Basel III Endgame Not Likely the End of the Regulatory Capital Revisions

With the voluntary liquidation of Silvergate and the recent failures of Silicon Valley Bank (SVB), Signature and First Republic out of the way, regulators and bankers will now begin sparring over proposed regulatory changes. In a recent speech, Vice Chair of Supervision Michael Barr has given us a glimpse of what to expect, including among other things, finalizing Basel III and long-term debt rules for large banks that are not quite as large as the global systemically important banks (G-SIBs), based on the $100 billion in total asset threshold.

Before addressing some of the specifics, at least some of the proposed changes were likely in the works before the recent failures. As such, the speech reflects a typical problem arising with regulatory reform as regulators chose what they’d like to change first, then write up the proposed rule and finally do the analysis to justify the rule change, rather than investigating the actual underlying problem before coming up with a solution. You can call it the “ready, fire, aim” approach. But also, the speech reflects another recurring problem in bank regulation, namely that changes often aim to fix the last “crisis,” as in, “if only we’d done x, y wouldn’t have happened.”

More Capital, But Which Kind?

The highlight of the speech in my view lies in the 4th paragraph:

[T]here is a component of bank funding—equity capital—that is well suited to building resilience. Banks rely on both debt and capital to fund loans and other assets, but capital is what allows the bank to take a loss and keep on operating. The beauty of capital is that it doesn’t care about the source of the loss. Whatever the vulnerability or the shock, capital is able to help absorb the resulting loss and, if sufficient, allow the bank to keep serving its critical role in the economy. Higher levels of capital also provide incentives to a bank’s managers and shareholders to prudently manage the bank’s risk, since they bear more of the risk of the bank’s activities.

I fully agree with this view. Yet we get the specifics of the envisioned change in the 25th paragraph. Vice Chair Barr suggests a 2 percentage point increase in the risk-based capital ratio could be in the works. What could be wrong with that?

Risk-Based Capital Means Regulatory Arbitrage, Unintended Consequences and Less Capital

Well, you can increase the risk-based capital ratio two ways: 1) adding more capital, but also by 2) lowering the risk-weighted asset measure, which you can do by increasing holdings of assets that the regulation says requires less capital. Commercial loans have among the highest risk-weights, mortgages held on balance sheet and municipal bonds require about half the capital as commercial loans, and mortgage-backed securities (MBS) and Treasuries require little to no capital. That in mind, if banks always chose the first option, I wouldn’t have an issue here. But when you give banks the choice between the two, the second option gives banks incentives to choose assets that the regulation says requires less capital, irrespective of whether the regulation actually correctly identifies how risky are the underlying assets. So when has this gone wrong?

Regulatory Arbitrage and the 2007-2009 Crisis

For starters leading up to the 2007-2009 Crisis. While we tend to think of low risk-weight assets as being safer, in 2008, highly rated CDO tranches were deemed safe but turned out to be the assets at the heart of the crisis. I showed in one study that when U.S. regulators adopted Basel II risk-weights in 2001 for highly rated securitization tranches, banks that commented on the regulation increased holdings of the highly rated tranches and decreased holdings of lower rated tranches. A related study by Berkeley Professors Stanton and Wallace showed that commercial MBS yields fell relative to corporate bonds after the same rule change in 2001, which is also consistent with a greater demand arising from the reduced capital requirements. And this wasn’t just a problem in the U.S. as this recent study showed German banks engaged in similar regulatory arbitrage in response to Basel II risk-weights. These are examples of the unintended consequences of regulatory changes that often get overlooked in debates over regulatory capital. But there’s more.

Implementing U.S. Basel III

Then in 2013, after the Basel III standards were finalized, my co-author and I showed that relative to the control group, the largest banks, which are subjected to the most stringent Basel standards, increased holdings of reserves and Treasuries, which have the lowest capital requirements. Also, relative to the control group, they also reduced holdings of loans, especially those with the highest capital requirements, such as commercial loans. However, that doesn’t mean higher regulatory capital requirements reduce corporate lending overall. For instance, a related study by Federal Reserve staff economists showed that other smaller banks pick up the slack when the largest banks turn down commercial lending due to such regulatory changes. What it does mean is that banks that do not actually increase their capital relative to total assets, but simply game the risk-based capital by holding assets that regulators say require less capital have more distorted balance sheets and less capital to absorb unexpected losses.

