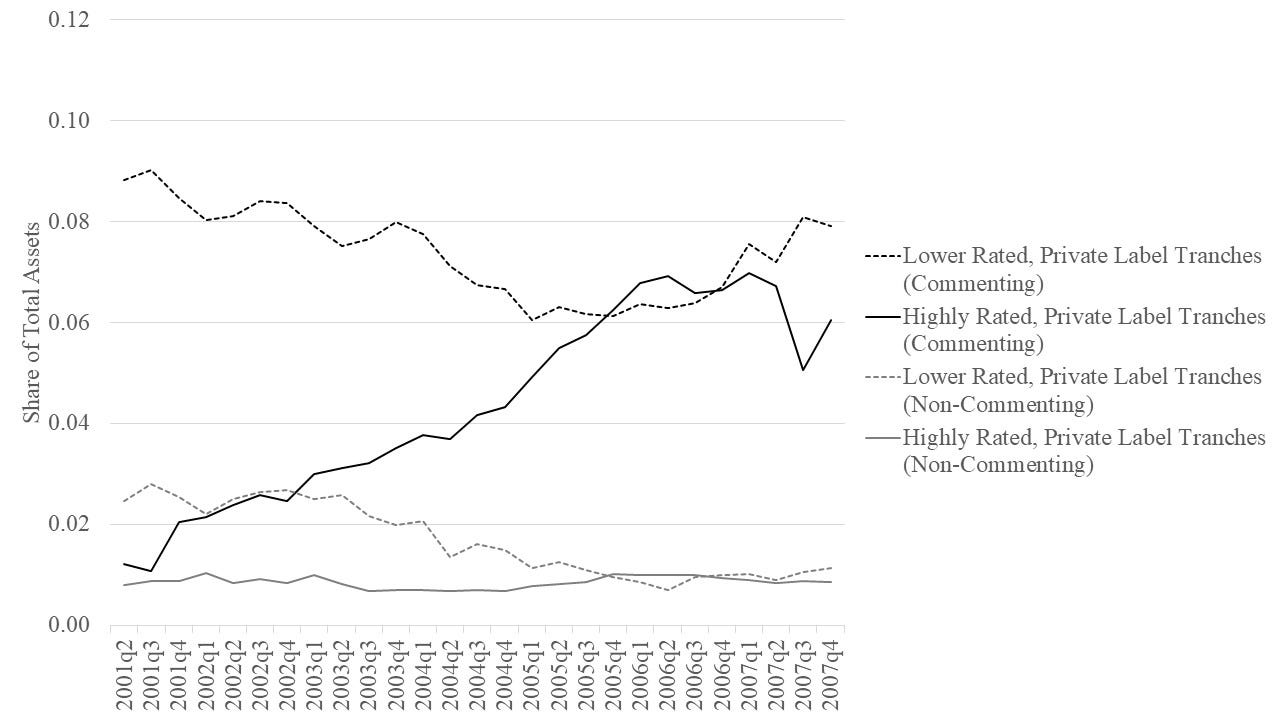

For the published version of my paper, in response to a referee’s request for changes to the working paper version, I used an electronic Freedom of Information Act request to get comment letters of the Recourse Rule notices of proposed rulemakings. That turned out to be useful because a handful of larger, securitization-active banks had subsidiaries that offered lengthy comments during the notice-and-comment period. Hypothetically, if a bank subsidiary responds, you might expect the bank to make subsequent use of the rule. Below you can see empirical evidence that’s consistent with the hypothesis and in the paper I offer some econometric tests, as well.

The graph shows that banks with subsidiaries that commented on average increased their highly-rated tranche asset share leading up to the crisis from about 1 percent to 6 percent. They also decreased their lower-rated tranche asset share from about 9 percent to 6 percent – the brief reversals in trends toward the end of the sample may reflect ratings downgrades, but I have no data to confirm that. You also see that banks that did not comment on average did not increase holdings of highly rated tranches but reduced holdings of lower rated tranches; they likely exited the market. I also found that banks with larger exposures to highly rated tranches on average were closer to defaulting and had greater changes in equity return volatility during the heart of the crisis from Q2 2008 to Q1 2009. It’s in that sense that the Recourse Rule contributed to that crisis.