The Inflationary Bear Market of 2022

After peaking in early 2022, the equity market together with the bond market experienced significant declines in 2022 in response to rising inflation. Even more traditional mortgage-backed securities and Treasuries, which might be safe from default risk, experienced losses due to the sudden increase in inflation. This was the case with SVB, as I discussed in an earlier blogpost, which had a significant share of its assets in MBS as well as Treasuries. A recent working paper shows that across the banking system, unrealized losses amounted to $2.2 trillion. This finding does seem to justify the proposal in the 24th paragraph of Vice Chair Barr’s speech to have large banks account for unrealized losses.

But such examples illustrate how risk-based capital requirements make it hard for anyone outside the bank to interpret, because without spending time looking at balance sheet data, you won’t know how a bank attained the higher risk-based ratio. But let’s look further at the evolution of risk-based capital and two other measures of capital between 2021 and 2022 for the failed banks.

Three Measures of Capital

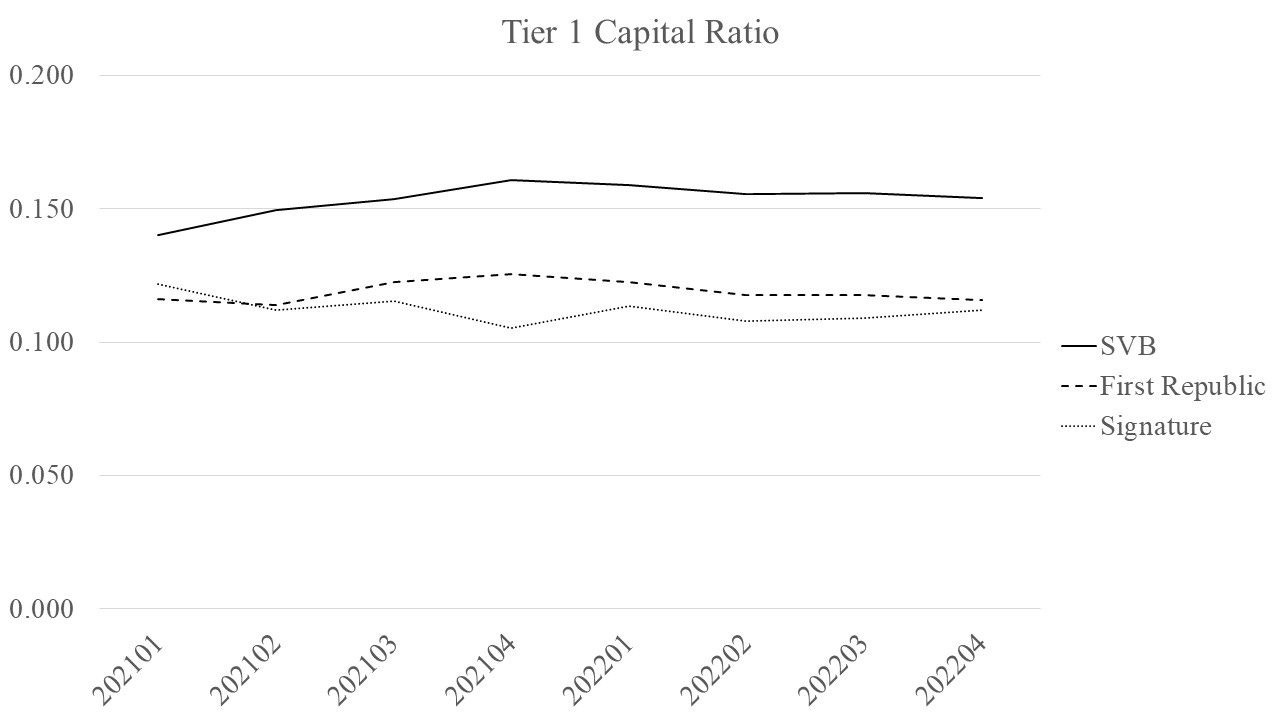

If you look at the Tier 1 ratio (Tier 1 capital relative to risk-weighted assets) reported by the three failed banks, First Republic and Signature had ratios above 10 percent in 2021 and 2022, while SVB had ratios above 15 percent during that same time.

How could a bank with regulatory capital ratios that high fail? Because these measures mask how far you are from default. The same thing happened in 2008, as former Scurities and Exchange Commission Chief Economist Mark Flannery showed in 2008 for the largest U.S. banks, which all satisfied the regulatory ratios but still experienced distress.

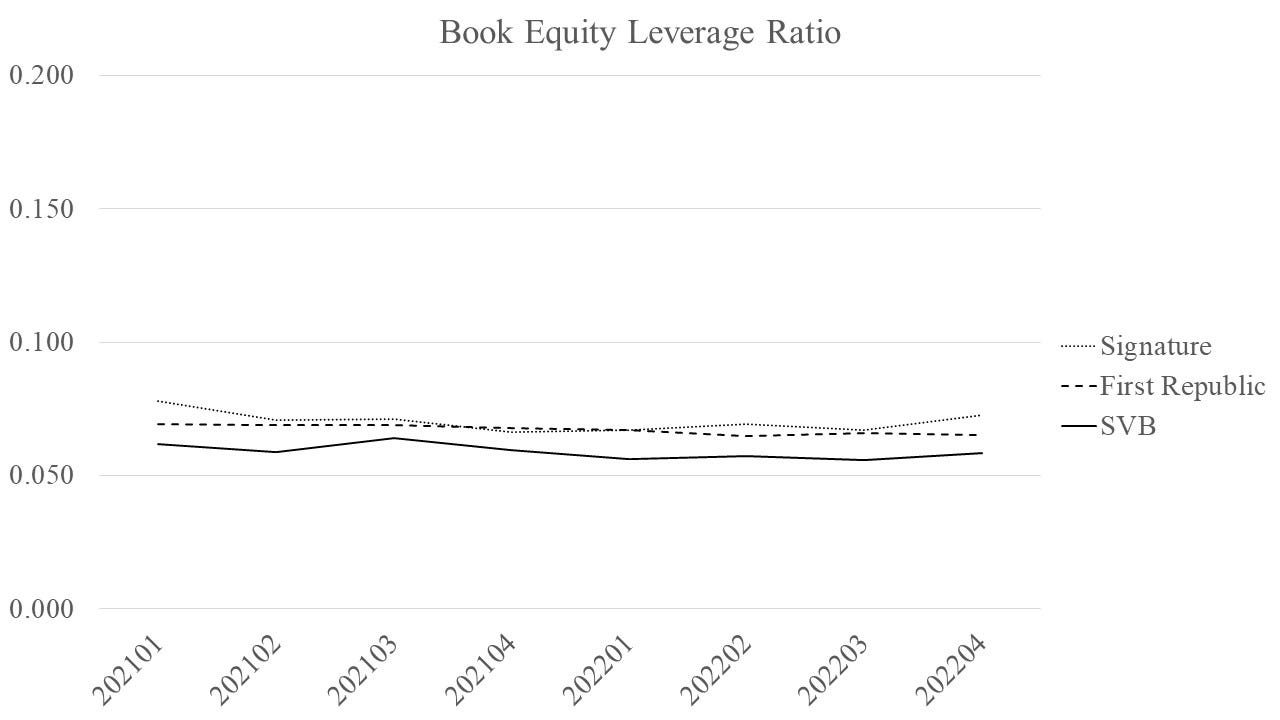

But let’s look at the simpler book equity to book asset leverage ratio for the three banks. They suggest that the three banks were closer to default than what the risk-based capital ratios suggest in 2021 and 2022. Relative to the Tier 1 risk-based capital ratio, the leverage ratio for SVB equaled only about 39 percent, for Signature equaled only about 63 percent, and for First Republic equaled only about 57 percent.