One rebuttal to the hypothesis that the rule change contributed to the crisis could be that the highly-rated, private label securitization tranche classification includes a wide variety of assets, from mortgage-backed securities (MBS), which overall did well, to CDO tranches, which lay at the heart of the crisis. I, therefore, wrote a follow up working paper to examine these issues. While I use a smaller sample than in the earlier study, large banks with subsidiaries that commented on the Recourse Rule also had CDO exposures and on average the market priced in substantial risks of insolvency for these banks during the crisis, but not before; in a related study, I show how these costs of restoring solvency were historically at their highest for the largest banks during Q1 2009. Non-commenting banks on average did not face such risks.

Another rebuttal could be that my studies are US focused. However, using more granular data, Matthias Efing showed that German banks with less slack above the required regulatory minimum amount of capital “reached for yield” and underperformed during the crisis. That paper provides evidence showing how risk-based capital contributed to the crisis faced by German banks.

2. On the “Gaming” of Risk-Based Capital Requirements

Basel’s risk-based capital standards encourage “gaming”, in a lawful way. I make the “lawful” distinction because the word “gaming” can have a nefarious connotation as when it results in something unscrupulous. A good analogy for the effects of bank capital regulation could be the long-standing dictum that the Internal Revenue Service through the tax code encourages taxpayers to reduce their tax liability, in a lawful way.

As I alluded to in my previous blogpost about the supplementary leverage ratio, with the leverage ratio, banks can only increase/decrease it by increasing/decreasing equity funding. Banks can increase/decrease their risk-based capital ratio by increasing/decreasing equity funding or by increasing/decreasing holdings of low risk-weight assets. The second avenue provides the window through which to satisfy capital requirements without increasing equity funding, in a lawful way.

The graph above showed the kind of “gaming” that I mean in the years leading up to the financial crisis: some banks took advantage of the rule to hold more highly-rated, private label securitization tranches. But after the crisis, there was a similar kind of “gaming”, in a lawful way, during the implementation of US Basel III, which I wrote about in a co-authored study.

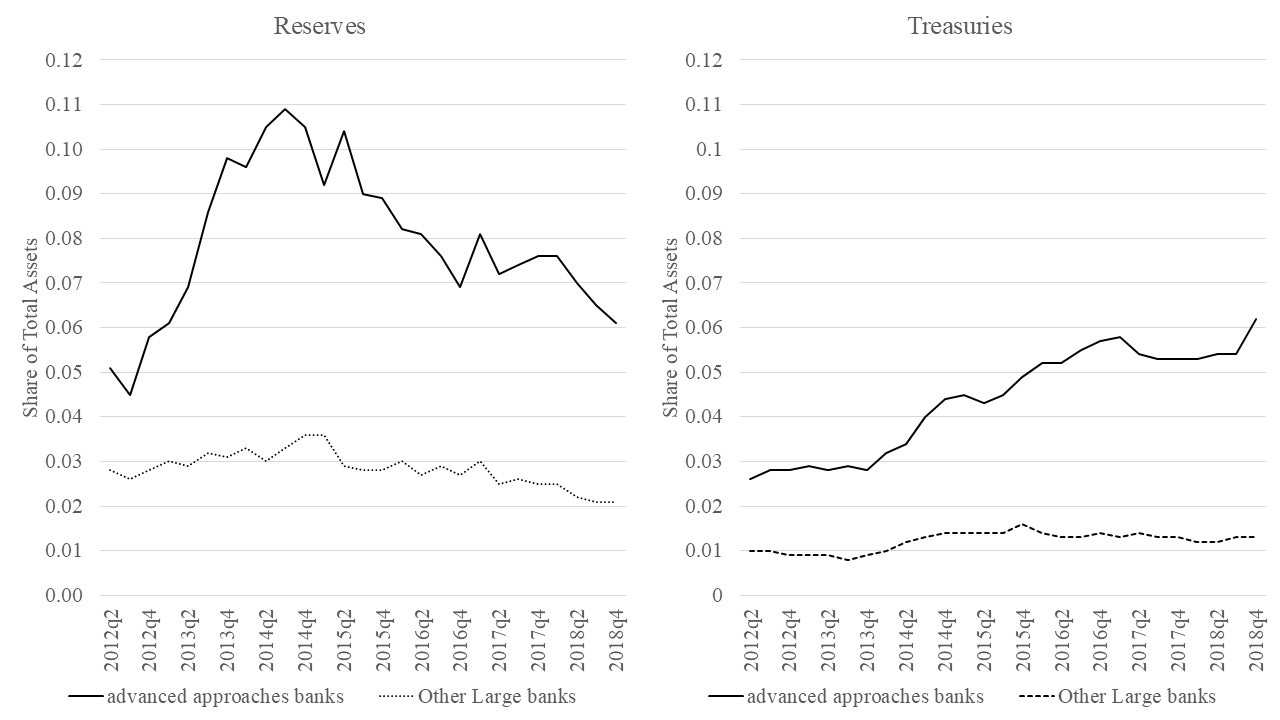

The study focused on how the so-called “advanced approaches” banks responded to the introduction of the new guidelines. The new guidelines called for increasing the minimum Tier 1 capital ratio from 4 to 6 percent. That might not seem like much from a percentage point perspective, but you can see how these banks responded in the graphs below.

From Q1 2013 to Q3 2014, the largest banks increased holdings of reserves from 6.1 percent to 10.9 percent, while holding their share of Treasuries at just under 3 percent. But after that, we also found that the advanced approaches banks also tended to shift toward holding more Treasuries when Treasury yields were relatively higher. Other large banks were less responsive to that rate differential between reserves and Treasuries. While banks had to comply with risk-based capital requirements before the liquidity coverage ratio was implemented, we don’t rule out that some of the changes might reflect the latter, and provide insight about that breakdown, too.

3. Are Risk-based Capital Ratios Neutral to Capital Allocation?

To motivate the co-authored paper that examined whether the implementation of US Basel III distorted bank asset holdings, we used an optimal bank allocation problem to determine how changing risk-based capital and leverage ratios affect bank asset shares. We found that if you held the leverage ratio fixed and increased the risk-based capital ratio, as happened in 2013, then banks would increase their holdings of low risk-weight assets, like reserves and Treasuries. We also found that unlike smaller large banks, the advanced approaches banks hardly increased their loan shares, which is understandable given that commercial loans receive the full 100 percent risk-weight. While increasing risk-based capital requirements result in significant distortions, we also find that if you were to increase the leverage ratio, holding everything else constant, that could result in minor distortions in bank asset shares. We suspect that’s because more equity funding for banks means less deposit funding, such that the banks might slightly reduce reserve shares given that we assumed banks faced reserve requirements (this was prior to 2020).

Overall, risk-based capital requirements contribute more to balance sheet distortions than cost of capital. Remember, equity capital regulation aims to cover unexpected losses, unlike risk-based capital which aims to turn all unexpected losses into expected losses. The Recourse Rule showed that didn’t work so well with what turned out to be risky securitization tranches. In Spring 2023, we also saw how SVB’s large exposures to zero/low risk-weight Treasuries/MBSs contributed to its demise given that the market value of capital deteriorated throughout 2022, well before it failed.