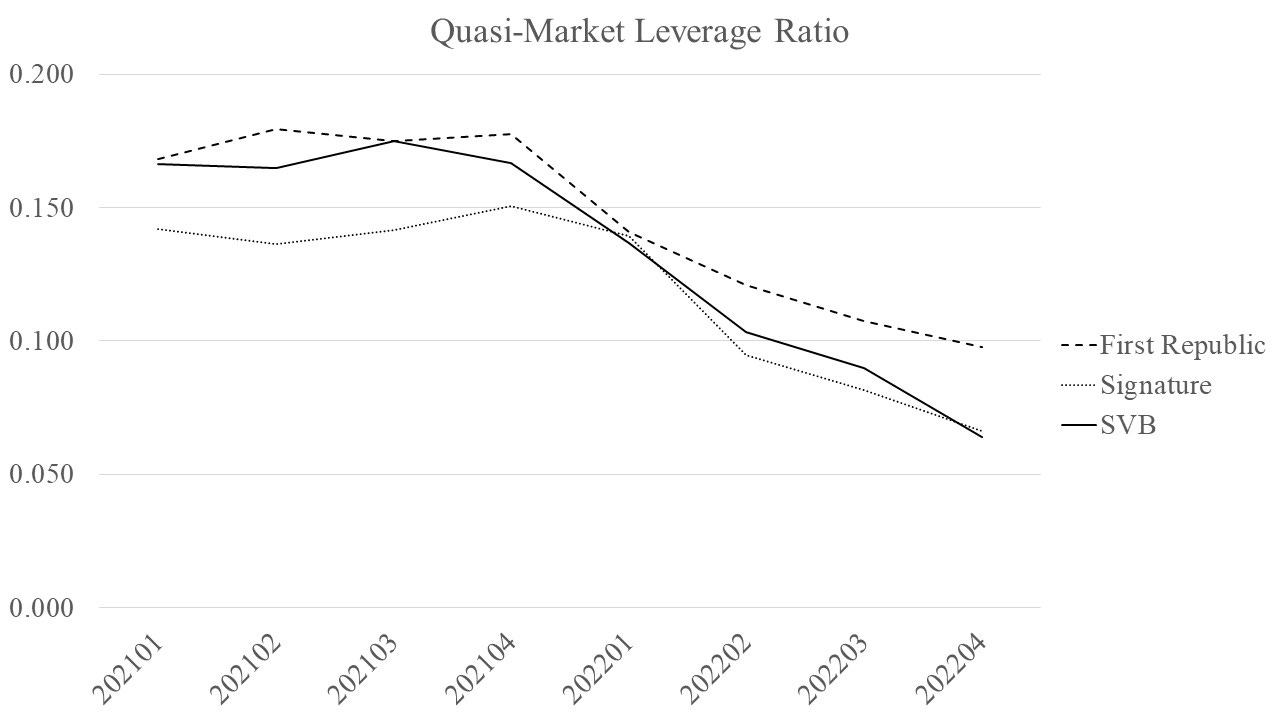

Finally, have a look at the quasi-market leverage ratio (the ratio of the market value of equity, relative to the quasi-market value of assets calculated as book assets minus book equity plus the market value of equity). You can see that during the 2022 Bear market the market values were dropping sharply. Relative to the Q4 2021 value, by Q4 2022 SVB’s dropped over 10 percentage points, and Signature’s and First Republic’s dropped at least 8 percentage points by the end of 2022. These declines were observable well in advance of the depositor runs in Q1 2023. That suggests to me that the equity market understood that there was something ominous happening at these banks.