4. Banks Could Fund With Much More Equity

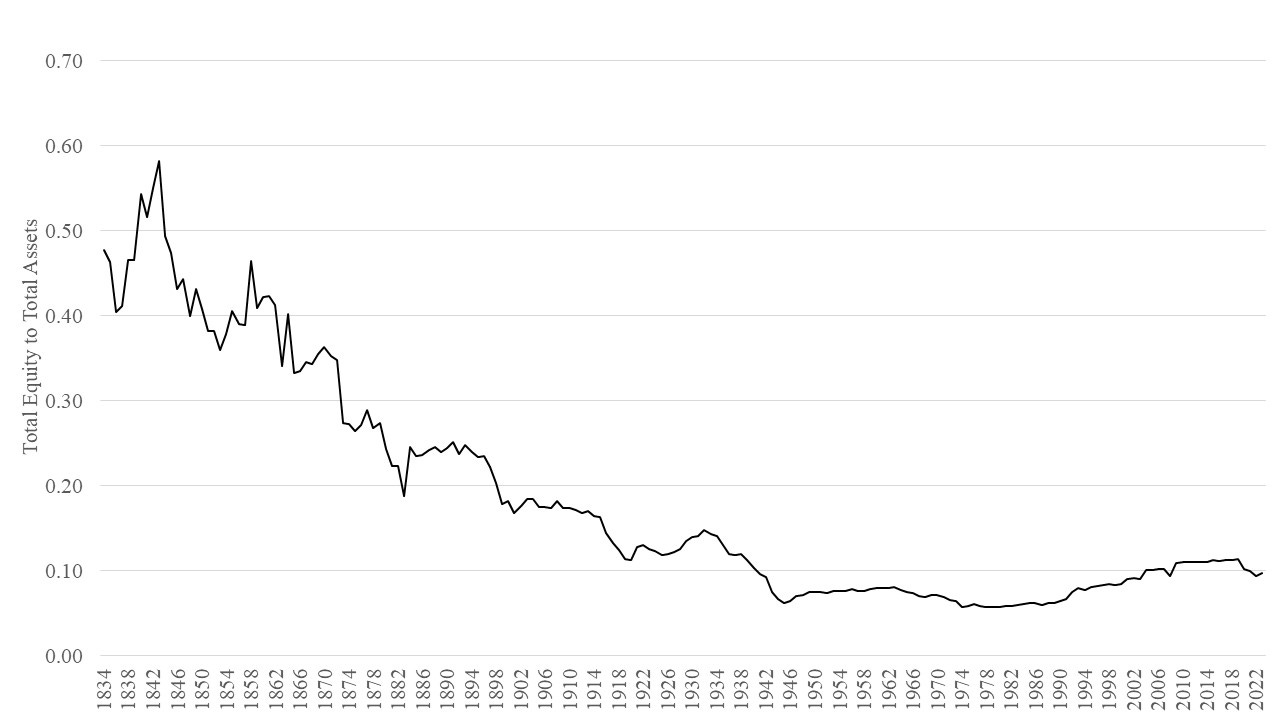

Last but not least, banks certainly could fund with much more equity than they currently do – and as the graph below shows, historically, they have. So when you hear people discuss how much more capital there is in the banking system now, that’s relative to historically low values. From a theoretical perspective, you wouldn’t expect models that assume historically low capital funding to predict that capital should be much higher than it has been.

That’s what Jim Barth and I found in co-authored a paper in which we conduct a benefit-cost exercise of increasing the minimum capital-to-asset leverage ratio from 4 percent to 15 percent over a long horizon. Even though we biased our results toward assuming banking crises having mostly temporary rather than permanent effects, we still find that the benefits of moving to 15 percent generally outweigh the costs. In our baseline case, we found the optimal leverage ratio equaled 19 percent, while the average and median across all assumption-based cases equaled 22 percent. These values are consistent with Admati and Hellwig’s recommended 20-30 percent range.

Concluding Thoughts

In a past post, I wrote about how capital regulation was supposed to be a simple, low cost way of regulating banks. Instead, it’s become highly complex and costly. Jim Barth and I in a companion piece on how regulatory capital has evolved in recent decades showed that after Basel III, at least 20 percent of all bank regulation concerns bank capital. Only large banks have the staffing necessary to comply with the most complex parts, which creates a regulatory moat around those complying with the regulation. That complexity also comes with unintended effects that tend to get ignored in regulatory debates, because they’re not always obvious to even the trained eye. A simpler, higher capital regime presents a more robust alternative for all banks.