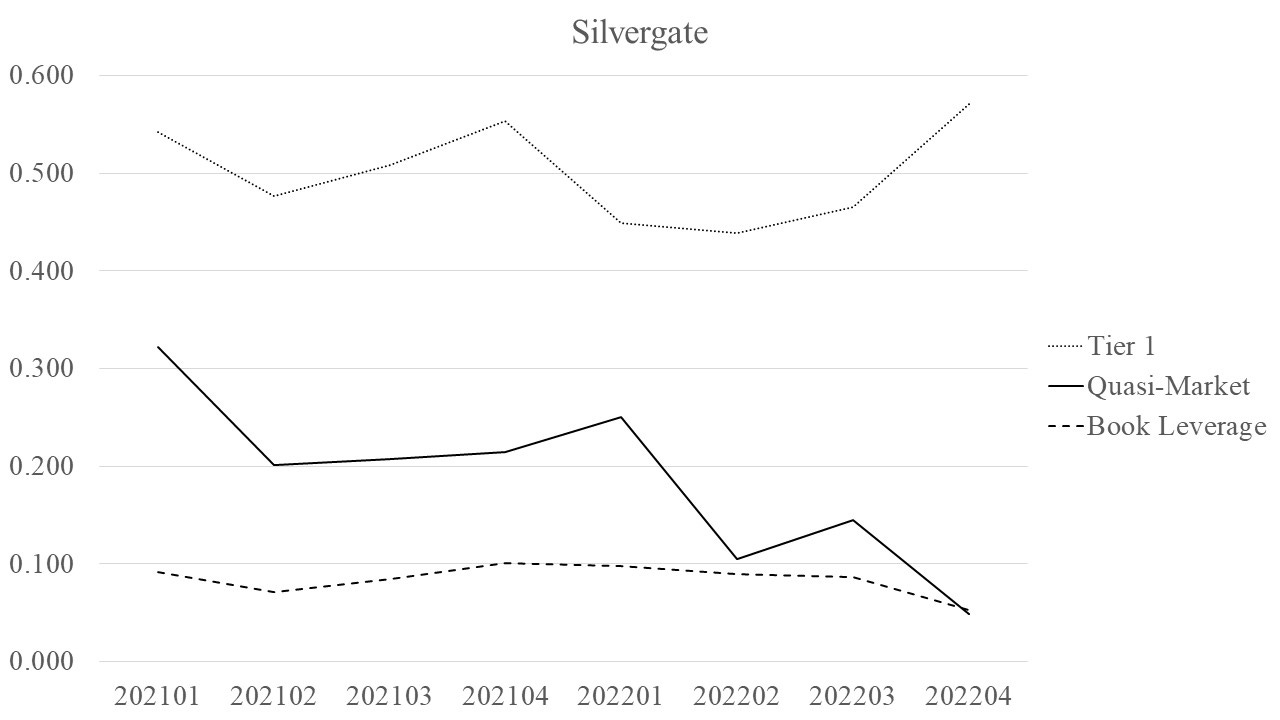

And then let’s look at Silvergate, which while smaller, did us a favor by voluntarily liquidating – and more weak banks should do this. In 2022, Silvergate’s Tier 1 ratio rose above 50 percent, just as its quasi-market and even the book leverage ratio began dropping.

In sum, the Tier 1 capital ratio can give a false sense of resilience concerning a particular bank, and the book and quasi-market leverage ratios reveal that these banks were much closer to default. It would make sense for regulators to keep an eye on market values, rather than focusing on once again simply fixing the existing regulatory measures of risk-based capital. After all, the Basel Committee and national regulators have been revising the guidelines for about 35 years now.

On Long-term Debt Rules

As Tom Hoenig and I have written about them elsewhere, I won’t say much about long-term debt rules here other than more long-term debt still means more leverage.

One Last Thought On the $100 Billion Asset Threshold: Stop Using Nominal Asset Values

In the speech, Vice Chair Barr suggests using a $100 billion asset threshold as a cutoff for the new regulatory capital requirements in the 5th, 23rd and 24th paragraphs. The asset thresholds have spurred debates that reflect partisan biases, with Republicans tending to want higher thresholds so that fewer banks are subjected to the regulation and Democrats tending to want lower thresholds so that more banks are subjected to the regulation. However, using nominal values in regulatory guidelines does not serve the public interest well, as I pointed out how their use can give misleading insights in a previous blogpost.

First, inflation tends to be positive, so over time the nominal threshold just scoops up more firms. If that’s what legislators and regulators want, then they should explicitly state that in the legislation and regulation. But even if you index the bank asset threshold to some measure of inflation, you can still be misled about a bank’s size because the banking sector grows over time. At the time of the 2008 Crisis, there were about $12 trillion in total assets and today there are about $23 trillion. So in nominal terms, banking sector assets have nearly doubled since then. What might be a better way to think about this?

Perhaps if we used a bank’s share of total sector assets that might give a less distorted view about bank size. As a fraction of total banking sector assets, I showed in that blogpost that First Republic had about 1 percent, SVB had 0.9 percent, and Signature had about 0.5 percent. When looked at this way, these banks seem smaller than what the headlines have suggested. They won’t grab headline attention the way dollar values do, but they can tell you more about how large a bank is in a way that escapes the noise created by inflation or banking sector asset growth.

Concluding Thoughts

Whatever changes take place, as long as they continue to call for more tinkering of risk-based capital guidelines that means we won’t likely see the end regulatory capital reform. Not only do they lack effectiveness, but as I showed in a blogpost some time ago, since Basel III about 20 percent of all of the federal regulatory code for banks arises from bank capital guidelines. One response to this observation could be that the complexity reflects how important regulators think capital is, given concerns over “Too Big to Fail”. The problem is, the risk-based capital guidelines, which are driving that regulatory complexity, don’t actually tell us which banks are well capitalized. They just tell us which banks regulators think are well capitalized. The equity market does seem to know when that’s not the case.